SUGAR The World Corrupted: From Slavery to Obesity By James Walvin 325 pp. Pegasus Books. $27.95.

Sweets have invaded the English language the way they have invaded our diet, with almost universally positive connotations. Sweet love, sweet people and sweet deals all suggest pleasant experiences, as do the sugary confections that grace our tables and fill our stores. James Walvin’s new book, “Sugar: The World Corrupted: From Slavery to Obesity,” will thoroughly disabuse you of such agreeable associations and may make you reluctant to reach for something sweet. Sugar, he shows, is a blood-soaked product that has brought havoc to millions and environmental devastation to large parts of the planet, premature death to the poorest populations in many parts of the world and huge health costs for societies from the United States to India. After reading this book the mere mention of sugar should make you think of slavery and cavities, imperialism and obesity — and remind you to check the label on the products you consume.

Walvin, the author of several books on slavery, takes his readers on a roller-coaster ride through 500 years of history. Sugar, he shows, was rare for most of human history, with sweetness largely derived from fruits and honey. Sugar was believed to have healing properties and in much of the world it was dispensed by apothecaries; consumption of small quantities of sugar was the prerogative of elites. Then, in the 16th century, Europeans seized large territories in the Americas and quickly dedicated much of that acreage to sugar cane. By killing off local inhabitants and enslaving Africans to do the backbreaking labor of tending the sugar plant, European settlers managed to build a huge production complex. Hungry for power and profit, they turned the fertile soils of Brazil, Barbados, Guadeloupe, Jamaica, St. Domingue and other places to the growing of sugar for European markets by slave labor, producing extraordinary wealth in cities like Bristol, Bordeaux and Boston, and unimaginable misery for millions of enslaved workers.

Sugar, Walvin argues, was the cutting edge of global capitalism, with the plantations among the largest business enterprises, the most significant sources of profit and, in light of their highly regimented discipline, the most modern work sites. As a major share of the total trade of both 18th-century France and Britain, sugar lubricated the world economy and provided nutrition to the growing number of people who worked in cities and industry. Sugar catalyzed some of the first waves of globalization — notably in British North America, which entered the world economy as a supplier of goods to the Caribbean sugar complex and a processor of its harvest. Boston, as much as Barbados, is sugar’s offspring.

As sugar streamed from the Caribbean, consumption grew. The European elite consumed ever-larger quantities — their rotting teeth in full view of their contemporaries, although discreetly hidden by their portraitists. By the 19th century, the working class in Europe and North America was sweetening its tea and coffee, and putting jam on its toast; by century’s end, it was breakfasting on sugary cereals. Fantastic quantities of sugar, in all its forms, kept stomachs full and workers productive. In 1770, rum — made from sugar cane — provided possibly one-quarter of the caloric needs of British North America. By the mid-20th century, the average annual consumption of sugar in Britain was an astonishing 110 pounds per person. “The fruits of slave labor,” Walvin writes, “had thoroughly permeated the Western world.” Even with slavery abolished in the British and French Caribbean, North Atlantic demand and investments allowed for another huge expansion of sugar slavery, this time in Cuba.

When slavery came to its slow end in the 19th century, the geography of sugar shifted. Brutalized indentured workers from India and China took up sugar production in Guyana and Fiji, Mauritius and Trinidad. Beet sugar producers in Germany and the American Midwest gained market share. And by the late 20th century, American corn growers were feeding huge quantities of high fructose corn syrup into global markets, enabling an ever-increasing quantity of sweeteners to be poured into soft drinks and cereals. Along the way, sugar turned out to be so important that governments came to regulate its production and trade, trying to secure inexpensive sugar for domestic markets and to bolster an ever more powerful food industry addicted to cheap sweeteners. Subsidies and tariffs, as well as imperial exertions on behalf of sugar-consuming industries, Walvin makes clear, shaped the global sugar market in ways that were good for industry and all too often harmful to workers and consumers. The result has been a wave of obesity that has moved at awe-inspiring speed across the planet — fattening up people from Europe to the United States, from India to Mexico, creating a global health crisis that suggests sugar is as toxic as tobacco. If current trends continue, Walvin observes, the majority of the British and American population may be obese by 2050.

“Sugar” is an entertaining, informative and utterly depressing global history of an important commodity. It takes its cues from histories of commodities like salt, tobacco and cotton and makes good use of the possibility inherent in this approach, especially the ability to link diverse developments in distant parts of the world over long time spans. It is less analytically sophisticated than some of its predecessors, and it enters a field — sugar studies — built on Sidney Mintz’s magnum opus “Sweetness and Power,” arguably the book that started the recent boom in commodity studies, and one that Walvin often cites. What Walvin adds to this literature is accessible prose and a more expansive view that focuses on the contemporary moment and, especially, the public health implications of a world addicted to sugar.

“Sugar” could have used another round of edits — it is maddeningly repetitive. Its numbers are often vague, and trajectories — of sugar consumption, for example — would be clearer if shown in a table or graph. Walvin’s arguments are morally forceful, but their lack of precision and specificity makes them analytically nebulous. “Sugar” also reads almost like two books — one focused on slavery, the other on obesity. And despite its global scope, the book remains beholden to a Eurocentric perspective that has little to say about pre-European systems of sugar production in Asia, glosses over the enormous expansion of systems of indentured labor in sugar-growing Asia, and is weak on sugar consumption in places like India, Barbados or Senegal — all currently suffering from a diabetes epidemic. Perhaps it is true, as Walvin asserts, that sugar tainted “all involved wherever it took root,” but how it tainted places and people, and who did the tainting, and how conditions changed over the past 500 years are often left unexplained, as are any resulting lessons we might learn.

By alerting readers to the ways that modernity’s very origins are entangled with a seemingly benign and delicious substance, “Sugar” raises fundamental questions about our world. It does not resolve all those questions, but it provides enough information for its readers to begin to see some answers and to see how troubling and disconcerting they are.

Medicare Advantage Is About to Change. Here’s What You Should Know.

Medicare Advantage plans will be allowed to cover adult day care, home modifications and other new benefits. But they may not be available to all enrollees every year.

by Paula Span - NYT - July 20, 2018

Did you fall in the bathroom and fracture your hip? Medicare, if you have it, will pay thousands of dollars for surgery to repair the injury and thousands more for your resulting hospital stay and rehab in a nursing home.

For decades, public health experts, doctors, patients and families have lamented this narrow, often counterproductive approach to older Americans’ health care.

“You don’t want somebody with asthma rushing to the emergency room with a breathing problem that could have been prevented with an air conditioner,” said Tricia Neuman, who directs the Medicare policy program at the Kaiser Family Foundation. Yet Medicare covers costly emergency medicine, not window units.

When Medicare’s open enrollment period begins on Oct. 15, the private insurers that underwrite Advantage plans — which already lure seniors with things traditional Medicare can’t cover, like eyeglasses, hearing aids and gym memberships — will be free to add a long list of new benefits.

Among those the Centers for Medicare and Medicaid Services will now allow, if they’re deemed health-related: Adult day care programs. Home aides to help with activities of daily living, like bathing and dressing. Palliative care at home for some patients. Home safety devices and modifications like grab bars and wheelchair ramps. Transportation to medical appointments.

“This will potentially help people stay in their homes longer and not have to go to institutions,” Seema Verma, the C.M.S. administrator, said in an interview. “You could provide a simple device or a home modification that could mean the world to a patient, but plans weren’t allowed to do that in the past.”

In 2020, thanks to Congress, the list of possible benefits could expand still further. Incorporated in the budget signed by President Trump, the Chronic Act is intended to help people manage conditions like heart failure and diabetes, in part by authorizing telehealth programs. It, too, will work through Medicare Advantage.

These actions could represent substantial change. Dr. Diane Meier, a geriatrician who directs the Center to Advance Palliative Care at the Icahn School of Medicine at Mount Sinai in New York, called them “a tectonic plate shift.”

“What I find most fundamental is the recognition, by C.M.S. and Congress, that this bright line between ‘medically necessary’ and things necessary to maintain health — like proper nutrition and transportation to a doctor’s office — is an illusion,” she said.

