Column: Health insurance companies are useless. Get rid of them

by Michael Hiltzik - LA Times - August 5, 2019

The most perplexing aspect of our current debate over healthcare and

health coverage is the notion that Americans love their health insurance

companies. This bizarre idea surfaced most recently in the

hand-wringing over proposals to do away with private coverage advocated

by some of the candidates for the Democratic nomination for president.

Oddly, this position has been treated as a vote-loser. During the

first round of televised debates on July 30 and 31, only four of the 20

candidates raised their hands when asked if they would ban private

insurers as part of their proposals for universal coverage: Sens.

Elizabeth Warren of Massachusetts, Bernie Sanders of Vermont and Kamala

Harris of California, and New York Mayor Bill de Blasio. Harris later

backed away, releasing a “Medicare for all” proposal that would accommodate private insurers at least for the first 10 years.

Health insurers have been successful at two things: Making money and getting the American public to believe they’re essential.

Health insurance expert Wendell Potter

She should have stood her ground. The truth is that private health

insurers have contributed nothing of value to the American healthcare

system. Instead, they have raised costs and created an entitled class of

administrators and executives who are fighting for their livelihoods,

using customers’ premium dollars to do so. “Health insurers have been successful at two things: Making money and

getting the American public to believe they’re essential,” says Wendell

Potter. He should know, since he spent decades as a corporate

communications executive in the industry, including more than 10 years at Cigna. The insurers’ success in making themselves seem essential accounts

for the notion that Americans are so pleased with their private coverage

that they’ll punish any politician who dares to take it away. But the

American love affair with private insurance warrants close inspection. Let’s

start by examining what the insurers say are their positive

contributions to healthcare. They claim to promote “consumer choice,”

simplify “the health care experience for individuals and families,”

address “the burden of chronic disease” and harness “data and technology

to drive quality, efficiency, and consumer satisfaction.” (These claims

all come from the website of the industry’s lobbying organization, America’s Health Insurance Plans (AHIP). They’ve achieved none of these goals. The increasingly prevalent mode

of health coverage in the group and individual markets is the the

narrow network, which shrinks the roster of doctors and hospitals

available to enrollees without heavy surcharges. The hoops that

customers and providers often must jump through to get claims paid

impose costly complexity on the system, not simplicity. Programs to

manage chronic diseases remain rare, and the real threat to patients

with those conditions was lack of access to insurance (until the

Affordable Care Act made such exclusion illegal). Private insurers

don’t do nearly as well as Medicare in holding down costs, in part

because the more they pay hospitals and doctors, the more they can

charge in premiums and the more money flows to their bottom lines. They

haven’t shown notable skill in managing chronic diseases or bringing

pro-consumer innovations to the table.

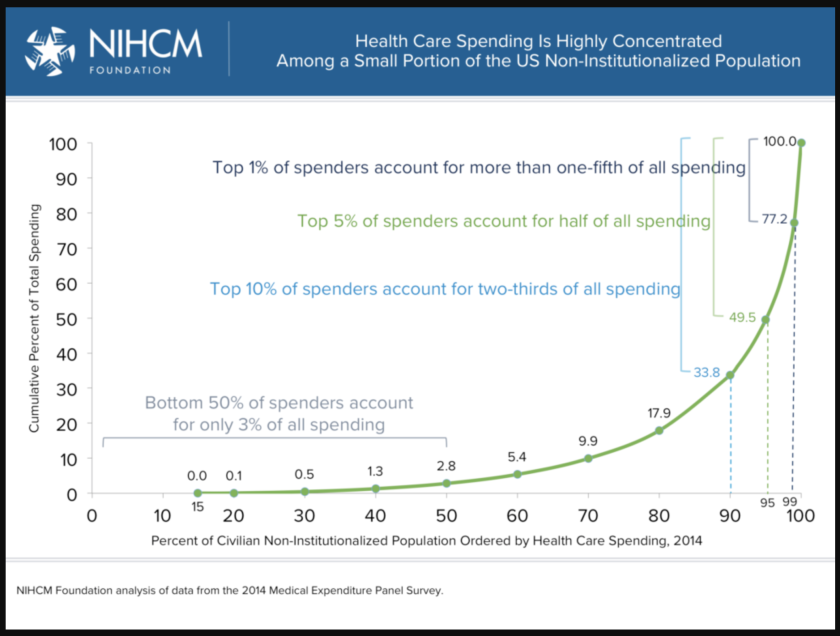

The vast majority of Americans have very little need for medical

care in any given year; that's why most people are satisfied with their

coverage. But what if they have a big claim? (NIHCM)

Insurers cite these goals when they try to get mergers approved by

government antitrust regulators. Anthem and Cigna, for example, asserted in 2016

that their merger would produce nearly $2 billion in “annual

synergies,” thanks to improved “operational” and “network efficiencies.” The pitch has a long history. The architects of a wave of health insurance mergers in the 2000s also proclaimed a new era of efficient technology and improved customer service,

but studies of prior mergers show that this nirvana seldom comes to

pass. The best example may be that of Aetna’s 1996 merger with U.S.

Healthcare in a deal it hoped would give it access to the booming HMO

market. According to a 2004 analysis

by UC Berkeley health economist James C. Robinson, the merger became a

“near-death” experience for Aetna. The deal was expected to bring about

“millions in enrollment and billions in revenue to pressure physicians

and hospitals” to accept lower reimbursement rates, he wrote. “The talk was all about complementarities, synergies, and economies

of scale... The reality quickly turned out to be one of incompatible

product designs, operating systems, sales forces, brand images, and

corporate cultures.” Aetna surged from 13.7 million customers in 1996 to

21 million in 1999, but profits collapsed from a margin of nearly 14%

in 1998 to a loss in 2001. Even when they don’t happen, insurance

merger deals cost customers billions of dollars. That’s what happened

when two proposed deals -- Aetna/Humana and Anthem/Cigna -- broke down

on a single day in 2017. The result was that Aetna owed Humana $1.8

billion and Anthem owed Cigna $1.85 billion in breakup fees -- money

taken out of the medical treatment economy and transferred from one set

of shareholders to another. In reality, Americans don’t like their

private health insurance so much as blindly tolerate it. That’s because

the vast majority of Americans don’t have a complex interaction with

the healthcare system in any given year, and most never will. As we’ve

reported before, 1% of patients account for more than one-fifth of all

medical spending and 10% account for two-thirds. Fifty percent

of patients

account for only 3% of all spending. Most families face at most a series of minor ailments that can be

routinely managed -- childhood immunizations, a broken arm here or

there, a bout of the flu. The question is what happens when someone does

have a complex issue and a complex claim — they’re hit by a truck or

get a cancer diagnosis, for instance? “We gamble every year that

we’re going to stay healthy and injury-free,” Potter says. When we lose

the gamble, that’s when all the inadequacies of the private insurance

system come to the fore. Confronted with the prospect of expensive

claims, private insurers try to constrain customers’ choices -- limiting

recovery days spent in the hospital, limiting doctors’ latitude to try

different therapies, demanding to be consulted before approving surgical

interventions. Indeed, the history of American healthcare reform

is largely a chronicle of steps taken to protect the unserved groups

from commercial health insurance practices. When commercial health insurance became insinuated into the American

