Patient-centered capitalism: redefining ethics in the medical industry

by Brian Jackson - STAT - September 24, 2019

Corporate misbehavior in the health-care

sector is widespread: irresponsible opiate marketing, misrepresentation

of research data, price gouging, and on and on. Some see it as

capitalism run amok.

In one sense, this isn’t surprising. As the Business Roundtable acknowledged in a recent statement,

American companies have too long prioritized shareholders and profits

over the interests of employees, customers, and communities. Health-care

companies are businesses, so why shouldn’t we expect them to act the

same way?

Why? Because health care isn’t just another consumer product. It is

more than that. The Hippocratic ideals of putting patients first are

ingrained in our culture and reflected in the regulation of medical

licenses and malpractice law. But although Hippocratic ideals have long

been the basis of expectations for medical professionals, they haven’t

yet been formally applied to health care companies. This is a major

shortcoming in an era when the actions of large health systems,

pharmaceutical companies, device companies, and insurance companies can

have even greater effects on patients than the actions of individual

clinicians.

advertisement

All of which is why I, a physician working in the clinical laboratory

industry, am excited about the growing interest in stakeholder

capitalism that the Business Roundtable laid out: for a business to be

sustainable over the long term, it must explicitly address the interests

of all major stakeholders. Owners (shareholders) are an

important stakeholder group, but so are customers, employees, and the

community in which the business operates.

Of all industry sectors, I am convinced that health care has the

most to gain from this model. Health care may also have the clearest

path to stakeholder capitalism due to some of its distinctive

characteristics.

First, the health-care industry includes groups that share a common

ethical culture and language. These include physicians, nurses,

scientists, and other professionals, all of whom are schooled in medical

ethics during training. It also includes mission-driven hospitals and

health systems, including many with religious affiliations.

Second, health care will find it easier than many other industries to

find the right balance among its various groups. The doctrine of

shareholder supremacy has a certain elegance in that it simplifies the

decision about which group comes first — shareholders. Medical ethics

and patient-centered capitalism offer an equally elegant solution:

patients come first and all others, including shareholders, come second.

Third, health care has a mature and well-defined set of ethical

principles against which to measure corporate behavior. The ethical

codes of the American Medical Association and the American Nurses Association are well-known examples, though they are worded specifically for individual practitioners. Another example is the Belmont Report,

commissioned by the U.S. government in 1978, which laid out rules for

conducting research on human subjects. All of these codes are based on

three core principles: respect for persons, beneficence, and justice.

Respect for persons includes autonomy and informed consent. If

medical device manufacturers followed this principle, they would have to

disclose to patients how likely they will be to actually benefit from a

particular hip replacement or pacemaker or cardiac stent. They would

also have to disclose whether there might be a competing device with a

higher success rate and a lower complication rate.

Beneficence includes the Hippocratic maxim of “Do no harm.” If

oxycodone and fentanyl manufacturers had followed this principle, they

would not have downplayed the abuse potential of these drugs in their

marketing messages to doctors.

Justice involves fairness for all patients. Health insurers following

this principle would need to ensure equitable coverage across all ages,

genders, disease categories — including mental health — and among

vulnerable populations.

Fourth, health care guided by patient-centered capitalism offers a

rich set of structural opportunities for accountability to all

stakeholders. Large health systems and group-purchasing organizations,

for example, have enormous market power over suppliers of medical

products. This power is currently leveraged mainly to obtain lower

prices, but it can just as easily be used to preferentially choose

suppliers whose marketing meets scientific standards of objectivity, who

contribute all clinical data to public registries, and who meet other

defined standards.

Likewise, medical professionals such as physicians and nurses have

enormous potential influence on health care companies. They can openly —

and ideally collectively — declare their expectations regarding the

companies they work for and whose products they use, and then back up

these statements with their career choices and medical product choices.

There is an obvious accountability role for regulatory agencies in

patient-centered capitalism such as the Food and Drug Administration and

the Centers for Medicare and Medicaid Services, but distributed mutual

accountability will be more robust than one-directional regulation

alone.

Changing corporate culture across an industry as huge as health care

will take time. But the barriers can be overcome. And the Business

Roundtable just took away one of them — the business doctrine of

shareholder supremacy — or at least signaled a willingness to do so.

The public expects and deserves ethical actions not just from

individual health care workers but also from the organizations and

companies in this sector. It’s time we make this happen.

Patient-centered capitalism can point the way. https://www.statnews.com/2019/09/24/patient-centered-capitalism-redefine-ethics-health-care/

Employer Health Insurance Is Increasingly Unaffordable, Study Finds

A

relentless rise in premiums and deductibles is putting insurance out of

reach for many workers, especially those with low incomes.

by Reed Abelson - NYT - September 26, 2019

Jessie McCormick had to quit her job to afford health care.

Ms.

McCormick, 27, who has a heart condition, had an opportunity to move

from part time to full time in her job at a small nonprofit in

Washington. Working full time would qualify her for the firm’s health

plan.

But she calculated that her out-of-pocket costs would be at

least $1,200 per month, about double the money she had left after

paying her rent and utilities.

Instead, she quit her job last

summer so her income would be low enough to enroll in Medicaid, which

will cover all her medical expenses. “I’m trying to do some side jobs,”

she said.

Employers remain the main source of health insurance in

the United States, covering about 153 million people. But premiums and

deductibles are pushing employer-based coverage increasingly out of

reach, according to a new analysis released Wednesday by the Kaiser Family Foundation, which conducts a survey of employers every year.

The

average premium paid by the employer and the employee for a family plan

now tops $20,000 a year, with the worker contributing about $6,000,

according to the survey. More than a quarter of all covered workers and

nearly half of those working for small businesses face an annual

deductible of $2,000 or more.

The new data on

employer coverage come as the Democratic presidential candidates debate

sweeping reforms to diminish the role of private insurance in the

American health system, including expanding the federal Medicare program

to everyone or giving people the option to enroll in a government-run

plan.

Many of the arguments for both systems center on expanding

health insurance to more of the estimated 27 million people who lack it.

But millions of people who already have coverage are deeply

dissatisfied with the current system as well.

“For some reason, we

like to focus on coverage when the issue for workers, people and the

public generally is cost,” said Drew Altman, the chief executive of the

foundation. About 2,000 small and large businesses responded in detail

to the survey.