“Failure to invest in simple things like safe housing and transportation means you will invest in hospitalization and emergency room visits” at far higher costs, she added.

Yet celebration may prove premature. Many questions remain about how insurers will respond to the legislative opening.

“We have concerns about where all this is heading,” said David Lipschutz, senior policy lawyer for the Center for Medicare Advocacy. “The scales really are being tipped in favor of Medicare Advantage, with unknown consequences.”

A primer: Medicare Advantage funnels federal dollars to private insurers — United Healthcare and Humana dominate the market — who must cover all Medicare services but can also dangle a number of bonus benefits.

Dentistry, for instance. Original Medicare doesn’t cover it, but with Medicare Advantage, “some plans cover cleaning,” Dr. Neuman said. “Some cover cleaning and extractions. Some might cover a crown every five years.” Now, such extras could expand.

The plans — including premiums and benefits — already vary widely. Enrollees pay the monthly Part B premium ($134 this year, though higher income people pay more) and may pay an additional Medicare Advantage premium. Last year, according to Kaiser Family Foundation analysis, that ran an average $36 a month, including Part D drug coverage.

So Medicare Advantage plans may appear cheaper than standard Medicare combined with Part D and a supplemental Medigap policy — though with co-pays, deductibles and drug formularies, they may not be.

“The key trade-off is that they generally operate with a restricted network of providers,” Dr. Neuman said. Most involve health maintenance or preferred provider organizations.

The proportion of Medicare beneficiaries who opt for these plans has climbed steadily, nonetheless, to 33 percent last year from about 16 percent in 2006. In 10 years, the Kaiser Family Foundation calculates, that figure will reach 42 percent.

“The Medicare Advantage program is very successful,”Ms. Verma said. “We see consistently high marks for satisfaction.”

Additional benefits could accelerate that growth, and Ms. Verma said she hoped they would.

“When people look at making a choice between enrolling in Medicare Advantage or the traditional program, they’re going to see this as a tremendous opportunity,” she predicted.

The immediate changes may be modest. Because C.M.S. announced its new rules in April, and insurers had to submit proposals last month, “there was very little time for the plans to mobilize,” said John Gorman, a consultant for many Medicare Advantage insurers. He expects more significant differences in 2020 and beyond.

And then?

What particularly troubles skeptics is that these intended improvements completely bypass most Medicare beneficiaries — the two-thirds who have stuck with traditional Medicare.

You can see why it’s played out this way. Funding for Medicare Advantage programs is capped: C.M.S. provides a set amount, which private insurers can use to provide whichever supplemental benefits they choose, theoretically stoking competition. Any increased costs will be borne by the plans and their enrollees, not the federal budget

“Republicans have always been some of Medicare Advantage’s biggest boosters,” Mr. Gorman noted. “In effect, you’re shifting deficits onto the private sector.”

As for the remaining Medicare population, “advocates are hoping this provides a pathway to expanded services for all beneficiaries,” Dr. Neuman said.

But Ms. Verma said that could raise costs and would require Congressional action. Moreover, C.M.S. also relaxed the requirement thatAdvantage plans must provide the same services for all enrollees. Now, they can furnish benefits to those with certain health conditions, not to everyone.

Thus, a plan can tailor its offerings, providing adult day programs, say, only for people with dementia. “If you see a plan advertising certain supplemental services, that’s not necessarily a guarantee the services will be available to you,” Mr. Lipschutz said.

In fact, since the more flexible rules permit but don’t require any of these new benefits, and since insurers won’t reveal the particulars until October, it’s not yet clear what they will offer — or whether these changesmight weaken traditional Medicare.

Advantage plans could provide certain benefits one year, then withdraw them the next, in the same way that drug coverage shifts. As for providers, “who’s in-network and who’s not changes by the minute,” Dr. Meier said.

Once they enroll, few people ever switch. “People find it very tedious, and they have little confidence in their ability to understand how plans differ,” Dr. Neuman said.

Now, those choices will grow still more complicated. The independent counselors at the free State Health Insurance Assistance Programs should probably brace for waves of new clients.

“It’s all going to require experimentation,” Dr. Meier said.

Still, a move to more broadly support the health and well-being of an aging population could mark an important turning point.

“Could” is the key word. “It’s only a possibility,” Dr. Meier said. “But it wasn’t a possibility before.”

A Vote Expanded Medicaid in Maine. The Governor Is Ignoring It.

by Abby Goodnough - NYT - July 24, 2018

Medicaid expansion is also emerging as a potent issue in gubernatorial and congressional races in Florida, Georgia and Kansas, among others. Here in Maine, where supporters of expansion have sued the LePage administration over its failure to act, the legal conflict has spilled into the race to replace Mr. LePage, who is finishing his second term.

Janet Mills, the state’s attorney general, is also the Democratic candidate for governor. She refused to represent the administration in the court case, leaving it to a private lawyer from Boston.

Ms. Mills said in an interview last week: “If for some reason Medicaid expansion isn’t implemented in the next five and a half months, I will do it on Day 1.”

Her Republican opponent, Shawn Moody, a businessman, sides with Mr. LePage. His spokeswoman — who is Mr. LePage’s daughter, Lauren — said in an emailed statement on Thursday that if elected, Mr. Moody would “enforce the laws on the books, with appropriate funding from the legislature who under the constitution must pass all spending bills.”

Janet Mills, the state’s attorney general and also the Democratic candidate for governor. She has refused to represent the administration in the court case.Greta Rybus for The New York Times

A statement Ms. LePage recently shared with Maine reporters took a more colorful tone, saying in part, “Shawn will not risk the fiscal health of the state to expand welfare for nondisabled individuals, and will not support funding welfare by raising taxes, raiding the rainy-day fund, or using one-time budget gimmicks.”

On June 4, A Maine Superior Court judge last month ordered the LePage administration to submit a plan within a week for expanding Medicaid, chastising its “complete failure to act.” Unsurprisingly, the administration appealed, and the state’s highest court, the Maine Supreme Judicial Court, heard arguments Wednesday about whether the lower court’s order should be kept on hold, as Mr. LePage wants, until his appeal is resolved.

The question of how to pay for Medicaid expansion kept coming up, with the justices appearing reluctant to get involved.

Patrick Strawbridge, the lawyer representing the LePage administration, said the lower court had been wrong to order Mr. LePage to submit a plan binding his administration to pay its share for Medicaid expansion when the legislature hadn’t appropriated “a single penny” for it.

Lynnea Hawkins, with a 17-year-old son and a volunteer job, qualified for Medicaid, but without the expansion, she will lose coverage next year when he turns 18.Greta Rybus for The New York Times

That led James Kilbreth, a lawyer for the plaintiffs, to point out the legislature’s allocation last month of $60 million, using one-time surplus and tobacco settlement funds, to cover the first year of Medicaid expansion costs.

“You can’t have a circumstance in which the governor, after the legislature appropriates funds, is free to veto and veto and veto appropriations to fund the act,” Mr. Kilbreth said.

The legislature failed to override Mr. LePage’s veto of the spending bill because a bloc of House Republicans refused to join in. Mr. LePage has said he will not approve spending that raises taxes or relies on the state’s rainy day fund or “one-time funding mechanisms or budget gimmicks.” He recently suggested increasing a tax on hospitals to cover the state’s share of expansion costs — a funding stream that a number of other states that expanded Medicaid are using — but legislative leaders say they need to see a formal plan before deciding whether to support the idea.

Mr. LePage often points back to earlier state decisions to expand Medicaid, over a decade ago. Afterward, Maine struggled with budget shortfalls and fell behind on Medicaid payments to hospitals. After Mr. LePage took office, he paid the hospitals more than $200 million that they were still owed and reduced Medicaid eligibility. The new expansion would be different in that the federal government would pay significantly more of the cost.