healthcare system following World War II via employer plans, it quickly

became clear who was left behind -- “those who were retired, out of

work, self-employed, or obliged to take a low-paying job without

fringes,” sociologist Paul Starr wrote in his magisterial 1982 book, “The Social Transformation of American Medicine.”The

process even left those groups worse off, Starr observed, because

insurance contributed to medical inflation while insulating only those

with health plans. “Government intervention was required just to address

the inequities.” Insurers wouldn’t cover the aged or retirees, so

Medicare was born in 1965. Insurers refused to cover kidney disease

patients needing dialysis, so Congress in 1973 carved out an exception

allowing those patients to enroll in Medicare at any age. (So much for

addressing the “burden of chronic disease.”) Individual buyers

were charged much more for coverage than those buying group plans

through their employers -- or barred from the marketplace entirely

because of their medical conditions -- the Affordable Care Act required

insurers to accept all applicants and, as compensation, required all

individuals to carry at least minimal coverage. The health insurance industry’s most telling contribution to the

debate over healthcare reform has been “to scare people about other

healthcare systems,” Potter told me. As a consequence, discussions about

whether or how to remove private companies from the healthcare system

are chiefly political, not practical. The Affordable Care Act

allowed private insurers to continue playing a role in delivering

coverage not because they were any good at it but because their wealth

and size made them formidable adversaries to reform if they chose to

fight it. They were sufficiently mollified to remain out of the fray,

but some of the big insurers then did their best to undermine the individual insurance exchanges once they were launched in 2015. Even as individual Americans fret over losing their private health

insurance, big employers have begun to see the light. Boeing, among

other big employers, is experimenting with bypassing health insurers

as intermediaries with providers by contracting directly with major

health systems in Southern California, Seattle and other regions where

it has major plants. It would not be surprising to see the joint venture

of Amazon, Berkshire Hathaway and JP Morgan Chase try a similar

approach in its quest to bring down costs. That’s an ironic

development, since the private insurers first entered the market

precisely by offering to play the role of intermediaries for big

employers. But instead of fulfilling the promise of efficiency and cost

control, they became rent-seeking profiteers themselves. There’s

no doubt that it will take years to wean the American healthcare system

off the private insurance model; Kamala Harris’s proposal may be merely a

recognition of the necessary time frame. It’s true that some countries

with universal healthcare systems preserve roles for private insurance,

including coverage for services the government chooses to leave out of

its own programs or providing preferential access to specialists, at a

price. But the private insurers’ central position in America’s

system is an anachronism dating back some 75 years. The sooner it’s

dispensed with, the better -- and healthier -- America will be. The next

time a debate moderator asks presidential candidates if they favor

doing away with private insurance, let’s see all the hands go up. https://www.latimes.com/business/story/2019-08-05/health-insurance-useless

Why Doctors Should Organize

Meeting the challenges of modern medicine will require more than seeing patients.

In the fall of 2018, the American College of Physicians published a position paper

on gun violence. “Firearm violence continues to be a public health

crisis in the United States,” its authors wrote, in the journal Annals of Internal Medicine.

The report argued that assault weapons should be banned and that

“physicians should counsel patients on the risk of having firearms in

the home.” When it was published, the National Rifle Association responded with a tweet: “Someone should tell self-important anti-gun doctors to stay in their lane.” The

N.R.A.’s tweet provoked an unprecedented response from the medical

profession. Using the hashtag #ThisIsMyLane, emergency-room physicians,

trauma surgeons, pediatricians, and pathologists, all of whom are

involved in the care of patients with gunshot wounds, posted images of

shooting victims and bloodstained hospital floors. Some shared selfies

in which they were splattered with blood. “Do you have any idea how many

bullets I pull out of corpses weekly? This isn’t just my lane. It’s my

fucking highway,” Judy Melinek, a forensic pathologist, tweeted. Melinek’s tweet went viral. Doctors appeared on television and wrote op-eds expressing their disgust with the N.R.A. As

a physician, I was thrilled by this display of solidarity and political

engagement. But I also wondered why such mobilizations aren’t more

common. In October, 1980, when I was a medical resident at San Francisco

General Hospital, a group of interns and residents went on strike,

protesting a disastrous shortage of nurses. (We also asked for on-site

childcare, and, less crucially, a lounge with a Ping-Pong table and

better food.) At the time, I was a resident in the Coronary Care Unit,

and so was involved in the care of critically ill patients; as a result,

I was allowed to cross the picket line. Still, my peers booed me. I

remember that the chief of the medical service stood at the hospital

entrance, demanding, through a bullhorn, that the doctors get back to

work. My colleagues were defiant, and the strike continued for a few

days, stopping only when the hospital agreed to alleviate the nursing

shortage. The strike was organized by the San Francisco Interns

and Residents Association—a union whose current iteration, this past

March, protested low pay and poor working conditions with a fifteen-minute walkoff

at the University of California, San Francisco’s Medical Center. There

have been some other efforts to form unions of doctors, such as the

California-based Union of American Physicians and Dentists. But they

haven’t caught on industry-wide—the U.A.P.D. has only four thousand

members—and, in my long career, the 1981 strike remains one of the few

times I’ve seen doctors come together around a common cause. In

truth, its stakes were small compared to the problems physicians must

confront today. Doctors now face a burnout epidemic: thirty-five per

cent of them show signs of high depersonalization, a type of emotional

withdrawal that makes personal connections with their patients

difficult. Administrative tasks have become so burdensome that,

according to one recent report, only thirteen per cent of a physician’s day, on average, is spent on doctor-patient interaction. Another careful study

of doctors’ time has shown that, during an average eleven-hour workday,

six hours are spent at the keyboard, maintaining electronic health

records. The widespread usage of electronic medical records began

in the nineteen-nineties—it’s taken decades to transform doctors into

data-entry clerks, a process Atul Gawande described,

in this magazine, last year—and yet, in all that time, the adoption of

such systems never met with aggressive pushback. Similarly, doctors were

unsuccessful in resisting the rise of health-management organizations,

which represented only three million patients in 1970 but, by 1999, had

enrolled eighty million. Intended to reduce health-care costs, H.M.O.s

have mainly succeeded in shifting control from doctors to

health-care-system managers. In 1992, Medicare adopted the “relative

value unit,” or R.V.U., a compensation metric that takes into account

the medical service provided and the expense embedded in that service.