Small employers in particular, and their workers, are struggling.

“Health

insurance in the United States is incredibly prohibitive for small

businesses,” said Shalin Madan, the founder of a small investment

advisory firm in Florida. He is not required to provide health insurance

to his workers, because his business is too small and he outsources

much of the work.

A policy for his own family, he said, runs about

$2,000 a month ($24,000 per year), with a $13,000 deductible. “I’m out

$37,000 before I see a return on investment, if you will,” Mr. Madan

said.

A recent Wall Street Journal/NBC News poll found that a

majority of registered voters, 56 percent, are opposed to the idea of a

government-run system like Medicare-for-all that would replace private

insurance. But Mr. Madan said the current system results in a schism

between those who have good employer coverage and those who do not.

“I had phenomenal health insurance being employed,” said Mr. Madan of his time working for a larger corporation.

One

of Senator Elizabeth Warren’s applause lines on the Democratic

presidential campaign trail is that no one likes their insurance

company. But employer coverage “isn’t monolithic,” said Mr. Altman.

While

some people, usually higher-paid professionals or union members, enjoy

generous coverage from their job, people making $25,000 or less — about

36 million Americans — are the most likely to be priced out of coverage,

he said.

People who work at companies where a large share of the

employees are low-wage workers pay an average of $7,000 annually for a

family plan, according to the survey, about $1,000 more than those

working at companies made up of better-paid workers.

Only

one in three of these workers is enrolled in an employer’s plan, about

half the rate at better-paying companies. “This is a group that really

deserves a lot more attention,” Mr. Altman said.

While some

low-wage workers may qualify for Medicaid in states that expanded it

under the Affordable Care Act, those with private insurance who are not

eligible for government help are having a more difficult time affording

care, said Dr. Benjamin Sommers, a health economist at the Harvard T.H.

Chan School of Public Health.

“The arc of the A.C.A. really tried, and largely succeeded, in leaving the employer market as is,” he said.

For

many businesses, it’s a Sophie’s choice between raising an employee’s

share of premiums or increasing the size of the deductible.

“I

try to keep the benefits pretty much the same,” said Joel Sturm, chief

operating officer of the New York College of Podiatric Medicine. The

majority of workers are in a plan that comes with a deductible of $1,000

for an individual and asks them to pay about 10 percent of their

medical bills. “It doesn’t kill them if they go,” Mr. Sturm said.

But

the employees must pay a hefty share of the overall premiums, about

$950 a month for a couple. Some employees have quit as a result of

having so much taken out of their paycheck and still having to cover

some out-of-pocket costs, Mr. Sturm said. “They’d rather be unemployed

than have very little take-home pay,” he said, adding that Medicaid can

seem like a more attractive option.

Image A

tag on Ms. McCormick’s backpack. Koda, her medical alert dog, can smell

when Ms. McCormick’s blood pressure drops, usually signaling an

imminent fainting spell.CreditSamuel Corum for The New York Times

Many

businesses have opted to increase deductibles instead of premiums. “A

lot of employers with lower-paid employees want to offer a low-cost

option that is typically a high-deductible plan,” said Chris Bartnik, a

senior vice president at Lockton Companies who advises businesses on

their coverage.

But some of his clients who once

embraced high deductibles have changed their minds, worried their

workers can’t afford to go to the doctor.

Some large employers are

adjusting the premiums and deductibles based on an employee’s income.

JPMorgan Chase pays 80 percent of the premiums for workers making under

$60,000, and the company lowered the annual deductible by $750 to $2,000

or less, depending on the plan they choose.

(JPMorgan Chase is also part of the trio of big corporations behind Haven, a new venture trying to reinvent employer-based coverage.)

H.A.

Cover & Son Lumber, in Thayer, Mo., has decided to pay the bulk of

premiums for workers, but the plans come with a deductible of $2,500 for

an individual and $5,000 for a family. The company is paying about

$16,000 a month to cover the 11 people enrolled in the plan.

The

deductible “is higher than we wanted to go,” said Marion Cowen, who

oversees benefits for the business, but the cost for more comprehensive

coverage was prohibitive. “We don’t know what we’re going to do if it

goes up much more,” she said.

She is intrigued by the idea of

being allowed to buy into a government plan, like Medicaid or Medicare,

that is being floated by some of the candidates. “We would consider it,

yes, we would,” she said, if the option saved money and provided

employees with high-quality coverage.

The

Wall Street Journal/NBC News poll found that about two-thirds of voters

supported the idea of allowing people to buy into Medicare. “Some states

are looking at a public option,” said David Chase, who leads the

national outreach efforts for Small Business Majority, an advocacy group

that supported the Affordable Care Act. He said the group is talking to

various states about allowing small businesses the option of buying

into a government program.

“There are a lot of hypothetical

proposals out there,” said Neil Trautwein, vice president of health care

policy at the National Retail Federation, who said his members are

increasingly concerned about rising health care costs. Companies are not

as keen on offering less generous plans, he said, but would be open to

other alternatives.

At Bagel Grove in Utica, N.Y., most of the 20 employees are now covered by Medicaid, said Anne Wadsworth, one of the owners. She

took advantage of the tax credits available to small businesses that

helped pay for the cost of coverage under the Affordable Care Act, but

the credits ran out. While she still covers 45 percent of the premiums,

all but one of her employees, herself included, have found better plans

on their own.

“I was all on board for Obamacare,” she said, but

it proved not to be “a long-term solution. It doesn’t lower the costs

for people.”

Ms. Wadsworth is wary of the sweeping plans now

proposed by the Democratic presidential candidates, which she worries

will become a political football, like the Affordable Care Act, and fail

to address the underlying issues.

“I just think health care costs need to go down,” she said. https://www.nytimes.com/2019/09/25/health/employer-health-insurance-cost.html?

Why the Private Health Insurance Industry Faces an Existential Crisis

A former health insurance executive says the moment the insurance industry fears most has arrived.

by Wendell Potter - Common Dreams - September 24, 2019

I have told a lot of stories about my time near the top of the health

insurance industry. This is not one I’ve ever shared, until now.

Shortly before I left Cigna, I was at a meeting of the company’s

senior executives. This was as then-presidential candidate Barack Obama

was gaining traction in national polls and filmmakers like Michael Moore

were documenting how broken our health insurance system had become. Our

CEO at the time, Edward Hanway, had just been asked a simple question

by the company’s top attorney: “What keeps you up at night?”