Ms. Staples, the breast-cancer survivor who attended the oral arguments, works part time in food service at Bowdoin College. She pays $75 a month for subsidized private coverage through the Obamacare marketplace, plus a deductible, but is poor enough to qualify for Medicaid if it were expanded, she said. She gathered hundreds of signatures to help get Medicaid expansion on the ballot last year, then knocked on hundreds of doors to get out the vote as a member of the Maine People’s Alliance, a nonprofit organizing group. It was the first time voters anywhere got to decide the issue, and they approved it 59 percent to 41 percent.

“We shouldn’t have to be fighting this right now,” Ms. Staples said outside the marble-lined courtroom as throngs of summer tourists, oblivious to conflict, wandered the Old Port neighborhood outside. “We have 70,000 lives on the line here.”

Her friend Lynnea Hawkins, 38, said she relished the prospect of Mr. LePage going to jail over Medicaid expansion, however unlikely that might be. She has only a volunteer job, with the Maine People’s Alliance, where she and Ms. Staples both serve on the board. She qualifies for Medicaid now as the mother of a dependent child, but without the expansion, she will lose it next spring when her son turns 18.

“I want to be outside the jail with a nice chair and some popcorn, waving to him — ‘Bye, have fun!’” said Ms. Hawkins, who lives in Lewiston.

Lori Dwyer, the president and chief executive of Penobscot County Health Care, which runs nonprofit clinics in the Bangor area and treats 65,000 patients a year, 17 percent of whom are uninsured.Greta Rybus for The New York Times

Robyn Merrill, the executive director of Maine Equal Justice Partners, the advocacy group leading the lawsuit, said, “We don’t have an objective indication that anybody is going to have to go to jail.” But she added that if the Supreme Judicial Court ultimately enforced the lower court’s order and Mr. LePage still refused to budge, the plaintiffs would ask the court to find his administration in contempt.

Donna Wall, 61, a plaintiff in the lawsuit, is uninsured. She racked up $60,000 in debt after shattering her ankle when she fell on an icy sidewalk in Lewiston last December while delivering newspapers in the middle of the night, a job that paid her $150 a week.

A GoFundMe.com campaign raised more than $10,000 to help her. But Ms. Wall, who cares full time for her 20-year-old autistic twins and donates blood plasma for extra income, is eager for the security of Medicaid coverage. She applied for it on July 3, a day after the state was supposed to start covering the newly eligible population under the law.

“The governor has this preconceived notion that we’re lazy,” Ms. Wall said on Tuesday. “I would love for him to come and live with me a couple weeks, see what it’s like to take care of the boys.”

The expansion would cover anyone earning up to 138 percent of the federal poverty level, which equals about $16,700 a year for a single person and $34,600 for a family of four. Many health clinics that treat the poor are telling their patients to apply for Medicaid now even though they may not get coverage any time soon.

“We’re telling them to let us know if or when they get denied,” said Lori Dwyer, the president and chief executive of Penobscot County Health Care, which runs nonprofit clinics in the Bangor area and treats 65,000 patients a year, about 17 percent of whom are uninsured.

“Though I’m an incredibly optimistic person and always hold out hope,” Ms. Dwyer said, “I’m extremely discouraged.”

Last month, when Alexandria Ocasio-Cortez, a 28-year old political upstart and avowed socialist, upended a a powerful Democratic incumbent in a New York congressional primary, it helped return the word “socialism” to prominence in American political debates — though not necessarily in a good way.

Ocasio-Cortez quickly became a political punching bag for conservatives. Countless columns by conservatives and even moderate Democrats exorcised Ocasio-Cortez’s dystopian vision of an America in which everyone has access to health care, affordable housing, a quality education, paid sick and family leave, and a living wage.

Indeed, many of the criticisms of Ocasio-Cortez’s platform, which is not radical, not truly socialist, and is actually fairly popular, seems to boil down to that nasty nine-letter word, “socialism.”

Case in point, the bizarre meltdown experienced by conservative commentator Meghan McCain on the talk show “The View,” earlier this week.

McCain is no fan of socialism because . . . socialism is bad. Her proof is the country of Venezuela, which is experiencing a calamitous economic and social breakdown and has become a useful poster child for socialism-bashing conservatives. Never mind that many countries around the world have adopted the allegedly “socialist domestic policies” that Ocasio-Cortez is extolling — and have a citizenry that is happier, healthier, and more economically comfortable than in the United States. Socialism is bad. Period.

McCain cited two examples of the evils of big government socialism in America — the Post Office and the Veterans Administration. She could hardly found a stranger duo.

These are two of the most successful and well-run government institutions in America. When it comes to the former, I defer to Post Office evangelist Paul Waldman, a writer for The Washington Post and The American Prospect. The Post Office, he writes, “will come to your house, take a letter that you’ve written, move that letter by truck or plane or boat thousands of miles as far as it needs to go, and deliver it to the person you’ve sent it to, all in just a few days.”

It delivers 149 billion pieces of mail a year, which is half the mail in the world. And how much does this extraordinary service that we all take for granted cost? Forty-nine cents.

Advertisement

If you wanted to build a mail service from scratch and keep prices as low as they are, it would be impossible — and certainly unprofitable. Only the government can do something like this.

What about the VA? In recent years, the agency has been buffeted by scandals, but in reality, it is one of the best-run health care systems in the country. According to a 2016 Rand Corporation study, the quality of care at the VA is “equal to or better than care delivered in the private sector.”

The VA is ahead of the curve when it comes to use of electronic medical records, evidence-based medicine, and top-notch behavioral health programs.

Indeed, one of the strangest elements of the socialism debate revolves around health care. Medicare, the health insurance program for the elderly, is one of the most popular government programs in the country (the only one more admired is another big government socialist initiative, Social Security). Beyond its popularity, Medicare is also more efficient than private health insurance.

How many Americans have warm and fuzzy feelings about their health insurance company? How about your cable company, your mobile provider, your airline, or your bank? How many Americans think these are well-run organizations, responsive to customer needs and highly efficient? One might even argue that government-run institutions, not burdened by the pursuit for profit, are better position to provide the most essential public services.

Advertisement

But for McCain, the issue with socialism is less about the provision of government services and more about the possibility that a larger role for government will mean higher taxes. Considering that McCain’s family has a fortune of more than $200 million and just saw their taxes cut — including the estate tax, which will likely impact Meghan McCain — I understand her concerns.

And let’s face it, for many Americans, just hearing the word socialism is like waving a red flag in front of a bull. But when you get past the loaded political rhetoric and look at the so-called socialist ideas being pushed by Ocasio-Cortez and other left-leaning Democrats, what you have are policies that are consistent with existing government programs that Americans actually like. If implemented, these policies might even bring enormous benefits to millions of Americans.

You don’t have to be a card-carrying socialist to believe that access to health care, affordable housing, a quality education, sick leave, and family leave are net positives and that the government can often provide those services better than the private sector. You just need to believe in facts.

WASHINGTON — The Trump administration is hitting back against advocates of “Medicare for all” even as the proposal gains momentum among left-leaning Democrats in this election year.

Alex M. Azar II, the secretary of health and human services, said on Thursday that the administration had a vision for “reforming the American health care system” that would shrink, not expand, the federal role.

In a speech at the conservative Heritage Foundation, Mr. Azar said that Medicare could barely afford to keep its current commitments. “Medicare is running out of other people’s money, and those other people happen to be our children,” he said.

Seema Verma, the administrator of the Centers for Medicare and Medicaid Services, was even more pointed in her criticism.

Medicare is meant for “a very specific population,” older Americans and people with disabilities, Ms. Verma said on Wednesday in a speech at the Commonwealth Club in San Francisco. Offering it to every American would not only strain the finances of Medicare, but also “run the risk of depriving seniors of the coverage” they have, she said.

“Ideas like Medicare for all would only serve to hurt and divert focus from seniors,” Ms. Verma said, predicting that, “in essence, Medicare for all would become Medicare for none.”

Senator Bernie Sanders, independent of Vermont and a leading champion of Medicare for all, dismissed the criticism.

“Medicare has worked extremely well for our nation’s seniors and will work equally well for all Americans,” Mr. Sanders said. “It is extremely concerning that the person charged with administering Medicare would rather throw 32 million Americans off the health insurance they have than join every major nation on earth and guarantee health care as a fundamental right.”