The formula’s output—currently $36.04 per R.V.U.—structurally overhauled

physician reimbursement, diminishing the value of non-procedural or

cognitive doctor activity. And yet the major medical professional

organizations went along with the practice, helping to negotiate the

rate, instead of more seriously challenging it. Privately, doctors

feel despair about their appalling working conditions and the

deteriorating doctor-patient relationship. But there have been no

marches on Washington, no picket lines, no social-media campaigns. Why

not? Why aren’t doctors standing up for themselves and their patients? In

theory, doctors could be a powerful force. There are more than a

million physicians in the United States, and around nine hundred

thousand are actively practicing. But the country’s largest medical organization, the American Medical Association, has

only around two hundred and fifty thousand members. (The

next-largest—the American College of Physicians, which represents

internal-medicine specialists—has about a hundred and sixty thousand.)

Most of the smaller societies represent a subspecialty and have

correspondingly fewer members each. The A.M.A. once represented

three-fourths of all American doctors; the growth of subspecialty

societies may have contributed to its diminishment. In any case, there

is no single organization that unifies all doctors. The profession is

balkanized. The power and impact of medical organizations is further diminished

because their priority—supporting their constituents—is often at odds

with the needs of the public. As a long-term member of the American

College of Cardiology, I was impressed with how effectively the

organization lobbied for preserving the reimbursement rates of

cardiologists. (Since cardiology is a procedure-rich specialty,

the introduction of R.V.U.s has been better for us than for, say,

primary-care physicians.) The college also provides educational programs

for its members and puts on annual national meetings. But the A.C.C.

does very little to promote the interests of patients, which is why I

have recently withheld my dues. Like many medical societies, it is

primarily a trade guild centered on the finances of doctors. On

many occasions, medical societies have turned entirely inward, pursuing

business as an end in itself. In the nineteen-nineties, the American

Medical Association announced a product-endorsement agreement

with the Sunbeam Corporation, a manufacturer of humidifiers, ice packs,

heating pads, and the like. Amid an uproar, the A.M.A. backed out of

the deal; Sunbeam sued for breach of contract and won a

ten-million-dollar settlement. The American Heart Association,

meanwhile, continues to rent out its name: a qualifying food

manufacturer can get a heart-check-mark logo, signifying “criteria for

heart-healthy meal” status, on its product’s package for an “administrative fee”

of as much as six thousand dollars. The logo adorns thousands of

low-fat items, such as Cheerios and various breads, which are not in any

meaningful sense heart-healthy. For decades, as part of this program,

the A.H.A. strongly promoted a low-fat diet, advocating the use of

margarine instead of butter, the avoidance of eggs, and the limiting of

saturated fats. As Nina Teicholz and Gary Taubes have shown, in their

respective books “Big Fat Surprise” and “Why We Get Fat,”

this endorsement, which was largely unsupported by data, helped fuel

the obesity epidemic. (The A.H.A. has stood by its recommendations.) Recently, Ivor Benjamin, the president of the A.H.A., appeared onstage

at an Apple special event, where he participated in the announcement of

the newest Apple Watch, which features the ability to detect atrial

fibrillation. Some cardiologists have raised concerns that this

technology will create a wave of false alarms and unnecessary testing

among people who are at low risk for heart-rhythm abnormalities. (Apple

clarified to the Verge that the device is not meant to be a substitute

for a proper EKG.) The American Academy of Family Physicians, similarly,

has accepted a large donation

from Coca-Cola to fund “consumer education content on beverages and

sweeteners,” though the partnership ended in 2015. Sunscreen

manufacturers once paid the American Academy of Dermatology for its endorsement, too, though that program is also defunct. Not all professional medical organizations are so self-interested. Recently, the Endocrine Society railed

against the prices of insulin, which have been raised in lockstep by an

oligopoly of three pharmaceutical manufacturers. (Between 2007 and

2017, the wholesale price of insulin tripled, a spike that has led a

significant proportion of patients to ration their dosing; many have died.) The American Academy of Pediatrics has protested

immigration policies that separate children from their parents. But

such instances are unusual. And they are, on the whole, muted—confined

to written communications in medical journals or position statements

that are only sometimes announced at press conferences. Such

organizations are ill-equipped to advocate for the larger interests of

doctors or patients.

It’s

possible to imagine a new organization of doctors that has nothing to

do with the business of medicine and everything to do with promoting the

health of patients and adroitly confronting the transformational

challenges that lie ahead for the medical profession. Such an

organization wouldn’t be a trade guild protecting the interests of

doctors. It would be a doctors’ organization devoted to patients. Its

top priority might be restoring the human factor—the essence of

medicine—which has slipped away, taking with it the patient-doctor

relationship. It might oppose anti-vaxxers; challenge drug pricing and

direct-to-consumer advertisements; denounce predatory, unregulated

stem-cell clinics; promote awareness of the health hazards of climate

change; and call out the false health claims for products advocated by

celebrities such as Gwyneth Paltrow and Mehmet Oz. This partial list

provides a sense of how many momentous matters have been left

unaddressed by the medical profession as a whole. Tackling any one of

them would be hard; perhaps patient-advocacy groups could join in common

cause. Such an organization could also address the profound

changes that are on the horizon for the medical profession. In 2018, I

had the privilege of leading a review of England’s National Health

Service, focussing on the digital future of medicine. We investigated,

among other things, the role that artificial intelligence could play in

that future. Our economists projected

that, for each minute of keyboard work that could be avoided by

doctors, four hundred thousand hours would be freed up for patient

interaction—the equivalent of hiring two hundred and thirty full-time

physicians. Keyboard liberation is just one of the gifts of time that

machine learning might provide: by synthesizing patient data, artificial

intelligence could speed chart review; it could allow for automated

diagnoses of common conditions such as urinary-tract infections, ear

infections in children, or skin rashes; it could help patients

self-manage high blood pressure or diabetes. All this outsourcing and

off-loading could alleviate the burden on doctors and pave the way for a

revitalized connection with patients. And yet it could also make

medicine worse. Unfortunately, unlike teachers, lawyers, and other

professionals, doctors are predominantly managed by businesspeople. Most

medical administrators know very little about the time it takes to

listen; to do a careful physical examination; to engender trust; to

cultivate a deep relationship with a patient, each of whom has his or

her own life story, pain, anxiety,

and anguish. Over the last four decades, the number of health-care

administrators in the United States has grown by thirty-two hundred per cent, while the number of doctors only increased by one hundred and fifty per cent. Several studies have found that outcomes for patients are better when health-care organizations are run by doctors instead of non-physician executives.

Often, though, increases in productivity in health care have been used

by managers and administrators to squeeze doctors, who are made to see

more patients, read more scans, interpret more slides, and so on.

Already, the emergence of machine learning has led some observers to

proclaim that, in the future, hospitals will be able to do without

radiologists, pathologists, and other medical specialists. That isn’t

true—deep-learning algorithms have, at best, narrow capabilities—and yet

it seems inevitable that managers will ignore medical realities in

favor of the bottom line. Who will be in charge of our health as

we move forward—doctors or their managers? The potential of A.I. to

restore the human dimension in health care will depend on doctors

stepping up to make their voices heard.