He responded without hesitation. “Disintermediation.”

I had never heard the term and had to look it up. The definition: cutting out the middleman.

This is a watershed moment for Medicare for All and America’s health insurance companies.

What scared us most at the health insurance companies was our place

on the priority list for patients. We know people want to see their

doctor, visit their preferred pharmacy or attend any hospital in an

emergency. This makes doctors, dentists, pharmacists and nurses

essential to the delivery of health care. They’re the faces of it.

Behind the scenes are companies that make drugs and machines important

to treatment, along with people who conduct research and implement

health policies.

Our health insurance companies, in contrast, are not essential. They

don’t treat anyone. They don’t prevent anyone from becoming sick. They

don’t take you to the hospital or make sure you take your pills. They

don’t fund or discover medical innovations. They’re simply middlemen we

don’t need. And in the industry, we always dreaded the day American

businesses and patients would wake up to that reality.

That day has come.

SCROLL TO CONTINUE WITH CONTENT

A majority of America’s small businesses now support Medicare for All. So do a majority of Americans who receive health insurance

through their employer. In my 20 years working inside the industry and

the 11 years I’ve been watching from the outside, I have never seen such

high support among the people who get their coverage through their

employers for switching to a publicly financed, privately delivered

health care system.

This is a watershed moment for Medicare for All and America’s health

insurance companies. Fifty-eight percent of nonelderly Americans receive health insurance

through their employer. Now most of them—and their employers who pay

handsomely to provide insurance—have decided they’d rather work with the

government (through an improved and expanded Medicare program) than

continue a relationship with private insurers. That is a stunning rebuke

of the private sector, though not one that has been unforeseen, as

health insurers charged an average of $6,715 per insured employee last year—and $20,000 for a family plan—according to the Kaiser Family Foundation.

There are two things to note about how the insurance industry has

responded to this development: they’ve simultaneously tried to prevent

change and prepared for the unraveling of the employer-based system.

The evidence for both is the “Coverage@Work”

PR and lobbying campaign America’s Health Insurance Plans launched last

year. Even though the percentage of nonelderly Americans enrolled in

employer-sponsored plans has declined from 67 percent to 58 percent over

the past decade, despite the Affordable Care Act mandating insurance be

given to all full-time employees, companies like the one I used to work

for continue to make a lot of money on these kinds of plans. The

industry wants to keep employers in the game as long as possible, though

they’ve known for more than a decade that the employer-sponsored health

insurance system is collapsing.

They’ve also known that we have an aging population, which is why big

insurers have placed such a big bet on Medicare Advantage, the private

alternative to traditional Medicare. Insurers devote a substantial

portion of their sales and marketing budgets to lure Medicare-eligible

Americans into Medicare Advantage plans. The bet has been paying off:

more than half of some of the big insurers’ revenue (including

UnitedHealthcare, the biggest insurer) is now coming from federal and

state governments. A growing percentage is coming from their Medicare

Advantage business and also from the Medicare supplement plans they

sell, as well as from their Medicare Part D pharmacy plans and the

Medicaid programs they operate under lucrative contracts with most

states.

As he was elaborating on disintermediation, Cigna’s CEO said his fear

was that someday American employers and their workers would begin to

question the “value proposition” of private health insurers. That’s

business-speak for something not being worth what you’re paying for it.

That someday has arrived for America’s job creators. They are waking up

to realize the middleman is not necessary. It’s time for our policymakers to wake up, too.

Rebecca Grimm tried to be a smart shopper when her second pregnancy ended in a miscarriage last year.

Grimm,

who has a high-deductible health plan, first tried a $10 pill to clear

the fetal tissue. When that didn’t work, she checked her insurance

company website to compare the cost of a surgical procedure at several

local medical centers.

All were around $900, she recalled. Grimm went to a center a few miles from her house. The procedure took 20 minutes.

The Grimms got a bill for $5,948.69.

“We thought something had to be wrong,” said Grimm, who is 29 and

lives in a small house in the northern suburbs of Indianapolis. “Having a

miscarriage was hard. Having to deal with medical bills for months

afterwards was like salt in the wound.… It made no sense at all.”

High-deductible

health plans, which are fast becoming the dominant form of coverage for

U.S. workers, were supposed to empower patients. Backers said the plans

would create engaged shoppers who would check prices and compare

providers, forcing hospitals, doctors and drugmakers to control costs.