The Congressional Budget Office estimated that a bill to repeal much of the Affordable Care Act, supported last year by President Trump and other Republicans, would have increased the number of people who are uninsured by 32 million.

Mr. Sanders is the chief sponsor of a bill, the Medicare for All Act, that starts by declaring, “Every individual who is a resident of the United States is entitled to benefits for health care services.” The bill would greatly reduce consumers’ out-of-pocket costs. The secretary of health and human services would establish a “national health budget,” set payment rates for health care providers, negotiate prices to be paid for prescription drugs and establish lists of covered drugs.

Fifteen Democratic senators have signed on as co-sponsors of Mr. Sanders’s bill. They include potential candidates for president in 2020 like Senators Cory Booker of New Jersey, Kirsten Gillibrand of New York, Kamala Harris of California and Elizabeth Warren of Massachusetts.

Democrats are already emphasizing the matter in midterm election campaigns.

“Health care is going to be the biggest issue in 2018,” said Senator Chuck Schumer of New York, the Democratic leader. “It is far more important to the vast majority of Americans than any other issue.”

In the House, 70 Democrats announced last week that they had formed a Medicare for All Congressional Caucus to build the case for such legislation. A bill to achieve that goal has been endorsed by 120 House Democrats, or about 62 percent of the party’s members in that chamber.

Representative Pramila Jayapal, Democrat of Washington and a leader of the Medicare for All Caucus, said Trump administration officials seemed “blind to the fact that a majority of Americans support expanding, not weakening, health care.”

A single-payer health care system would be much simpler and could save hundreds of billions of dollars a year, Ms. Jayapal said.

A study by a team of researchers at the Urban Institute in 2016, when Mr. Sanders was running for president, estimated that an earlier version of his plan could increase national health spending by a total of $6.6 trillion over 10 years. The proposal would shift spending from the private sector and states to the federal government, so, it said, federal spending could increase by $32 trillion over 10 years.

Mr. Sanders takes issue with those estimates. The cost would depend, in part, on how much the government paid for care provided to new beneficiaries. The Urban Institute team assumed that payment rates would be like those currently used in Medicare.

The Trump administration mobilized a major effort last year to persuade Congress to repeal the Affordable Care Act. Just days before a climactic Senate vote in late July, Energy Secretary Rick Perry circulated a newspaper column urging Congress to “repeal this crushing law,” and his department posted a message on Twitter drawing attention to his column.

The Government Accountability Office, a nonpartisan investigative arm of Congress, ruled on Thursday that the Twitter post violated federal law because the Energy Department was not authorized to spend money for that purpose.

Mr. Perry could not show any “reasonable and logical relationship between tweeting about health care and the purposes” for which Congress provided money to his department, said Thomas H. Armstrong, the general counsel of the Government Accountability Office.

Do Physicians Trust Physicians to Make Medical Decisions?

by Milton Packer - MedPage - July 11, 2018

Decades ago, physicians were among the most trusted members of their communities. Clinicians were viewed along with the clergy as venerable sources of knowledge, life experience and comfort. Much like religious vocations, careers in medicine were regarded as a calling. Physicians routinely cared for the poor without asking for remuneration, subsiding their endeavors with fees collected from those who could afford to pay. We spent countless hours relentlessly pursuing a diagnosis, partnering with patients to wage a war on death, and communing with families. We were routinely invited to our patients' weddings and funerals.

Physicians were not excessively paid, but they were showered with respect and received preferential treatment in countless ways. (Remember MD license plates?) Physicians were commonly excused for minor traffic violations, simply because the police could imagine that they were in a hurry to see a patient. Most local jurisdictions granted physicians an exemption from jury duty, believing that they already provided an irreplaceable service to their communities. If you wanted reservations at short notice in a popular restaurant, you told them you were a doctor. Even physicians honored other physicians. Doctors who required medical care were given "professional courtesy." In the 1980s, I was a patient at the Mayo Clinic, and received incredible medical care for free; no one ever asked for insurance information, and I never received a bill. In truth, the tokens of respect were often trivial and elitist, and in most cases, no reasonable person should miss them. But their emblematic significance was unmistakable.

As Paul Starr wrote in his book The Social Transformation of American Medicine,physicians were accorded a respect usually given to astronauts and coaches of championship football teams. Society also granted physicians a virtual monopoly in all aspects of medical decision-making. Extraordinarily, 40-50 years ago, more than 75% of Americans had great confidence in medical leaders, according to Dhruv Khullar, MD, MPP, in the New York Times last January. Despite exceptionally long hours, physician burnout was virtually nonexistent.

In 2018, the days of universal respect for physicians are gone. Many patients now view practitioners as hurried and financially motivated, lacking empathy. No social courtesies are granted to physicians; on the contrary, physicians are generally viewed as being undeserving of elite perquisites. Laymen are suspicious of physician motivations. "Am I getting the treatment that is best for me or for my physician's pocketbook?" patients wonder. The decision-making authority of physicians has evaporated. Payers now tell physicians what they can prescribe, and healthcare systems remind physicians about the number of procedures they must perform to warrant their compensation.

In a Gallup poll taken last month, Americans were asked about their respect for many of society's institutions and organizations. Only 36% said that they had a great deal of trust in the medical system. The good news: The "medical system" fared better than public schools (29%), big business (25%), and the criminal justice system (22%). The bad news: we fared much worse than the military (74%) and the police (54%) -- worse even than the Presidency (37%).

The lack of trust in the medical system is a particular American phenomenon. The U.S. is tied for 24th place among 29 surveyed countries in a ranking of the proportion of adults who think that doctors can be trusted. Only 58% of U.S. adults trust physicians, as compared with 83% in Switzerland, 79% in Denmark, 78% in the Netherlands, and 76% in Britain. According to Khullar, just 25% of Americans feel confident about the health system -- a statistic even more dismal than the results of the Gallup poll.

Some physicians may believe that the lack of public trust is related to a lack of public understanding of the demands on the profession. Non-physicians cannot understand the magnitude of information, the rigorous requirements for technical expertise or the complexities of healthcare delivery. Only physicians can understand what it is like to be a physician.

Well, physicians certainly know what it feels like to be a physician AND a patient. So we should ask: When physicians need medical care, do physicians trust other doctors or the medical system to take care of them?

I cannot find any formal surveys on this question, but I am fairly confident that uncertainties about competence and motivations may be especially high -- amongst physicians!

Every week, I am asked by physicians who are wondering (and worrying) about the wisdom of medical advice or treatment that they or a family member has received. Why did they not take an adequate history? Why did they order tests that do not make any sense? Why did they recommend an elective procedure that had nothing to do with my chief complaint? When they found out I didn't need surgery, why did they stop caring for me? Why do they never respond to my phone calls or the questions I send by email? Do they really have the wisdom, experience and expertise to provide the best possible care?

It is true that many physicians no longer have the time or staff to communicate effectively -- even with their physician patients. But based on personal experience, they certainly have the staff to make countless telephone calls to chase $10-$25 copays.

Here is the good news: Physicians can rebuild trust. They can prioritize patient communication over revenues. They can take steps to make sure that patients are able to navigate the complex steps of healthcare.

But to do so, physicians would need to really want to. They would need to refocus their attention on patients rather than themselves.

Many readers who are physicians will certainly be inclined to dismiss my musings as old-fashioned and outdated, with little relevance to modern medicine. Most troubling, some may no longer even care if patients trust them.

Indeed, many physicians fully acquiesce in the decline in medicine as a trusted institution. For some, the practice of medicine is now a job, not a calling (and for some, not even a career). Many try to fill the emptiness in their souls with the knowledge that they are well-paid or that they perform more procedures than their colleagues. The achievement of numerical targets has replaced trust and respect as a source of personal gratification. Yet, soaring rates of physician burnout attest to the fact that this substitution is likely to be misguided and futile.