Many

would say that such an event is highly unlikely. Doctors

organizing—it’s a crazy idea. The image of residents picketing in front

of a hospital seems to hail from another world. Many people suspect that

doctors suffer from a congenital inability to control their own

destinies. Medical culture seems data-centric, conservative, heads-down,

apolitical. And—surely—doctors are too busy. In fact, there is

plenty of evidence that doctors can organize for the common good. There

are numerous examples of medical activists who work in underserved

communities, fighting against addiction, smoking, e-cigarettes, and

guns. The challenge that lies ahead is building on these disconnected

efforts. Fortunately, there’s a new generation of young doctors who are

digital natives; they’re savvy with social media and recognize the power

of such platforms to affect change. The increasing diversity of the

medical profession is a hopeful sign. Many of the physician leaders who

took on the N.R.A. are women: Esther Choo, an emergency-room doctor;

Judy Melinek, a forensic pathologist; Stephanie Bonne, a trauma surgeon;

Jeannie Moorjani, a pediatrician. When the water in Flint, Michigan,

was revealed to be saturated with toxic levels of lead, the leader of

that exposé was Mona Hanna-Attisha, another pediatrician. Perhaps

dealing with long-standing gender inequities in medicine has helped

these doctors cultivate a willingness to stand up. We’ve all seen how

the student survivors of Marjory Stoneman Douglas High School, in

Parkland, Florida, have organized a national initiative,

with marches, demonstrations, and active nationwide participation. If

these resourceful, energized, impassioned teen-agers can organize a

movement, shouldn’t doctors be capable of organizing, too? Because

of the unique technological moment at which we live, we may not see an

opportunity like this one for generations to come. We have a chance to

affect the future of medicine; to advocate for patient interests; to

restore the time doctors need to think, to listen, to establish trust,

and build bonds, one encounter at a time. For these purposes, and in

these times, an organization of all doctors is necessary. Rebuilding our

relationships with our patients: that is our lane.

It’s time for Democrats to get their facts right on Medicare-for-all

by Pramila Jayapal - Washington Post - August 1, 2019

Pramila Jayapal, a Democrat, represents Washington’s 7th Congressional District in the U.S. House.

In the wake of the second Democratic presidential debate, it is clear that Medicare-for-all has become a defining issue of the 2020 election. Earlier this year, when I introduced our comprehensive, 120-page “Medicare for All Act of 2019,”

I expected attacks from big pharma and for-profit insurance companies.

But I did not expect misrepresentations from Democratic presidential

candidates about what the bill is and is not.

Let’s be clear about the scale of this crisis. The United States currently spends an astronomical $3.6 trillion per year on health care — almost double what peer countries spend — and it is set to increase within 10 years to $6 trillion annually. Pharmaceuticals such as basic insulin cost up to 10 times less in Canada for the exact same drugs. Approximately 500,000 Americans turn to bankruptcy each year because they cannot afford medical costs — and that includes people with insurance.

With so much at stake, facts matter. So let’s get them right.

First, it is a myth that Americans love private insurance.

The vast majority of Americans are deeply frustrated with the

health-care system — even if they have private insurance. Opponents and

pundits often quote polling that suggests support for Medicare-for-all

drops when you tell people that their private insurance plan would go

away. But when polls accurately describe Medicare-for-all,

and explain that you can keep your doctor or hospital, the majority

support increases. People are happy to get rid of private insurance;

they just want to know they can keep their doctors and hospitals, even

if they switch or lose their jobs. Medicare-for-all would let them do

so.

Second, it’s wrong to assert that taxes will rise without talking about what health care currently

costs Americans in premiums, co-pays and deductibles. The average

American family with employer-sponsored insurance incurs more than $28,000 dollars

in health-care costs per year, of which about $15,800, or 56 percent,

is paid by employers. And many argue they still can’t get the care they

need. Americans are smart enough to be asked questions like: Would you

be willing to pay more in taxes each month

if you saved more money by not paying private insurance premiums,

deductibles and co-pays and were guaranteed high-quality health care?

Third, it is simply false that labor unions don’t want Medicare-for-all.

Sure, they fought hard for employer-sponsored health insurance plans

for their workers. But they, above all others, recognize that the rising

costs of insurance premiums are directly related to stagnating wages

and, more and more, the pressure of those costs hurts worker power at

the bargaining table. Take a look at the unprecedented number of unions

that have endorsed our bill, all of which know Medicare-for-all is

necessary.

Fourth, comparisons of Medicare-for-all to the GOP’s push to “repeal and replace”

the Affordable Care Act are simply unfounded. Republicans are the only

ones trying to take away health care. There is absolutely no daylight

between leading on Medicare-for-all and fighting to shore up the ACA

right now, or stopping the GOP from stripping care away. The Affordable

Care Act made profound improvements to our health-care system. But it

was never meant to be the end goal, since it does not address the real

disease in our system: a profit motive that leaves millions either

without access to care, bankrupt or unable to afford medication in the

world’s richest country. We can strengthen the ACA and work toward

Medicare-for-all at the same time. Even former president Barack Obama agrees.

Fifth,

we simply cannot expect to bring down the costs of health care in the

United States without taking on the for-profit insurance and

pharmaceutical corporations, which are raking in billions of dollars at

the cost of American lives. Incremental steps such as a public option might sound appealing but would still leave more than 10 million people without coverage while keeping in place a costly private-insurance middleman that eats up 25 to 30 percent in administrative waste and profits. If we want to achieve true universal health care while containing costs, Medicare-for-all is the only answer.

Finally, Democratic candidates should stop using one-liners from industry front groups and Republican playbooks — such as “Medicare-for-all would shutter hospitals," or telling seniors that “Medicare goes away as you know it. All the Medicare you have is gone.” These claims — amplified by contributions from the private health-care industry

— are designed to incite fear and sow confusion. I’ve spoken with

several hospital CEOs who see Medicare-for-all as a lifeline for their

hospitals — particularly safety-net and rural hospitals that are barely

surviving under the current system. And my Medicare-for-all billimproves Medicare for seniors by adding additional benefits such as dental, vision, hearing and long-term care.

As

the debates continue, I hope that my fellow Democrats will take a good

look at our bill and get the facts right. The Medicare-for-all movement

has overwhelming public support, unprecedented grass-roots organization,

and a serious plan that is ready to change our health-care system right now.

Health

care is the top issue for voters, and they deserve to know the truth

about the solutions we are proposing. I’m willing to debate

Medicare-for-all with anyone — but we owe it to all Americans to stick

to the facts.

The healthcare claims adjudication process in the United States—A picture is worth a thousand words

Health economists analyzing a single payer system don't account for enough of the savings derived from the elimination of our chaotic claims processing methods. These comparative images, one from the US and one from Canada, give us something to think about.

By Henry Broeska- July 26, 2019- Irvine, California

We already know that Canada’s healthcare costs across the board are cheaper by half. And we know that Canadians don’t pay personal premiums, co-pays, or anything out of pocket for their basic medical care, and that includes hospitalizations. So how can Canada cover everyone and do it for less than we pay in the United States?