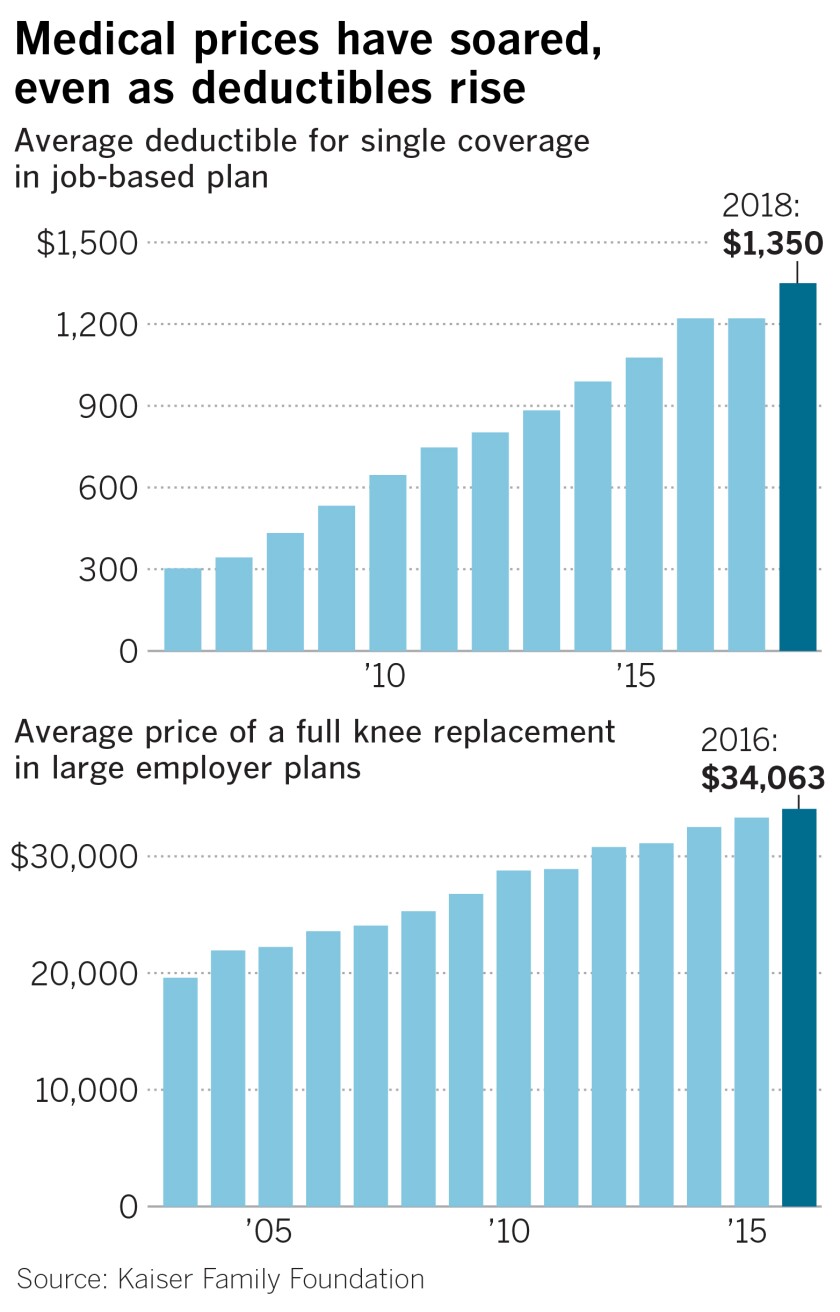

Deductibles have more than tripled over the last decade

for people who get insurance through their jobs, but the promised

consumer revolution never materialized. Instead, Americans have been

left shopping in the dark and increasingly struggling with medical bills

they can’t afford, a Times examination of job-based health insurance

shows.

“This idea that we were going to give patients ‘skin in the

game’ and a few shopping tools and this was going to address the broad

problems in our healthcare system was poorly conceived,” said Lynn

Quincy, former healthcare advocate at Consumer Reports now at Altarum, a nonprofit research and consulting firm.

“It’s clear now that the idea definitely hasn’t borne fruit,” Quincy

continued. “It hasn’t made people feel more confident seeking care. It

hasn’t led to better value. And it’s had terrible consequences on

patients’ ability to afford care.”

Although Americans are willing to seek out lower-priced generic

medications, few are comfortable shopping for medical care, studies and

surveys show. Patients like Grimm who do try are often frustrated by

incomplete or inaccurate information from insurers, hospitals and other

medical providers.

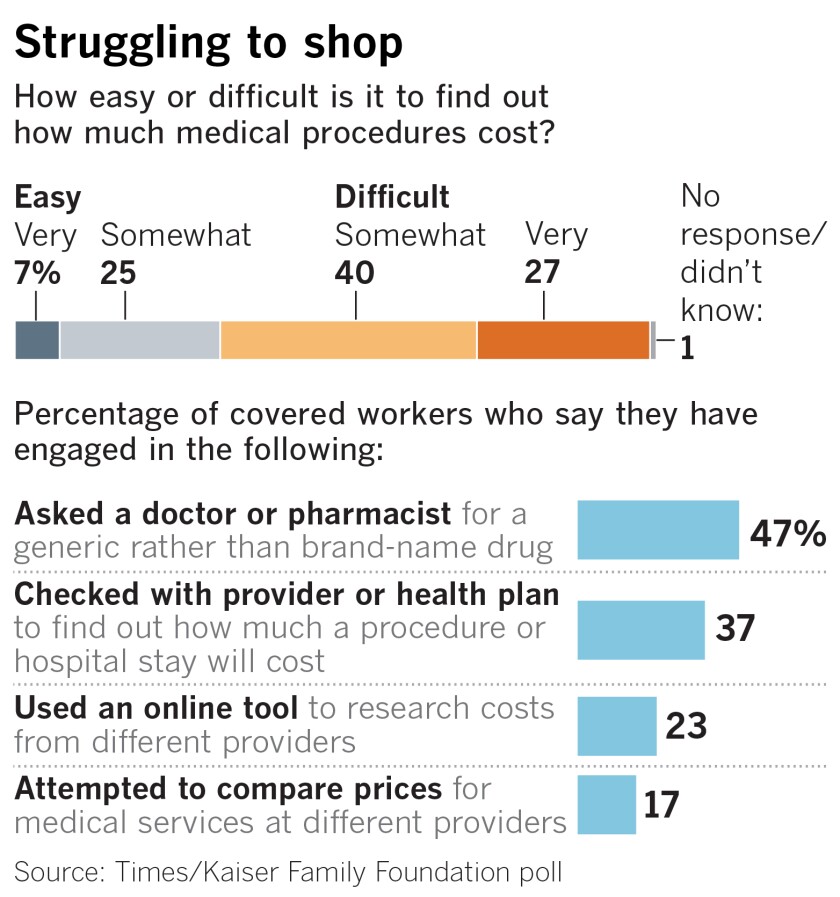

Just 1 in 6 covered workers even tried to shop for the best price for a medical service in the previous year, according to a nationwide poll

conducted for this project by The Times and the nonprofit Kaiser Family

Foundation. Two-thirds of workers with job-based coverage said finding

the cost of a medical treatment or procedure was somewhat or very

difficult.

Meantime, prices for medical care and prescription

drugs haven’t moderated, as advocates of high-deductible insurance

predicted. Instead, they have soared.

The average price of a knee replacement, for example, shot up nearly

80% between 2003 and 2017, increasing at more than double the rate of

overall inflation, a Kaiser Family Foundation analysis of commercial insurance data found.

These

price hikes are crushing insured Americans: 1 in 6 workers with

job-based benefits in the Times/Kaiser Family Foundation poll reported

that they had to make a “difficult sacrifice” in the past year to pay for healthcare, such as cutting back on food and other essentials.

“We overestimated the ability of consumers to be good stewards of

their healthcare dollars in a system that is very unfriendly to

consumers, and underestimated the support they would need from us,” said

Dr. Marcus Thygeson, a former Blue Shield of California executive who

worked on early efforts to develop so-called consumer-directed health

plans.