My father could not tolerate playing Monopoly. His reason: There is no honor, dignity, or fulfillment in playing or winning. Within the game's value system, a player succeeds without garnering another's trust, and there is no mechanism by which a player's choices can invoke respect. Under all circumstances, when the game ends, the person with the most money still loses.

It’s 4 A.M. The Baby’s Coming. But the Hospital Is 100 Miles Away.

by Jack Healey - NYT - July 17, 2018

KENNETT, Mo. — A few hours after the only hospital in town shut its doors forever, Kela Abernathy bolted awake at 4:30 a.m., screaming in pain.

Oh God, she remembered thinking, it’s the twins.

They were not due for another two months. But the contractions seizing Ms. Abernathy’s lower back early that June morning told her that her son and daughter were coming. Now.

Ms. Abernathy, 21, staggered out of bed and yelled for her mother, Lynn, who had been lying awake on the living-room couch. They grabbed a few bags, scooped up Ms. Abernathy’s 2-year-old son and were soon hurtling across this poor patch of southeast Missouri in their Pontiac Bonneville, racing for help. The old hospital used to be around the corner. Now, her new doctor and hospital were nearly 100 miles away.

Medical help is growing dangerously distant for women in rural America. At least 85 rural hospitals — about 5 percent of the country’s total — have closed since 2010, and obstetric care has faced even starker cutbacks as rural hospitals calculate the hard math of survival, weighing the cost of providing 24/7 delivery services against dwindling birthrates, doctor and nursing shortages and falling revenues.

Today, researchers estimate that fewer than half of the country’s rural counties still have a hospital that offers obstetric care, an absence that adds to the obstacles rural women face in getting health care. Specialists are increasingly clustered in bigger cities. Clinics that provide abortions, long-term birth control and other reproductive services have been forced to close in many smaller towns.

“It’s scary,” said Katie Penn, who said she was rejected by eight doctors before finding an obstetrician in Jonesboro, Ark., about an hour from Kennett. “You never know what can happen.”

When obstetric services leave town, a cascade of risks follows, according to experts at the University of Minnesota Rural Health Research Center who have studied the consequences. Women go to fewer doctor’s appointments and more babies are born premature, compared with similar places that do not lose access to care. And when women go into labor, they are more likely to end up at emergency rooms with no obstetric care or to deliver outside a hospital altogether.

Families struggle to afford the gas, child care and time off work to drive hundreds of miles for an ultrasound, shots or hospital tests. Women say they have ended up on waiting lists at overwhelmed clinics, or been turned away because they said doctors did not want to take them as patients late into their pregnancies.

Women like Ms. Abernathy and Ms. Penn are particularly isolated because they live in the Missouri Bootheel in the southeast corner of the state, named for the way the area juts out of the state’s otherwise orderly shape.

The region was already coping with some of the state’s highest rates of maternal and infant mortality, and then in April came the news that Dunklin County’s only hospital, the Twin Rivers Regional Medical Center, would be closing. More than 179 rural counties have lost hospital obstetric care since 2004. Dunklin was now one of them.

‘Hospital Closed. Call 911 for Emergencies’

The white, 116-bed hospital had been a busy lifeline for this 31,000-person county’s most vulnerable people. The emergency room received about 22,000 visits a year, and unlike many struggling hospitals, the maternity ward was busy. About 400 babies were born at Twin Rivers every year, often to mothers who had themselves been born in the same rooms.

About 95 percent of the hospital’s patients were on Medicare, Medicaid or had no insurance, said Dr. Steve Pu, a former member of the hospital’s advisory board. Rural hospitals like Kennett’s are being financially battered by several factors: Cutsto public health-insurance programs, struggles with debt and sharply worsening finances in states that did not expand Medicaid.

In April, Twin Rivers announced it would be shutting down as part of a corporate consolidation by its owner, Community Health Systems, a publicly traded, for-profit hospital company. In a statement announcing the closing, the hospital’s local chief executive, Christian H. Jones, called it the “most sustainable plan for the future.”

Patients say they were told to seek care at another Community Health Systems hospital in Poplar Bluff, about 50 miles away down narrow two-lane roads. The hospital in Kennett had about 300 employees, the largest employer in a county with a 5.5 percent unemployment rate.

Then last month, with little warning, a sign went up at Twin Rivers: HOSPITAL CLOSED. CALL 911 FOR EMERGENCIES. Its last day of operations was June 11, more than two weeks earlier than the date executives initially told people in Kennett.

The only obstetrician in Kennett had operated his practice out of the hospital, and he began discharging patients and winding down services in the weeks before Twin Rivers closed. Women said his waiting room became a scene of sadness and confusion as they worried about where they would go next and how they would afford gas for weekly visits at distant hospitals when they barely had enough money to pay electric bills and rent.

The only pediatrician in Kennett, Andy Beach, hung a banner outside his clinic that mirrored the town’s defiant spirit, “We are not leaving the area!”

An ambulance service has been shuttling patients to other hospitals in the region, and a medical helicopter is on call for the worst emergencies. Doctors around Kennett and a hospital in Jonesboro are working to open urgent-care clinics, and officials have put a tax increase onto August ballots to raise money to build a hospital. Someday.

State officials and doctors are also trying to work out a plan and find $1.5 million to reopen the obstetric unit at the Pemiscot County hospital in Hayti, the closest hospital to Kennett.

In the meantime, the absence of local care is being felt already.

Mary Louisa, who was 26 weeks pregnant, recently started experiencing contractions that are a hallmark of preterm labor but had not had a full prenatal checkup in a month.

Susanna Hernandez’s first pregnancy ended in miscarriage. Now she was worried about her second and had not seen a doctor since the hospital in Kennett closed. Every few minutes, she touches her abdomen to feel for a kick, a movement, any sign that the girl inside is still healthy and growing. Ms. Hernandez, who emigrated from Mexico a year ago, speaks almost no English and spends her days trying to relax and pray.

“Our community is just in panic,” Deloris Johnson, who sits on the county’s ambulance board, said in an interview in June. “They don’t know what to do.”

Then, this month came the news that she and many in Kennett had been dreading. Two infant boys, each about a month old, died on opposite ends of the county, one on July 4 and the other the following morning.

In both instances, officials said that family members discovered the children unconscious and rushed them to local ambulance stations. One was driven 20 miles to a hospital in Paragould, Ark., and the other was taken to a hospital in Piggott, Ark., where they were each pronounced dead, investigators said. Investigators would not release the children’s names or any additional details. They said autopsy reports had not been completed and said they did not yet know how the children had died, or whether any intervention could have saved them.

Their deaths sent a shudder through Kennett.

“This is just the beginning,” Ms. Johnson said. “To think we don’t even have a damn hospital for these people to go to.”

Rushed Into Surgery After a Four-Hour Trek

As Ms. Abernathy and her mother raced down dark country roads at 90 miles an hour, all they could think about were the twins. Would she have to deliver them on the side of the road, before she got to a hospital? Would the babies be O.K.?

They pulled into the town of Hayti 17 miles east and rushed into the Pemiscot County hospital. It was an act of desperation. The hospital’s obstetrics unit had closed four years ago, and the emergency-room staff looked shocked to see her. The labor and delivery rooms now sat unused.

The staff told Ms. Abernathy she needed to reach the hospital now caring for her after Kennett’s closed: St. Francis Medical Center in Cape Girardeau, Mo., nearly 80 miles away. It had a neonatal intensive care unit, neonatal operating rooms and a full battery of obstetric doctors and nurses. But there was no ambulance ready to take her.

Ms. Abernathy said she waited for about 25 minutes as an ambulance rushed over from Kennett to pick her up. An obstetric nurse rode along, rubbing her back and helping her breathe as the contractions continued.

When they passed through the small town of Sikeston, Ms. Abernathy said the ambulance driver asked whether they needed to stop at the hospital there. Keep going, Ms. Abernathy and the nurse told him. Nearly four hours after she woke up screaming in bed, they arrived at a hospital with an obstetrics ward.

Her doctor rushed to get her into surgery. Forty-five minutes later, the twins were born by cesarean section, first Kaleb at 3 pounds 6 ounces and then Kylynn at 2 pounds 12 ounces.