US-based opponents of government-enabled health insurance schemes would have us believe that countries like Canada do it by rationing access to medical care with long wait lines because inept governments can't manage anything. But that's just 'boiler plate' rhetoric from an ongoing industrial propaganda campaign against the concept of universal healthcare. For over 50 years the American health insurance industry has been using misinformation to keep Americans in the dark. The last thing they want is more concerned citizens understanding how well other nations’ universal healthcare systems work.

Whether single payer or multi-payer, all universal healthcare plans world-wide really practice the same conventions. Successful national healthcare systems have been able to expand coverage to everyone and control costs for five main reasons: 1) They’ve created one comprehensive plan for everyone, 2) they’ve reduced the number of payers allowing everyone to run on a common, secure electronic platform, 3) they’ve reduced medical and administrative costs through rate regulations, 4) they’ve adopted global budgeting for purposes of running hospitals, and 5) they negotiate formula pricing with all drug manufacturers and fiercely guard against the manipulation of generic pharmaceutical supply and pricing. An ancillary benefit of these controls, is that they’ve eliminated the possibility of healthcare fraud, an element that shouldn’t exist in a well-managed system.

But none of those imperatives are features of the US healthcare system. In this article, I'll make comparisons between the US and the Canadian healthcare systems' claims adjudication process to provide evidence that it’s possible to derive far more efficiencies from a single payer system at far less cost.

For no socially beneficial reason...

From World War II on, where all other wealthy countries positioned healthcare as a human right, Americans were persuaded to see healthcare as a market-based commodity. To bolster the concept, insurance companies differentiated their insurance contract offerings with changeable compensations. Nowadays when industrial spokespeople and their political surrogates talk about the importance of 'choices' in health insurance, what they are really reinforcing is the commodity perspective that's been carefully planted in the subconscious of every American over decades.

I often hear my American friends say, “I have good healthcare,” referring to their all-inclusive personal health insurance policy. It’s a statement that’s difficult to understand for someone who didn’t grow up in America. Why do they put the word “good” in front of "healthcare?" In reality, there is only "healthcare," based on best practices. As an American reader, that last sentence may be just as foreign to you as the concept of “good healthcare” is to a non-American. It simply means that other countries have left patient treatment decisions to their doctors, not insurance companies. * But it's that distinction ― the idea that 'healthcare' can be of high quality or inferior quality, or variations in-between ― that's the underlying reason for America’s dysfunctional healthcare system. When it comes to healthcare, Americans are essentially speaking a different language than the rest of the world.

“I just interviewed the German Minister of Health, and it was an exhilarating experience, because it was a totally different language. It was obviously important that everyone should have the same deal in healthcare.” ― Uwe Reinhardt

One of the most powerful visual aids I can imagine to illustrate the administrative difference between Canada and the US is in the area of health insurance 'claims processing.' Claims processing is the receipt and adjudication of a claim filed by the insured against a third-party insurer, often through a Clearinghouse. Claims are accepted or rejected based on the member’s insurance policy. In the US, there are over 4000 health insurance carriers contracting with millions of employers, each offering perhaps hundreds of differently structured health insurance policies. 1

The commercialization of health insurance creates an almost endless number of different contractual terms and conditions adjudicated by thousands of different companies ― each processing claims in their own unique way. Millions of claims are transacted daily in the US. Each claim can trigger hundreds of actions based on strict rules and regulations. Clearinghouses designed to help manage claims, process many trillions of these actions each year.

This ponderous variability across multiple stakeholders makes the US claims payment infrastructure the most complex, the most expensive, and the least efficient claims processing system anywhere in the world. It’s also the reason why the US consumes at least twice as much healthcare administration as any other comparable industrialized country.

Fig 1. (below) depicts the Rube Goldberg-esque processing method we've developed to adjudicate healthcare claims. This image isn't meant entirely to be a lampoon of the system ― it's a true representation of the actual system we use. In fact, the illustration doesn't include nearly enough features; there are layers upon layers of processes and rules that sit below what is shown on top.

Fig 1. US Healthcare Claim System Payment Infrastructure

The main features of the claims adjudication process are: the transmission and receipt of claims, rounds of review, re-submission of denied claims, payment processing, distribution of Explanations of Benefits (EOBs), claims data recording and claims archiving. Every activity and feature seen in the above flow chart fulfills one of those 7 functions in what we call 'the US healthcare system,' even though it is not one, but many systems that interact at some point with everyone in the US ― including the uninsured. But if it only fulfills 7 functions, why should it be as insanely complex as the flow chart?

To get a clearer picture, let’s go to a second chart. The pie chart below accounts for all 329 million Americans by how they interact with the many parts of the US healthcare system. Everyone on American soil is in some way included. Even the uninsured have the right to be treated through the Emergency Medical Treatment And Labor Act (EMTALA). 2 For many who walk into a hospital in medical distress, it's their only and last chance at being treated for acute conditions through a hospital emergency department.

Fig. 2. Total US Healthcare Coverage (millions of ppl) by insurance type (April 2019)

Fig 2. The 8 major segments can be further broken down into many more smaller segments. For example the Employer Segment can be broken down by 4000 different insurance carriers of various sizes, all performing a different claims adjudication process on a perplexing number of proprietary software adaptations.

No matter how someone is insured, or not insured, once they enter the system their data must be accounted for somehow, and that’s all reflected in the claims process. Every claims processing software system on the market must attempt to accommodate every possible claims scenario. Most Providers (physicians, clinics, hospitals, etc,) need to be able to claim against each Payer in each segment. Each of those segments has different rules and different public and private funding sources. The Payers within those segments all have different claims formats. Providers who send in claims on behalf of their insured patients, must format each claim differently depending on their contract with that Payer, the patient's insurance and the applicable state laws.

Incredibly, in the US, there is no universal, standard claims format. Some are still even paper-based. Payers struggle with providing the correct contracts to each Provider, and Providers struggle with each different claims format. Mistakes with the first claims submission in some systems are as common as 'clean claims.' Some unethical Payers deliberately make their claims process as difficult as possible, further complicating the process. A mistake at any level kicks the claim out and the process starts over again. Oftentimes, valid claims, once rejected, are not re-submitted for a variety of reasons. Days, weeks, and months may be added to the revenue cycle for Providers due to delayed payments (and unpaid debt has ballooned across every Provider sector in the past 5 years). In many cases, up to 80% of premium costs are spent dealing with claims, not medical care. It's really the convolution of so many variables that makes claims processing in the US an administrative nightmare ― and very close to the chaos it appears to be.