Early champions of high-deductible health insurance —

including benefit consultants, conservative health-policy advocates and

Republican politicians such as former House Speaker Newt Gingrich —

promised something very different when they sold employers on shifting

more costs onto workers in the early 2000s.

Rebecca Grimm plays with her 2-year-old daughter, Amelia, and husband, Mark, at their home in Westfield, Ind.

(Leah Klafczynski / For The Times)

“When consumers apply pressure on an industry, whether it’s retailing

or banking, cars or computers, it invariably produces a surge of

innovation that increases productivity, reduces prices, improves quality

and expands choices,” Harvard Business School professor Regina

Herzlinger wrote in an influential 2002 essay. Herzlinger became a leading proponent of having patients put more “skin in the game.”

By some measures, healthcare markets appeared ripe for an intervention.

Then and now, prices for the same medical service can vary dramatically from one hospital or doctor’s office to another.

In

Philadelphia, for example, the price of a colonoscopy ranges from less

than $1,000 at some hospitals to nearly $4,000 at the most expensive,

researchers at the Health Care Pricing Project found by analyzing commercial health insurance data from around the country.

Similarly,

the lowest-priced hospitals in Houston billed as little as $15,000 for a

knee replacement, while the costliest charged more than $35,000.

That kind of price variation — which has little relationship to

quality, according to a growing number of studies — spawned online tools

that were supposed to help patients find the most economical place to

get care.

“There was this notion that if people could figure out

where to buy the cheapest Kleenex, they could pick doctors and

hospitals, too,” said Dr. Arnie Milstein, medical director of the

California-based Pacific Business Group on Health, an organization of large companies including Boeing, Safeway, Walmart and Wells Fargo.

Finding medical care is more complex than choosing facial tissue, however. And few workers ended up using these tools.

In one study

of nearly 150,000 people covered by two large national employers, only

about one in 10 who could shop for price information did, even if they

had a high-deductible plan. And use of the tool was not associated with

lower healthcare spending.

In the Times/Kaiser Family Foundation

survey, only about a quarter of workers with job-based coverage reported

using an online cost tool.

Americans show little inclination to

find the best deal even for a basic medical service like an MRI scan,

which can be as much as five times more expensive in one facility than

in another, another recent study found.

Researchers

analyzing commercial insurance data from tens of millions of Americans

reported only 14% of patients went to the lowest-cost MRI within a

30-minute drive of their house. Patients on average passed six

lower-priced MRI facilities on their way from home to the place where

they had the imaging, the study found.

Many Americans don’t want to have to shop for healthcare, preferring to let their physicians guide their care.

“We

pretty much go where we’re comfortable. We’re not looking for the

cheapest doctor,” said Jim Morrissey, 39, a food service manager who

lives near Harrisburg, Pa. “I’m loyal to the doctors I trust.”

Americans’ lack of enthusiasm for medical shopping also reflects how little information is available about prices.

The wildly inaccurate estimate that Grimm got for her procedure in Indiana is hardly unique.

When researchers in 2011 and 2012 called a sample of 122 hospitals

across the country to get a price for a hip replacement, a common and

usually straightforward elective surgery, only 19 were able to provide a

complete estimate, including the hospital and physician costs.

Even

when the researchers called a physician’s office separately to get

doctors’ fees, they could get a full estimate less than half the time.

Four years later, when a second group of researchers repeated the exercise with the same hospitals, the results were worse: Only eight gave a complete estimate.

Information on the quality of medical services, which patients would need to be informed shoppers, is even harder to come by.

Hospitals

that can provide a single price for something like a hip replacement

typically “bundle” all the services required for the procedure,

including the surgeons’ fees, the anesthesia, the use of any medications

and the cost of using hospital facilities such as the operating and

recovery rooms.

But that’s not the way most medical care in the

U.S. is billed. Rather than a single price, hospitals, doctors and other

medical providers rely on approximately 10,000 individual billing codes

to charge for services. A consumer who wanted to shop would have to

price each service separately.

When Grimm finally succeeded in

getting an itemized bill from the surgical center, she and her husband

were floored by the 23 individual charges, including: $65.23 for

Lidocaine, an anesthetic; $133.28 for two injections of Ondansetron, a

drug to prevent nausea and vomiting; $413 for oxygen; $132.80 for a

liter of sterile water.

There were two charges for the surgery itself of $2,380 and $9,782. Grimm’s brief stay in the recovery room cost $720.

“How in the world were we supposed to know how to shop for all that?” she said.

Herzlinger,

the Harvard Business School professor, said in a recent interview that

the consumer revolution she envisioned didn’t occur because hospitals

and doctors resisted efforts to make healthcare pricing more

transparent.

“There are a lot of people who don’t want this

information revealed,” she said, adding she never believed

consumer-directed healthcare required high deductibles. “I personally

think deductibles are too high,” she said.

Shopping becomes even more unrealistic for a person with an emergency — chest pain, for example, or an automobile accident.

Nor

would a patient have either the ability or much incentive to compare

costs for a complex disease like cancer that may require months of

chemotherapy, radiation and other expensive and often-unpredictable

medical services, the price of which would likely exceed even the

highest deductibles.

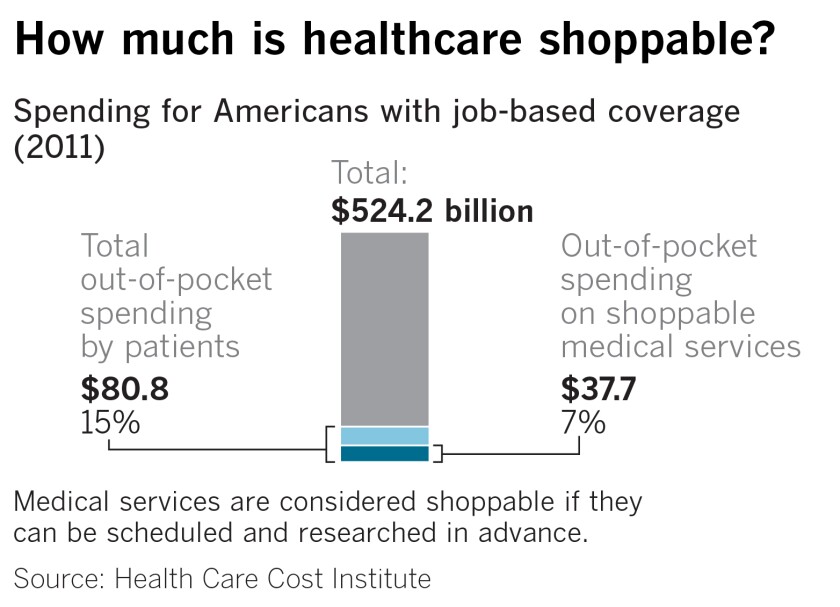

By one estimate

by the Health Care Cost Institute, just 7% of total healthcare spending

for Americans with job-based coverage was on medical services that

could be considered “shoppable” because the service required an

out-of-pocket payment and the procedure could be researched in advance.