They were healthy, but because they arrived early, they would need weeks of close care at the hospital: nurses who could check their breathing and vital signs and also show Ms. Abernathy how the babies needed to be touched and held.

This meant that Ms. Abernathy had to make regular 200-mile round trips to the hospital to see the twins and then back to Kennett to be with her 2-year-old. One day, her C-section incision was so inflamed by the drive that she could barely stand. Another afternoon, she and her mother had to pull over when a summer storm swamped the highway.

Ms. Abernathy said she was eager to bring the twins home and to get back to her $8.50-an-hour job as a home health aide. There is rent to make, baby clothes to purchase, $80 of gas to buy for the coming week.

“My mom raised me to be independent,” she said. “I’ve always worked.”

One morning, she lay underneath a blanket on her couch, exhausted and upset about the inconveniences and indignities of the past month and the stress of not seeing a doctor for weeks when she knew she was a high-risk patient.

“I was an emotional wreck. I can’t tell you how many times I cried,” Ms. Abernathy said, as her mother hovered beside her. “We can’t keep a hospital. What is our community coming to?”

The preceding article is a dramatic example of the inevitable result of applying market principles to the delivery of health care.

Caveat Emptor!

-SPC

The real driver of health care spending

An inefficiency gap is boosting costs — and profits

Edward M. Murphy - Commonwealth Magazine - July 9, 2018

THE HEALTH CARE DEBATES that occurred in Washington over the past year were largely irrelevant to what’s happening in the health care marketplace. Republicans couldn’t repeal the Affordable Care Act but they made some changes that weakened it. Those changes will increase insurance premiums in the individual market but they do nothing to address the most significant trends that are evolving across the system. To understand the important trends, one must look elsewhere.

In March, three researchers from the Harvard T. H. Chan School of Public Health published a study in JAMA analyzing the well-known reality that the United States spends dramatically more on health care than other wealthy countries. They compared the US, where health care consumes 17.8 per cent of gross domestic product, to 10 comparable nations where the mean expenditure is 11.5 percent. Despite spending much less, the other countries provide health insurance to their entire populations and have outcomes equal to or better than ours. The researchers found that this inefficiency gap is primarily driven by two characteristics of the US system: the high cost of pharmaceuticals and inordinate administrative expenses.

For example, annual per capita pharmaceutical expenditure in the US is $1,443 as compared to an average of $749 in the 10 other countries. Our administrative costs consume 8 percent of total spending as compared to a range of 1 to 3 percent elsewhere. No one else is close on either of these measures.

The high administrative spending derives in large part from the fact that 55 percent of the people in the US are covered by private health insurers who embed their own billing requirements, expenses, and profit into the system. The next highest country in this regard is Germany, where 10.8 percent of the population is covered by private insurers. In many countries, there are no such middlemen.

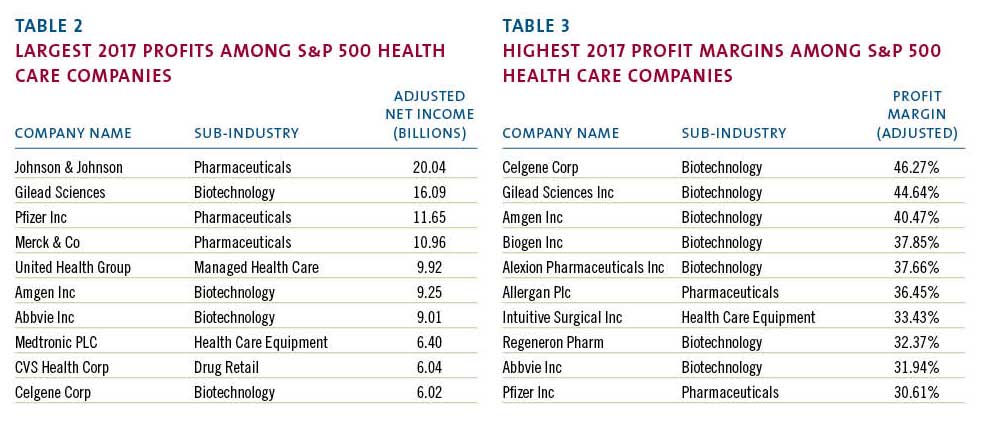

Coincidentally, when the JAMA study was published, the large publicly traded health care companies that dominate the US market had just finished disclosing their 2017 financial results. Examining those results provides additional insight into the economic forces that make our system so expensive and inefficient. The scale of the money involved is sometimes hard to grasp. The largest health care corporations, those included in the S&P 500, had almost $2 trillion in revenue last year. (Table 1)

Most of these enormous companies are engaged in one of two businesses: they’re either selling drugs or they’re selling health insurance. The excess costs reported by the Harvard researchers serve mainly to support the revenue of the companies in those fields.

The 2017 reporting of corporate profits was complicated by the passage of the new tax bill. But most companies also reported “adjusted net income,” which shows their normalized profits after accounting for the one-time impact of the tax law. The chart below (Table 2) uses the adjusted numbers to show the largest annual profits among S&P health care companies.

Health insurers such as United Health and retailers such as CVS have enormous revenue and impressive profits but, when profit is measured as a percentage of revenue, they can’t compete with biotech and pharma. The highest relative profitability, using the same reported adjusted results, is in the chart below. (Table 3)

These profit margins show that there are many situations where between a third and a half of every dollar spent on a prescription drug falls to the bottom line of the of the company that made it. This profit derives in large part from the enormous difference in drug prices in the US versus other countries where such prices are more effectively controlled.

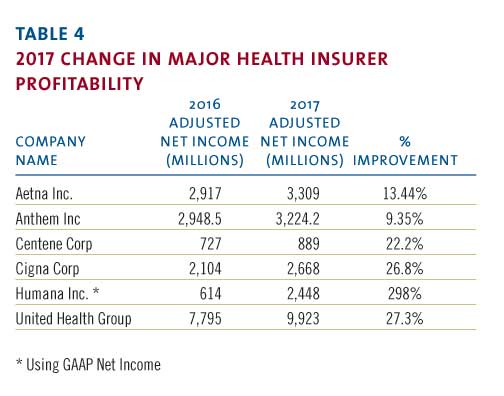

The high administrative cost of the US system stems from the large portion of the market dominated by insurance companies looking to maximize their profits. Notwithstanding many news stories about turmoil in the insurance markets, 2017 was a banner year for the largest health insurers. The big players all had significant increases in annual profitability in 2017.

Note that Humana did not report “adjusted” numbers even though its profit was swollen by unusual events. A major distortion was a huge break-up fee the company received from a failed merger. That accounted for approximately $630 million in after-tax profit. Even discounting that, it was a very good year.

The revenue and profitability of these corporations support the proposition that high pharmaceutical prices and insurance-related administrative costs account for much of the extraordinary expense of our system. US health policy, or the absence thereof, has enabled these businesses annually to drive costs up for the benefit of their bottom line. That effect will continue. Not surprisingly, the big health care companies are developing new strategies to enhance their businesses and drive their profits going forward.

The term now heard often among health care giants is “vertical integration,” which means combining upstream suppliers with downstream buyers to control the flow of business. If this strategy persists, health care delivery will evolve significantly although it is unlikely to become less expensive. The most prominent current example of vertical integration is the planned $68 billion acquisition of Aetna by CVS.

How would these companies work together? A Wall Street analyst recently described the vision as a way to “identify high risk patients and preemptively get them into a Minute Clinic.” Thus, your health insurer could send you to a local store for diagnosis, treatment, drugs, and anything else you might need from the shelves. This will keep even more of the health care dollar under their control.

Similarly, Cigna is in the process of acquiring Express Scripts, a huge pharmacy benefits manager, for $54 billion, another attempt to bring more services under one roof. The combined company would have annual revenue of $142 billion and, presumably, enough leverage with drug companies to improve profits although not necessarily to lower costs to patients. United Health, a leader of vertical integration, previously bought a pharmacy benefit manager but co-pays and deductibles for its patients have continued to climb. United has aggressively acquired physician practices in recent years and is now in the process of buying DaVita Medical Group, which operates nearly 300 clinics and outpatient surgical centers.