Henry J. Aaron, the noted American health economist described the system: “I look at the US healthcare system and see an administration monstrosity, a truly bizarre mélange of thousands of payers with payment systems that differ for no socially beneficial reason, as well as staggeringly complex public systems with mind-boggling administered prices and other rules expressing distinctions that can only be regarded as weird.” 3

“Every healthcare system is perfectly designed to get the results it gets.” ― Don Berwick

Obviously anyone designing a healthcare system wouldn't plan it like this. As Henry Aaron suggests, it’s an inherited legacy of bizarre circumstances that we’ve been building on for decades. Nothing about this healthcare system happened through strategic planning; it all happened by accident. 4 Employer-based healthcare was invoked as an ad hoc emergency war measure during World War II. Its enactment as temporary tax relief against employer health spending was a desperate act by the federal government to keep domestic workers from the real possibility of going on strike in the middle of a war effort. It was not meant to last ― and it certainly wasn't meant to be the cornerstone of enlightened nation-building. But the private insurance companies, who profited mightily from the business of healthcare based on the method, lobbied heavily for it to remain in place after the war, so it stayed.

The Digital Revolution

The acceleration of administrative complications within our fragmented healthcare system started with the massive expansion into electronic health records in the 1990s. To get rid of paper, data had to be stored and transferred electronically for the system to work. Similarly, all healthcare-related financial transactions became automated. Computerization meant that insurance companies could expand and offer more differentiated products to a broader market. But computerization also attracted more government scrutiny and more regulations to safeguard private health information ― and to fight an increasing amount of fraud. The heavy regulation of electronic health data started in 1996 with the passage of the Health Insurance Portability and Accountability Act (HIPAA) into federal law, locking down data privacy and security provisions for the protection of medical information. 5

New rounds of regulations and rules were written up every time new programs like the Children's Health Insurance Program (CHIP) and the Affordable Care Act (ACA or 'Obamacare') were enacted. New privacy legislation applying newly adopted standards came into effect. 6 Health Information Technology (HIT) became its own sector of the economy. Growing communications, data-handling and security challenges in turn spawned the emergence of many more third-party specialty technology suppliers, all needing to be profitable as businesses. The burgeoning trend towards more and better HIT that started in the 1990s has only gathered momentum since.

What we've discovered about the American healthcare system intersecting with the digital revolution was that we could rid ourselves much of the paper burden, but not the endless need for more non-clinical workers

The original thinking of all healthcare stakeholders, was that automated claims processing would make life easier. The insurers went all in. They believed that "auto-adjudication," that is, the processing of a claim as soon as it came in ("in real time"), could be achieved electronically. To help expedite the claims process, insurance companies expanded their administrative divisions and technological capacities by building in-house solutions and/or by contracting with third-parties like Cerner, Epic, or McKesson among others. Insurers believed it was just a matter of time before billions of dollars in technology investment would pay off with more competitive health insurance products and savings for consumers. At least, that’s what they told us.

As the fragmented administrative processes became more complex across the industry, they also became institutionalized. By institutionalized, I mean that each one of those small way-points, or boxes in Fig. 1 connected by an arrow to some other function in the process represents an entire area of industry where dozens of technology companies, each with thousands of employees compete for dominance only within that silo of specialized function.

For example, in Fig 1. I've circled one of those little boxes in red. It's an acronym that most of us have never heard of. Electronic Data Interchange, or EDI, became a government-regulated necessity for the secure transfer of health data between multiple organizations. 7IBM, SAP, Microsoft, and a hundred other smaller companies offer their own proprietary EDI solutions for healthcare utilizing a national set of coding and format standards for all electronic transactions related to healthcare. A coalition called "The Workgroup for Electronic Data Interchange" or WEDI, comprises of thousands of individuals and organizations that represent a cross-section of the American healthcare industry.

It’s impossible to do without EDI in US healthcare, but similarly, it’s impossible to do without all of the other complex, rules-based functions as well. They all must connect to make the system work. Over 100,000 rules apply to any healthcare-related insurance transaction performed in the United States. If I picked any of the other way-points, I could point you to third-party activity on a massive industrial scale, where like EDI, scores of companies and thousands of technicians and coders are diligently working to drive efficiencies into the process. In American healthcare the need for HIT innovation never ends, because the administrative burden never stops growing.

Today there are many millions more Americans than just those who work for the insurance companies whose livelihoods depend on the unrestrained growth of our current healthcare system ― and few of them have anything to do with the field of medicine. As one might have guessed, the massive expansion of technology companies saturating the market with software focused on better patient scheduling, automated intake, improved record-keeping, better claims processing, and streamlined billing has not been successful in lowering costs.

Unfortunately, there is no magic bullet that will improve the system's performance. Gains in efficiency, if they can be found at all, are going to be insignificant to the overall cost of the burgeoning administration process. In the current scenario, none are large enough to change the growth rate of healthcare inflation, which far outstrips the growth in American workers' wages.

Comparable industrialized nations have far less complicated health insurance systems. Typically, governments rigorously regulate national health insurance plans that cover most or all citizens with unchanging rules and uniform fee schedules. Such systems cannot help but keep administration costs lower. Compared to countries like Canada, the US healthcare system is more complex by several orders of magnitude. Given the out-of-control administrative costs that the US is experiencing, it’s little wonder that health policy has been a reform target for decades.

“If the rule you followed brought you to this, of what use was the rule?” ― Cormac McCarthy

For those incrementalist reformers who assume that tinkering with the current system will lead to lower costs, the Affordable Care Act proves that isn’t true. We hear that adding "the public option" 8 will cover the rest of Americans with insurance and make everything better. But they are missing the point. The complexity of the US system makes incremental or piecemeal health reform impossible. Unless the current system is abandoned altogether, changing the rules in one part of the system will have enormous effects on every other part of the system. In most cases, there are unintended and costly consequences of changing rules, even when the change is made for noble reasons, like attempting to cover more people with affordable healthcare. The introduction of the Affordable Care Act reduced some direct costs significantly, but increased others, further complicating the picture. Ultimately, the ACA has done nothing to reduce our claims processing problem and has only created more of those little flow chart boxes.

Victimizing the powerless

American consumers deserve much more for their healthcare dollar. Chief among consumer complaints are: dangerous delays in treatments, erroneous denials of care, incorrect bills, surprise charges, and costs not covered by their plans. Bill corrections often take so long to fix that outstanding balances ― for money not owed, mind you ― have already been handed off to collection agencies and members’ credit ratings have been damaged as a result. Sometimes patients don’t even know they are in debt collection until they search their credit score. Unpaid bills lead to other problems that can impact health. Patients requiring care often don’t get seen by their doctors for reasons related to unpaid bills. Another troubling reason for claim denial is the fact that some insurance companies deliberately engage in obstructing the claims process to delay or block payment obligations. This unethical business practice expands profits by using the system's natural convolution. Every legitimate payment denied or delayed goes right to the bottom line of the insurance company. For those insurers who favor their shareholders over their clients, it's relatively easy to game the system on an industrial scale.

A basic question that Americans must ask themselves is: Why am I willing to accept this kind of shoddy treatment from my insurer and from no other vendor?

The US stands alone in this Dystopic model of administrative inefficiency, which is reflected in almost any healthcare-related statistic you care to name. A growing number of Americans – over 40% - have medical debt problems. Close to 31 million Americans have no health insurance at all. About a third of each dollar spent on healthcare in the US goes to supporting the waste, fraud and abuse in the system ― over a trillion dollars each year. *** Incremental changes are not enough.Unless there is a profound change in the way our healthcare system works, our nation, and each of us, are locked into a nearby date with a bleak and uncertain healthcare destiny.