“The

fact is very little medical care is shoppable,” said David Newman, the

institute’s former director, noting that medical care is not like other

services that Americans typically buy.

“We become good shoppers

when we are repeat shoppers,” he said. “If you buy a new car every three

years, you can become an informed shopper. There is no way to become an

informed shopper for your appendix. You only get your appendix out

once.”

Julie Hernandez, a 61-year-old graphic designer in Oregon,

discovered the limits of medical shopping the hard way when she went to a

dermatologist earlier this year to get a small cancerous growth removed

from her nose.

Sensitive to costs, in part because she had a

high-deductible plan, Hernandez tried to get estimates from several

medical offices in her area around Medford. She selected what seemed to

be the lowest-cost option, even though she was told the procedure might

cost $3,000 to $8,000.

Midway through the surgery, after the

doctor had removed several layers of skin from Hernandez’s nostril to

take off the cancerous tissue, the doctor asked Hernandez as she lay on

the operating table whether she wanted to have the wound closed with

skin from her cheek or from another part of her nose.

“I had a

gaping hole the size of a dime in my nose,” she said. “At that point,

money didn’t come into play. I went with the option the doctor said was

best.”

Hernandez later got a bill for $5,568.

As for the

Grimms, they ultimately got a discount for Rebecca’s procedure after she

spent months filling out forms and negotiating with the surgery center.

They ended up paying $2,300.

But as she prepared to have a second

baby this summer, the couple didn’t even try to shop for the best

price, though they knew they’d have to pay thousands of dollars for the

delivery. https://www.latimes.com/politics/story/2019-09-25/shopping-medical-care-lots-of-luck?

Nurses in Four States StrikPush for Better Patient Care

Registered nurses with National Nurses United say current nurse-to-patient ratios do not allow for the best possible care.

by Aimee Ortiz - NYT - September 20, 2019

Thousands

of nurses across the country went on strike Friday morning, pushing for

better patient care by demanding improved work conditions and higher

pay.

About 6,500 National Nurses United members at 12 Tenet

Healthcare hospitals in California, Arizona and Florida organized a

24-hour strike, which began at 7 a.m., to protest current

nurse-to-patient ratios that they contend are burning out employees and

making it difficult to provide the best possible care.

In

Chicago, more than 2,000 nurses walked off the job after contract

negotiations between National Nurses United and the University of

Chicago Medical Center broke down on Wednesday night.

“We’re here

to advocate for our patients,” said Yajaira Roman, an intensive care

unit nurse who works for Tenet Healthcare’s Palmetto General Hospital in

Hialeah, Fla., and a member of the union’s bargaining committee. “We’re

pretty much urging the hospital to invest in the nurses and take steps

to strengthen our recruitment and retention of experienced nurses at the

hospital.”

“It’s very difficult to give a patient optimal care if our patient ratio is so high,” Ms. Roman said.

Research

shows that with “every patient over four assigned to one nurse in a

medical surgical unit, there’s an increase in mortality of 7 percent per

patient,” she said, noting her hospital currently allows for eight

patients to one nurse.

A strong contract between the union and

the hospital, Ms. Roman said, helps ensure that patients receive the

best possible care. National Nurses United members in all four states

have been working either without a contract or under an expired one. The

strikes in Arizona and Florida are the first by registered nurses in

those states, the union said.

Fawn Slade, a registered nurse at St. Joseph’s in Tucson and a union member, echoed the concerns about patient ratios.

“If we did not feel that this was necessary to get a strong contract, we would not be out here doing this,” Ms. Slade said.

In

Arizona alone, 37,000 people with active registered nurse licenses

don’t work as nurses, Ms. Slade said. “We are hopeful that this strong

contract will bring those nurses back to the bedside.”

In a

statement on Friday, Tenet Healthcare said the company’s top priority

“is providing our patients with excellent care, as always.”

“Our

hospitals are fully operational with dedicated and experienced nurses,

caregivers and supporting staff delivering high-quality, compassionate

care throughout today’s one-day strike,” a Tenet spokeswoman said.

The

hospital system did not give specific nurse-to-patient ratios, but the

spokeswoman said, “Our hospitals are staffed appropriately.”

“The

safety of our patients is paramount and staffing decisions are made to

support this based on acuity and individualized needs of each patient,”

she said.

The University of Chicago Medical Center also brought in

temporary nurses to cover its gaps in staffing during the one-day

strike, contracting them for five days — a move union members saw as

retaliation for the demonstration.

“They chose to lock us out for

these five days,” said Talisa Hardin, a registered nurse at the

center’s burn unit. She said that the hospital deactivated the badges of

striking nurses and removed their parking privileges, and that meant

that nurses would lose five days of pay, Ms. Hardin said.

Debi

Albert, the hospital’s chief nursing officer, said the temporary

nurses, who came in from across the country, would come in only for a

five-day contract.

“The competition for those relief nurses was

quite high,” Ms. Albert said. The staffing agency used to hire the

temporary nurses, she said, indicated to the hospital that “if we wanted

to safely staff the hospital for one day, we had to commit to those

nurses for five days, or they would not travel.”

In addition to

hiring the temporary nurses, the University of Chicago Medical Center

moved several patients out of the neonatal intensive care unit, the

pediatric intensive care unit and the intensive care unit. The

hospital’s emergency room is currently on diversion, meaning ambulances

must find somewhere else to go, even if it is the closest one.

“It’s

heartbreaking” that they’re moving patients, Ms. Hardin said. “You work

in a place and you think that there’s values and that what you do

matters, and they do things like take your patients away.”

The

nurses at the University of Chicago Medical Center face unsafe working

conditions daily, according to Ms. Hardin. She said that units often

borrow supplies, equipment and even staff from one another just to make

ends meet.