More striking are reports of a potential but unsigned merger of Walmart and Humana, a combined company that would have revenue of $550 billion. Walmart is a large operator of retail pharmacies inside its stores and the logic is similar to the Aetna-CVS deal. Humana, a huge insurer, is separately in the process of acquiring a large home health business from Kindred so this could represent yet another level of vertical integration.

If this course continues, the health care system will evolve quickly, giving fewer and larger companies even more market leverage. Integration of this kind benefits the large corporations that initiate it but there is no evidence it will lead to lower costs, improved access, or enhanced quality. These changes are driven by highly focused corporate financial interests and are occurring without reference to public policy. That’s because there is no coherent public policy to guide these changes.

On May 11, President Trump made a long-awaited speech to reveal what he described as “the most sweeping action in history to lower the price of prescription drugs for the American people.” His typically firebrand language struck at “drug makers, insurance companies, distributors, pharmacy benefit managers, and many others” who contributed to “this incredible abuse.” His attack seemed to target the large public companies that have benefited from the abuse. Unsurprisingly, his speech did not include specifics. His staff then released tepid policy details, which immediately generated a significant upward spike in the biotech stock index as well as the stock prices of other large health care companies. For all the presidential bombast, investors saw Trump’s policy for what it is: indifference to the current path and no threat to high prices.

It is not in the interest of huge profit-making corporations to restrain the overall cost of the US health care system. In fact, their interest is served by driving health care expenditures higher. When combined with the spending analysis provided by researchers, the financial data disclosed by public corporations point to a path that the country must follow to make our system more coherent and less costly. Any progress will require driving down pharmaceutical pricing and reducing administrative costs imposed by middlemen. We are not doing that yet but, ultimately, we must.

Hidden From View: The Astonishingly High Administrative Costs of U.S. Health Care

The complexity of the system comes with costs that aren’t obvious but that we all pay.

by Austin Frakt - NYT - July 16, 2018

It takes only a glance at a hospital bill or at the myriad choices you may have for health care coverage to get a sense of the bewildering complexity of health care financing in the United States. That complexity doesn’t just exact a cognitive cost. It also comes with administrative costs that are largely hidden from view but that we all pay.

Because they’re not directly related to patient care, we rarely think about administrative costs. They’re high.

A widely cited study published in The New England Journal of Medicine used data from 1999 to estimate that about 30 percent of American health care expenditures were the result of administration, about twice what it is in Canada. If the figures hold today, they mean that out of the average of about $19,000 that U.S. workers and their employers pay for family coverage each year, $5,700 goes toward administrative costs.

Such costs aren’t all bad. Some are tied up in things we may want, such as creating a quality improvement program. Others are for things we may dislike — for example, figuring out which of our claims to accept or reject or sending us bills. Others are just necessary, like processing payments; hiring and managing doctors and other employees; or maintaining information systems.

That New England Journal of Medicine study is still the only one on administrative costs that encompasses the entire health system. Many other more recent studies examine important portions of it, however. The story remains the same: Like the overall cost of the U.S. health system, its administrative cost alone is No. 1 in the world.

Using data from 2010 and 2011, one study, published in Health Affairs, compared hospital administrative costs in the United States with those in seven other places: Canada, England, Scotland, Wales, France, Germany and the Netherlands.

At just over 25 percent of total spending on hospital care (or 1.4 percent of total United States economic output), American hospital administrative costs exceed those of all the other places. The Netherlands was second in hospital administrative costs: almost 20 percent of hospital spending and 0.8 percent of that country’s G.D.P.

At the low end were Canada and Scotland, which both spend about 12 percent of hospital expenditures on administration, or about half a percent of G.D.P.

Hospitals are not the only source of high administrative spending in the United States. Physician practices also devote a large proportion of revenue to administration. By one estimate, for every 10 physicians providing care, almost seven additional people are engaged in billing-related activities.

It is no surprise then that a majority of American doctors say that generating bills and collecting payments is a major problem. Canadian practices spend only 27 percent of what U.S. ones do on dealing with payers like Medicare or private insurers.

Another study in Health Affairs surveyed physicians and physician practice administrators about billing tasks. It found that doctors spend about three hours per week dealing with billing-related matters. For each doctor, a further 19 hours per week are spent by medical support workers. And 36 hours per week of administrators’ time is consumed in this way. Added together, this time costs an additional $68,000 per year per physician (in 2006). Because these are administrative costs, that’s above and beyond the cost associated with direct provision of medical care.

In JAMA, scholars from Harvard and Duke examined the billing-related costs in an academic medical center. Their study essentially followed bills through the system to see how much time different types of medical workers spent in generating and processing them.

At the low end, such activities accounted for only 3 percent of revenue for surgical procedures, perhaps because surgery is itself so expensive. At the high end, 25 percent of emergency department visit revenue went toward billing costs. Primary care visits were in the middle, with billing functions accounting for 15 percent of revenue, or about $100,000 per year per primary care provider.

“The extraordinary costs we see are not because of administrative slack or because health care leaders don’t try to economize,” said Kevin Schulman, a co-author of the study and a professor of medicine at Duke. “The high administrative costs are functions of the system’s complexity.”

Costs related to billing appear to be growing. A literature review by Elsa Pearson, a policy analyst with the Boston University School of Public Health, found that in 2009 they accounted for about 14 percent of total health expenditures. By 2012, the figure was closer to 17 percent.

One obvious source of complexity of the American health system is its multiplicity of payers. A typical hospital has to contend not just with several public health programs, like Medicare and Medicaid, but also with many private insurers, each with its own set of procedures and forms (whether electronic or paper) for billing and collecting payment. By one estimate, 80 percent of the billing-related costs in the United States are because of contending with this added complexity.

“One can have choice without costly complexity,” said Barak Richman, a co-author of the JAMA study and a professor of law at Duke. “Switzerland and Germany, for example, have lower administrative costs than the U.S. but exhibit a robust choice of health insurers.”

An additional source of costs for health care providers is chasing patients for their portion of bills, the part not covered by insurance. With deductibles and co-payments on the rise, more patients are facing cost sharing that they may not be able to pay, possibly leading to rising costs for providers, or the collection agencies they work with, in trying to get them to do so.

Using data from Athenahealth, the Harvard health economist Michael Chernew computed the proportion of doctors’ bills that were paid by patients. For relatively small bills, those under $75, over 90 percent were paid within a year. For larger ones, over $200, that rate fell to 67 percent.

“It’s a mistake to think that billing issues only reflect complex interactions between providers and insurers,” Mr. Chernew said. “As patients are required to pay more money out of pocket, providers devote more resources to collecting it.”

A distinguishing feature of the American health system is that it offers a lot of choice, including among health plans. Because insurers and public programs have not coordinated on a set of standards for pricing, billing and collection — whatever the benefits of choice — one of the consequences is high administrative burden. And that’s another reason for high American health care prices.

HHS Plans to Delete 20 Years of Critical Medical Guidelines Next Week

by John Campbell - The Daily Beast - July 12, 2018

Experts say the database of carefully curated medical guidelines is one of a kind, used constantly by medical professionals, and on July 16 will ‘go dark’ due to budget cuts.

The Trump Administration is planning to eliminate a vast trove of medical guidelines that for nearly 20 years has been a critical resource for doctors, researchers and others in the medical community.

Maintained by the Agency for Healthcare Research and Quality [AHRQ], part of the Department of Health and Human Services, the database is known as the National Guideline Clearinghouse [NGC], and it’s scheduled to “go dark,” in the words of an official there, on July 16.

Medical guidelines like those compiled by AHRQ aren’t something laypeople spend much time thinking about, but experts like Valerie King, a professor in the Department of Family Medicine and Director of Research at the Center for Evidence-based Policy at Oregon Health & Science University, said the NGC is perhaps the most important repository of evidence-based research available.