“Masters in our own house we must be, but our house is the whole of Canada.” — Pierre E. Trudeau

For comparison, I’ve created the same claim adjudication flow for a healthcare system like Canada’s, where every citizen is covered (Fig 3) and every physician, clinic and hospital is considered “in network.” Keep in mind that claims for exactly the same medical tests and procedures occur in Canada as the US. But there is no use for all of those 3-letter acronyms that have become regulated institutional fixtures in the United States. Canadians don’t know what EDI, HRAs, HSAs, HMOs, PPOs, MCOs or ACOs are. In each Canadian province, there's only need for one secure interface between 2 computers for the adjudication process to work. To put it into simple terms that Americans understand, Canadians are all members of the same plan with the same coverage.

To make a claim for a service provided to a patient, a doctor or his office staff simply enter the provincial tariff codes into a database hosted by the Payer. For Providers, there is only one set of prices for each province based on a fee-for-service payment structure. These prices are maintained for years with an annual inflation factor added. For patients, there is nothing to do; no plans to choose, no paperwork, no bills. Less work and fewer rules means administrative costs are lower.

Fig. 3 Healthcare Claim Payment Infrastructure in Single Payer System

Depending on area of practice, 95-100% of physicians’ claims are paid by the provincial Payer every 15 days. That’s the length of the revenue cycle in Canada ― two weeks. Physicians never worry about collections or bad debt. The flow chart for the Canadian healthcare system in Fig. 3 shows why. It's clean, simple, and precise, with no need for any of the billion dollar technology features and onerous government regulations that must be applied to the same adjudication process in the US. And fraud? The system is so simple and transparent that fraud in the Canadian healthcare system is rare and nearly unheard of.

In the case of Canadian hospitals, global budgets are used as a cost-containment method to control expenditures. Global hospital budgets set caps on spending and are highly effective for controlling medical inflation. Virtually all healthcare services in the hospital are covered and paid for by the public Payer. Since the hospital managers know what it cost to run the hospital in the previous year, and they know the rate of medical inflation, they can predict with some accuracy how much they will need to run the hospital in the following year. Except for a relatively few 'hospitalists,' physicians work independently in the hospitals and submit bills to the public Payer, just as if they were submitting them from their clinics, which they operate as small businesses. Here again, like clinics, the hospital system is invisible to patients who receive no bills or paperwork of any kind.

It should tell us something that none of the complex claims adjudication software systems that are sold in the US are even offered for sale outside of the United States. And the standardized software used across the healthcare system in each Canadian province takes a small fraction of the labor force needed in the US to enter the data.

"Change the rule and you will get a new number.” ― W. Edwards Deming

The administrative comparisons between Canada and the US are stark. It takes about 8 billing clerks to enter billing data for a large ~900-bed Canadian hospital. Contrast that to Duke University where their 957-bed hospital requires the employment of 1,600 billing clerks and an additional unknown number of billing consultants. 9

In a well-known comparative study, administrative overhead accounted for 11.7% of private plan healthcare expenditures in the US, compared to 1.9% for provincially administered plans in Canada. 10 Hospital administration costs in Canada are around 11% of total operational costs while in the US they are closer to 26%. And medical inflation rates in the US are running at over twice the inflation rate of Canada and other OECD countries.

In the topsy-turvy scenario that's playing out, healthcare stakeholders have placed higher value on a good revenue cycle strategy than the delivery of healthcare itself.

Meanwhile, back here in America, all healthcare stakeholders are hiring more low-level clerks and administrators to manage the choke-points. **** In this scenario there is no need for more physicians who would only generate more paperwork ― best to curtail the care to lessen the admin burden, and raise prices to pay for the new hires. In the topsy-turvy scenario that's playing out, healthcare stakeholders have placed higher value on a good revenue cycle strategy than the delivery of healthcare itself. The result? Higher healthcare premiums, higher co-pays, more high-deductible plans, a high rate of inflation that guarantees significantly higher insurance plan costs each year, and far less coverage than ever before. The other result that’s perversely and indefensibly higher is insurance company profitability. It doesn't matter that the insurers have failed spectacularly in their mission to provide affordable plans to Americans. It only means that ‘whoever has the gold makes the rules.’

Fig. 4 Growth in Physicians and Administrators US Healthcare System 1970-2017

Cleaving the Gordian Knot

The Canadians have created a plan benefit design that is comprehensive and their laws have given provincial governments the regulatory teeth to make it work. They understand that the more players who are allowed to represent more variable and alterable plans, the more administrative problems it creates for Providers and patients alike. The more Payers and plans ― what we like to call ‘choice,’ in America ― the greater the reduction in cost-effectiveness. Although opponents of 'socialized medicine' typecast it as 'Americans under the thumb of Big Government,' it's impossible to conceive of a system that's more bureaucratic, wasteful and corrupt than what we have now.

According to a Harvard study, we put up with $60 billion in overpayments (Americans being charged and paying more than they should have been billed) Annual care for the uninsured and under-insured generates $85 billion in uncompensated costs covered by us, the taxpayers. 11 There is $272 billion in medical billing fraud each year. 12 That means the American system 'absorbs' more in unrecoverable costs due to fraud each year than the entire Canadian healthcare system costs to run! ('absorbs'=recovered out higher premiums we all pay) There are also $262 billion in medical claims that are denied, leaving patients to scramble to either get the denial decision reversed or find an alternate means of financing their care. 13Physicians give away $125 billion in free services for rejected claims each year. 14 Uncompensated care provided by American hospitals is over $38 billion per year. 15

Attempts to reclaim these losses cost an additional untold billions in administrative costs, not to mention the millions of hours of unpaid time spent by patient families attempting to get the medical care they need. In fact, every pointless and unnecessary cost in the system is recovered on the backs of the American consumer – you and me. That’s because insurers don’t endure the cost; they simply recoup losses by increasing premiums, raising deductibles and decreasing coverage.

Through all of this, it's key to remember that the number of uninsured Canadians is zero, and the personal debt accumulated for insured medical care is zero. Because the provincial plan pays, no Canadian has ever been denied care or accumulated personal debt for a medical reason. Canada can offer this to everyone because they've wrestled their costs to the ground. Canada and Scotland have the lowest hospital administration costs in the world. 14There is much to be said about the simplicity and practicality of viewing healthcare as a right, and not a commodity.

If we truly believe that the private sector can deliver cheaper healthcare more efficiently than the public sector, then all Americans deserve an explanation from both industry and lawmakers as to how private healthcare that costs twice as much as it does in countries with so-called ‘socialized medicine’ is benefiting us as taxpayers.

Lured by the insurance companies and the drug manufacturers with the assurance of re-election campaign funding (insurance companies are often the biggest single contributors to re-election campaigns in the US), American lawmakers still drone on about more market forces being the answer to the American healthcare system becoming more efficient. 16Health economists, in trying to lay blame for high healthcare costs, will write tomes on the supply shift needed to balance the demand shift and the a shortage of doctors creating artificially high prices, but will never once mention the obvious claims processing problem.