“It’s kind of a robbing-Peter-to-pay-Paul situation,” Ms. Hardin said.

The University of Chicago Medical Center, through a spokeswoman,

rejected the notion that the hospital was inadequately staffed.

“As

in any hospital, we often see unpredictable and sudden increases in

demand for care within our inpatient units,” she said. But she noted

that the hospital has a group of nurses who can shift between units

depending on need.

Speaking in a video

message before the strike, Sharon O’Keefe, president of the University

of Chicago Medical Center, said Thursday, “We’re disheartened that we

had to get to this point.”

The hospital “worked long and hard

negotiating with the help of a federal mediator and had hoped union

leadership would meet us halfway,” she said. “We now have to focus our

efforts on safely operating our hospitals and caring for the patients

who depend on us.”

Friday’s nurses’ strikes add to a growing list

of union actions that have taken place across the nation recently,

including the continuing United Auto Workers strike and the Los Angeles teachers’ strike earlier this year. https://www.nytimes.com/2019/09/20/us/nurse-strike.html?

On

Monday, the United Nations High-Level Meeting on Universal Health

Coverage took place in New York, convening leaders from all countries to

reinforce political commitment toward health care for all by 2030.

Dozens

of countries have universal coverage models in place, and many low- and

middle-income countries are making great strides; ironically, the

meeting’s host country, the United States, is a strong outlier.

A large percentage of the United States’ gross domestic product is spent on health care, yet life expectancy and health outcomes compare poorly with other high-income countries spending much less. Although fewer Americans live in poverty today, an increased number live without health insurance. A need for emergency care may put these families in financial distress or, worse, on the streets.

On

Monday, the United Nations High-Level Meeting on Universal Health

Coverage took place in New York, convening leaders from all countries to

reinforce political commitment toward health care for all by 2030.

Dozens

of countries have universal coverage models in place, and many low- and

middle-income countries are making great strides; ironically, the

meeting’s host country, the United States, is a strong outlier.

A large percentage of the United States’ gross domestic product is spent on health care, yet life expectancy and health outcomes compare poorly with other high-income countries spending much less. Although fewer Americans live in poverty today, an increased number live without health insurance. A need for emergency care may put these families in financial distress or, worse, on the streets.

If

not these, then what are strong enough incentives to protect the

Affordable Care Act as a steppingstone to move toward health care for

all?

‘Value’ of Care Was a Big Goal. How Did It Work Out?

by Austin Frakt - NYT - September 23. 2019

A period of Medicare innovation has resulted in more ‘singles than home runs.’

“It

doesn’t mean that the vast majority of the care Medicare purchases is

linked to actual value,” said Sherry Glied, a health economist, and dean

and professor at the Wagner School of Public Service at N.Y.U. “We

don’t even know what we mean by value. How do you pay for something when

you don’t know what it is?”

Different programs have different notions of “value.” Medicare’s Hospital Readmissions Reduction Program,

established in 2010, penalizes hospitals that have high rates of

readmissions for certain illnesses. Although hospitals can lose only up

to 3 percent of payment, 100 percent of their payment is considered

“tied to value.”

The key is whether programs like this improve

health care quality or reduce health care spending. The Hospital

Readmissions Reduction Program has been extensively examined, with

studies drawing different conclusions. Initial analyses of the program suggest it is responsible for reducing hospital readmissions, saving Medicare billions of dollars a year.

But some later studies found that these reports of success were overstated, among other concerns. Some studies found that reduced hospital readmissions were associated with increased risk of death, though not all studies

agree on this point, and experts disagree on the value of the program.

What is clear is that the program has had a smaller impact on hospital

readmissions than originally thought — perhaps reducing them by as

little as one-third of a percentage point.

Another Medicare value-based payment program is considerably more broad. The Hospital Value-Based Purchasing Program

was introduced in 2011 and rewards or penalizes hospitals based on

mortality; infection rates; patient experience and safety; cost; and

other measures of quality — 20 in all. Typical bonuses or penalties are a fraction of 1 percent of a hospital’s total Medicare payments.

A study published in

Health Services Research compared about 2,800 hospitals in the program

with about 300 exempt from it. The study found no effect from financial

incentives of the program on quality of care or patient satisfaction.

But the study included data only up to nine months after the program’s

start, and it may take hospitals longer to make measurable changes.

Another study, published in BMJ, looked at outcomestwo

and a half years after the start of the Hospital Value-Based Purchasing

Program. It found no differences in changes in mortality rates between

hospitals in the program versus those exempt from it. And another study,

published in Health Affairs, found no evidence that the program improved patient satisfaction up to three years after implementation.

Jose

Figueroa, a physician at Brigham and Women’s Hospital in Boston, and an

assistant professor of medicine at Harvard Medical School, was an

author of both of these longer studies. “So far, there’s no evidence the

program has improved quality or patient satisfaction,” he said. He

ticked off some possible reasons: “The financial incentives are too weak

to drive any meaningful changes across hospitals. The program’s design,

with numerous measures across different domains, makes it hard for

hospitals to understand what to focus on.”

Medicare has achieved

greater success with programs that have raised the stakes — ones that

have put hospitals and health care organizations at greater risk of

financial loss or have offered prospects for larger financial gain.

One

popular approach, called “bundled payments,” pays health providers one

amount for all of the care for a certain condition within a certain

period — like 90 days for hip replacement care. There is evidence that some of these programs can save money without reductions in quality, although design details matter.

“Bundled

payments are a straightforward way to make hospitals consider all the

costs they are responsible for,” said Adam Sacarny, assistant professor

with Columbia’s Mailman School of Public Health. “The evidence suggests

they encourage hospitals to treat patients more efficiently, although

the cost savings are at least partly offset by extra payments to

hospitals to reward them for saving money in the first place.”

Another

approach — accountable care organizations — also takes many forms. What

they have in common is they offer health care organizations the chance

to earn bonuses for accepting some financial risk, provided they meet a

set of quality targets. Many studies of accountable care organizations (A.C.O.s) have found they reduce spending with no quality degradation.

“There

is strong evidence that, on average, Medicare A.C.O.s save a modest

amount of money,” said Alice Chen, assistant professor at the University

of Southern California Sol Price School of Public Policy.