“Guideline.gov was our go-to source, and there is nothing else like it in the world,” King said, referring to the URL at which the database is hosted, which the agency says receives about 200,000 visitors per month. “It is a singular resource,” King added.

Medical guidelines are best thought of as cheatsheets for the medical field, compiling the latest research in an easy-to use format. When doctors want to know when they should start insulin treatments, or how best to manage an HIV patient in unstable housing — even something as mundane as when to start an older patient on a vitamin D supplement — they look for the relevant guidelines. The documents are published by a myriad of professional and other organizations, and NGC has long been considered among the most comprehensive and reliable repositories in the world.

AHRQ said it’s looking for a partner that can carry on the work of NGC, but that effort hasn’t panned out yet.

“AHRQ agrees that guidelines play an important role in clinical decision making, but hard decisions had to be made about how to use the resources at our disposal,” said AHRQ spokesperson Alison Hunt in an email. The operating budget for the NGC last year was $1.2 million, Hunt said, and reductions in funding forced the agency’s hand.

Not even an archived version of the site will remain, according to an official at AHRQ. Areport from the Sunlight Foundation’s Web Integrity Project found the agency announced the site’s retirement, as well as that of a related but less trafficked “Quality Measures” site, this Spring. Some of the NGC’s pages are preserved in a third party archive, but no comprehensive backup of the site’s contents or search functions exists.

Part of what makes NGC unique is its breadth, King explained. Drawing on research from all over the country and the world, from professional organizations and research institutes, the site offers a free, and virtually comprehensive, body of guidelines in a centralized and easily searchable location. Rather than seeking out guidelines from dozens of individual publishers, King said, the NGC allows researchers to find the full range of resources in one stop.

The site plays another critical role, King said: that of gatekeeper. Because medical guidelines are produced by such a vast array of organizations, they vary widely in quality.

“In times past, there were an awful lot of, let me put air quotes around this — ‘guidelines’ — that weren’t of good methodologic quality,” King said. “They were typically just expert opinions, or what we jokingly refer to as BOGSAT guidelines: ‘bunch of guys sitting around a table’ guidelines.”

The NGC has a screening process designed to keep weakly supported research out. It also offers summaries of research and an interactive, searchable interface.

That gatekeeping role has sometimes made AHRQ a target. The agency was nearly eliminated shortly after its establishment, in the mid-90s, when it endorsed non-surgical interventions for back pain, a position that angered the North American Spine Society, a trade group representing spine surgeons. A subsequent campaign led to significant funding losses for AHRQ, and since then, the agency as a whole has been a perennial target for Republicans who have argued that its work is duplicated at other federal agencies.

The vetting role played by the NGC is a critical one, says Roy Poses, with the Patient-Centered Outcomes Research Institute.

“Many guidelines are actually written mainly for commercial purposes or public relations purposes,” said Poses, and can be subtly shaped to promote a given course of treatment. A guideline written for the treatment of depression, for example, may emphasize pharmaceuticals over talk therapy.

“The organizations writing the guidelines may be getting millions of dollars from big drug companies that want to promote a product. The people writing them may have similar conflicts of interest,” Poses said. NGC’s process provided a resource comparatively free of that kind of influence.

Underscoring how medical research like that maintained by the NGC can be politicized, AHRQ drew the ire of then-congressmember Tom Price in 2016 when it published a study critical of a drug manufactured by one of his campaign donors.According to ProPublica, one of Price’s aides emailed “at least half a dozen times” asking the agency to pull the critical research down. Price was the first director of HHS, AHRQ’s parent agency, under the Trump Administration, before resigningunder pressure last year over his spending on chartered flights.

The current director of AHRQ, Gopal Khanna — a Price appointee — is the first non-scientist to head the agency. His résumé includes mostly positions in information technology management, in state government in Minnesota and Illinois, and a brief stint in the George W. Bush White House. Shortly after he was hired in 2017, heannounced that data dissemination as one of his central priorities at the agency.

Mary Nix, Deputy Director of the Division of Practice Improvement at the Center for Evidence and Practice Improvement within AHRQ, cited budget cuts as the driving force behind NGC’s retirement. The site was most recently supported by a fee on some health insurance plans, which was instituted as part of the Affordable Care Act but is set to sunset in 2019. Nix estimates that the site would cost a “few hundred thousand” dollars per year to maintain even as a static archive.

Nix has been helping coordinate an effort to get some outside stakeholder to take over the site’s operations. She said she’s still hopeful, and even days before the site’s scheduled demise, AHRQ spokesperson Hunt told the Daily Beast that the search continued.

“Losing [the NGC] is really losing a valuable resource,” said Ana Maria Lopez, President of the American College of Physicians. She said the NGC is a primary source for her organization’s research, and noted that digital repositories like the NGC are only more critical today. “We’ll be thinking through what role we might be able to play here in helping to protect access to scientific information.”

Health Insurers Are Vacuuming Up Details About You — And It Could Raise Your Rates

by Marshall Allen - Maine Public - July 17, 2018

To an outsider, the fancy booths at a June health insurance industry gathering in San Diego, Calif., aren't very compelling: a handful of companies pitching "lifestyle" data and salespeople touting jargony phrases like "social determinants of health."

But dig deeper and the implications of what they're selling might give many patients pause: A future in which everything you do — the things you buy, the food you eat, the time you spend watching TV — may help determine how much you pay for health insurance.

With little public scrutiny, the health insurance industry has joined forces with data brokers to vacuum up personal details about hundreds of millions of Americans, including, odds are, many readers of this story.

The companies are tracking your race, education level, TV habits, marital status, net worth. They're collecting what you post on social media, whether you're behind on your bills, what you order online. Then they feed this information into complicated computer algorithms that spit out predictions about how much your health care could cost them.

Are you a woman who recently changed your name? You could be newly married and have a pricey pregnancy pending. Or maybe you're stressed and anxious from a recent divorce. That, too, the computer models predict, may run up your medical bills.

Are you a woman who has purchased plus-size clothing? You're considered at risk of depression. Mental health care can be expensive.

Low-income and a minority? That means, the data brokers say, you are more likely to live in a dilapidated and dangerous neighborhood, increasing your health risks.

"We sit on oceans of data," said Eric McCulley, director of strategic solutions for LexisNexis Risk Solutions, during a conversation at the data firm's booth. And he isn't apologetic about using it. "The fact is, our data is in the public domain," he said. "We didn't put it out there."

Insurers contend they use the information to spot health issues in their clients—and flag them so they get services they need. And companies like LexisNexis say the data shouldn't be used to set prices. But as a research scientist from one company told me: "I can't say it hasn't happened."

At a time when every week brings a new privacy scandal and worries abound about the misuse of personal information, patient advocates and privacy scholars say the insurance industry's data gathering runs counter to its touted, and federally required, allegiance to patients' medical privacy. The Health Insurance Portability and Accountability Act, or HIPAA, only protects medical information.

"We have a health privacy machine that's in crisis," said Frank Pasquale, a professor at the University of Maryland Carey School of Law who specializes in issues related to machine learning and algorithms. "We have a law that only covers one source of health information. They are rapidly developing another source."

Patient advocates warn that using unverified, error-prone "lifestyle" data to make medical assumptions could lead insurers to improperly price plans – for instance raising rates based on false information – or discriminate against anyone tagged as high cost. And, they say, the use of the data raises thorny questions that should be debated publicly, such as: Should a person's rates be raised because algorithms say they are more likely to run up medical bills? Such questions would be moot in Europe, where a strict law took effect in May that bans trading in personal data.

This year, ProPublica and NPR are investigating the various tactics the health insurance industry uses to maximize its profits. Understanding these strategies is important because patients – through taxes, cash payments and insurance premiums—are the ones funding the entire health care system. Yet the industry's bewildering web of strategies and inside deals often have little do with patients' needs. As the series' first story showed, contrary to popular belief, lower bills aren't health insurers' top priority.

Inside the San Diego Convention Center, there were few qualms about the way insurance companies were mining Americans' lives for information — or what they planned do with the data.

Linking health costs to personal data