The accelerating loss of health insurance coverage year-over-year portends a disastrous outcome for the health and welfare of tens of millions of Americans if we don’t act immediately. At this point, invoking ideologies is not useful to honest policy discussion. To eliminate bias, we must identify and marginalize lawmakers who take re-election campaign funding from private insurance and pharmaceutical companies. Every politician who does, is simply a shill for the industry. We must recognize that political self-interests have turned our healthcare system into both a public health risk, 17 and one of our greatest national security threats. 18

The Canadian healthcare system is not perfect. Compromises in the face of aging populations must be made until funding and capacities are realigned. Although Canadians worry about how to finance their healthcare system (news flash: every country does) *****, they do a good job of providing care to everyone who needs it for less than half of what we pay here. They do it by prioritizing care for those who need it most, prudently managing the claims process and making sure that expenditures are kept within budget forecasts.

If a picture is worth a thousand words, then the two comparative process diagrams I’ve illustrated surely provide an eloquent answer to our healthcare problems. But the gains found by eliminating the tortuous claims process only occurs by moving to a simpler system. It’s time to take a serious look at how other countries deliver healthcare for half of what we pay before the harm the current system inflicts upon the country becomes an unrecoverable condition.

Conclusions:

1) In the context of American healthcare, the word "choice" is a doublespeak euphemism for barrier, denial, and unaffordable cost.

2) If everyone in a healthcare system was entitled to equal access to the same comprehensive services for a standard of healthcare based on best practices, there would be no reason for the convolution of the claims adjudication process we experience in the US. It would look like Canada's.

3) The administrative simplicity of the single payer model does not waste financial resources that are more appropriately used for patient care.

4) Health insurance companies contribute directly to high healthcare costs in the United States by driving up prices and by generating ever more administrative waste.

5) "Socialized medicine" is not a negative result of healthcare reform. Public healthcare systems exist only to provide the people they serve with the greatest value in health services. Insurance companies are in business to increase their revenues and are therefore in a conflict of interest with the public good.

FOOTNOTES * The greatest fear of the insurance companies is that they will be left out of risk assumption and therefore be denied the ability to restrict spending on the client's treatment in some way. For this reason they have made up the lie that under any government sponsored healthcare program, it will be the government who will make decisions about patient's care. In fact, in Canada and other countries, doctors are the only ones who make decisions about the patient's medical care. Unlike in the US today, private insurance companies (if they exist at all, i.e.: Germany) assume no risk in any countries with universal care and therefore play a much reduced role in the distribution of health insurance. ** An electronic medical billing clearinghouse acts as a middleman that takes medical claims information and then submits it electronically to insurance companies. They perform the functions of: eligibility verification, determining the patient portion to be paid, Electronic Remittance Advice (ERA), payment and adjustment updates, claim status reports, claim rejection analysis (error coding), editing and correcting of claims online, Printing out of claims, mail services, tracking and management of claims, patient statement services, and all support in real-time. *** The prices for all medical goods and services including drugs and physician’s fees continue to grow at over twice the rate of inflation. Hospital prices have increased almost four times in the past 4 decades. The recent hospital merger trend has significantly accelerated the costs of hospitalization. Overall, US healthcare spending has increased from 6% of the GDP in 1967 to around 18% ($3.5 trillion) in 2019. Canada’s healthcare spending was also at 6% in 1967 and remains stable at around 11% of GDP today. **** The single electronic system by which healthcare claims are adjudicated in Canada is regarded as a tool. In the US, the claims adjudication process has turned into an industry on its own, employing millions of people. The complexity of the process with its multiplicity of plans and contracts, medical codes that may or may not be billable, rules that are different in each American state, different networks, different formularies, different medical Providers charging differently, different shares of public and private funding, multiple accounts to draw from for the same claim, different cost-sharing arrangements, inconsistent deductibles and reimbursement levels, even within the same plan ― and on and on and on ― make it impractical to apply algorithms. Algorithms are computations that deal with finite numbers of precisely defined successive states, eventually producing a final outcome. Algorithms have made consumer-facing companies like Amazon, Facebook, Snapchat, and Uber successful. But health insurance claims are more like snowflakes ― no two are exactly the same, making algorithms that depend on ‘sameness’ difficult to adapt. No matter how many feedback loops you build into the process, there continue to be so many computational failures along the algorithmic flow that real humans must intervene every so often to resolve problems and move the claim forward. Human touches are expensive and time consuming ― and make the fantasy of real-time adjudication a false choice. ***** Less than a decade ago, France was rated as the best healthcare system in the world, touted in Michael Moore's 'Sicko.' Now it's reeling from budget projections that weren't met and failure to plan for staffing needs. President Macron has vowed to fund it appropriately. In 2019, Britain's healthcare system is suffering under budget austerity. Similarly, first-class care but long queues are frustrating Swedes. Healthcare in the Netherlands is rated as the world's best but the Dutch are paying more in taxes for healthcare than ever before. Despite all of these problems, the healthcare systems in these countries are rated an order of magnitude higher by all measures than the US healthcare system, costing half as much and producing better outcomes and higher life expectancies. There are challenges facing all national healthcare systems, underscoring the fact that ongoing vigilance and preparation is paramount. A successful healthcare system is forever aspirational; it is a journey, not a destination.

3) H.J. Aaron , “The Cost of Health Care Administration in the United States and Canada—Questionable Answers to a Questionable Question,” New England Journal of Medicine 349 , no. 8 ( 2003 ): 801 –303. https://www.nejm.org/doi/pdf/10.1056/NEJMe030091

6) Institute of Medicine (US) Committee on Health Research and the Privacy of Health Information: The HIPAA Privacy Rule; Nass SJ, Levit LA, Gostin LO, editors. Beyond the HIPAA Privacy Rule: Enhancing Privacy, Improving Health Through Research. Washington (DC): National Academies Press (US); 2009. Glossary. Available from: https://www.ncbi.nlm.nih.gov/books/NBK9572/

10) Woolhandler, Steffie , Terry Campbell , and David U. Himmelstein, Costs of Health Care Administration in the United States and Canada, New England Journal of Medicine 349, June 2003.: 768, 775. https://www.nejm.org/doi/full/10.1056/NEJMsa022033

17) Institute of Medicine (US) Committee for the Study of the Future of Public Health. The Future of Public Health. Washington (DC): National Academies Press (US); 1988. 1, The Disarray of Public Health: A Threat to the Health of the Public. Available from: https://www.ncbi.nlm.nih.gov/books/NBK218222/

The vast majority of Americans have very little need for medical

care in any given year; that's why most people are satisfied with their

coverage. But what if they have a big claim?

The vast majority of Americans have very little need for medical

care in any given year; that's why most people are satisfied with their

coverage. But what if they have a big claim?

No comments:

Post a Comment