Although accountable care organizations have saved a few percent of Medicare spending, the amount varies

by program design. “We’ve found that A.C.O.s that are physician groups

as opposed to big hospital systems have produced more savings,” said

Michael McWilliams, a professor at Harvard Medical School and a general

internist with Brigham and Women’s Hospital. “That’s because physician

groups don’t erode their own revenue when they keep their patients away

from hospitals.”

So over all, is Medicare moving toward higher

value? “There has been some progress, but even the most generous read of

the evidence is very far below the projections made by fans of value-based payment before the A.C.A.,” Ms. Glied said.

Robert

Berenson, a fellow at the Urban Institute, agreed: “Value payment

overemphasizes performance measurement, but even so, it’s been

disappointing. We simply lack good metrics that can’t be gamed or evaded

by most targeted providers.”

But some are more optimistic. “The

successes are more like singles than home runs,” said Michael Chernew, a

health economist with Harvard Medical School. “Despite the modest

results, I think some approaches, like A.C.O.s, are a foundation for

future improvements.”

Paying for health care value is a popular slogan, but Medicare is still figuring out how to do it. https://www.nytimes.com/2019/09/23/upshot/medicare-health-value-costs.html?

Pelosi Offers Medicare Negotiation Plan to Curb Drug Prices

by Associated Press - September 19, 2019

WASHINGTON — House Speaker Nancy Pelosi, trying to seize

the agenda on a top consumer issue, announced an ambitious prescription

drug plan Thursday that would allow Medicare to negotiate prices for

seniors and younger people.

The proposal would direct Medicare to

bargain over as many as 250, but no fewer than 25, of the costliest

drugs. Insulin is on the list. Drugmakers that refuse to negotiate could

face steep penalties. Companies that raise prices beyond inflation

would have to pay rebates to Medicare.

The plan would limit copays

for seniors covered by Medicare's "Part D" prescription drug program to

$2,000. Medicare-negotiated prices would be available to other buyers,

such as employer health plans.

It's shaping up as a high-stakes

gamble for all sides in Washington. Polls show that high drug prices

have Americans worried, and regardless of party affiliation, they want

Congress to act. As a candidate, President Donald Trump called for

Medicare negotiations but later seemed to drop the idea.

Pelosi, D-Calif., said her goal is a deal that Trump can sign onto and that could pass the GOP-controlled Senate.

"We

don't want a political issue at the polls," Pelosi said at a news

conference. "We want a solution in Congress, and we want it now."

Weighing

in on Twitter, Trump said, "Let's get it done in a bipartisan way!"

Unlike other Republicans, he refrained from criticizing Pelosi's bill

and said "it's great" to see her out with a plan. But he said he

preferred a bipartisan Senate bill being pushed by Iowa Republican Chuck

Grassley.

In the Senate, Republican John Cornyn of Texas said

Pelosi's proposal "has absolutely no chance —zero, zip, nada" of

passing. Some House Republicans quickly dismissed it as "socialism."

The

2003 law that created Medicare's prescription drug benefit barred the

program from negotiating prices, a restriction Democrats have long

opposed. Most Republicans say they believe price negotiations are best

left to private players such as insurance companies.

The

industry group Pharmaceutical Research and Manufacturers of America

said Pelosi's plan was "radical" and would usher in an era of government

price-setting that would "blow up" the current system, stifling

innovation. But health insurers called the plan "bold reform" and

hospitals said it takes "significant strides toward reducing

out-of-control drug prices." Public Citizen, a consumer group on the

political left, said the bill didn't go far enough because it left

intact drugmakers' monopoly on new medicines.

A leading House

progressive, Texas Democrat Lloyd Doggett, agreed that more is required.

"This new bill was promoted as a way to sway President Trump and a

reluctant Republican Senate," said Doggett. "I await their embrace."

While

the legislation leans left politically it also incorporates ideas from

the Trump administration and from Republican and Democratic senators — a

signal Pelosi wants a deal.

Pelosi's proposal would:

—

authorize Medicare to negotiate prices for up to 250 drugs with the

greatest total cost to society. That includes pharmacy drugs under the

Part D prescription benefit, and Part B medications dispensed in

doctors' offices, such as many cancer drugs. Medicare would negotiate

for as many drugs as possible on a list refreshed annually, but no fewer

than 25. The maximum price would be determined using a blend of

international prices, similar to a more limited proposal from the

administration. Drug companies that balk at making a deal would face

penalties that start at 65% of sales for the drug at issue, and escalate

if they hold out.

— require drugmakers to pay rebates to Medicare

if they raise prices beyond the increase in inflation. That idea

resembles the plan from Sens. Grassley and Ron Wyden, D-Ore. Their

proposal has cleared a key committee, with Trump's support. But many

Senate Republicans oppose inflation rebates, and it's unclear what

Majority Leader Mitch McConnell, R-Ky., plans to do next.

— limit

what seniors pay out of pocket for their medications to $2,000 a year.

Currently, Medicare's pharmacy benefit has no cap on copays, and the

advent of drugs costing hundreds of thousands of dollars a year has left

some seniors saddled with bills that rival a mortgage payment. An

out-of-pocket limit is part of the Grassley-Wyden bill and is backed by

the administration.

For now, criticism of the industry — from Trump and lawmakers of both parties — appears to be having an effect on prices.

The

Commerce Department's inflation index for prescription drug prices has

declined in seven of the past eight months, which is highly unusual.

That index includes lower-cost generic drugs.

For brand-name

drugs, a recent Associated Press analysis shows prices are still going

up on average, but at a slower pace. Costly brand-name drugs that

translate to steep copays are the top concern for consumers.

The

AP analysis found that in the first seven months of 2019, drugmakers

raised list prices for brand name medicines by a median, or midpoint, of

5%. That's a slowdown. Prices were going up 9% or 10% over those months

the prior four years.

Still, there were 37 price increases for every decrease in the first seven months of 2019.

“It’s clear now that the idea definitely hasn’t borne fruit,” Quincy

continued. “It hasn’t made people feel more confident seeking care. It

hasn’t led to better value. And it’s had terrible consequences on

patients’ ability to afford care.”

“It’s clear now that the idea definitely hasn’t borne fruit,” Quincy

continued. “It hasn’t made people feel more confident seeking care. It

hasn’t led to better value. And it’s had terrible consequences on

patients’ ability to afford care.”

No comments:

Post a Comment