The View From Here: What are we talking about when we talk about Medicare for All?

Bernie Sanders' bill is more than health care reform, it's a restructuring of the national economy.

by Greg Kasich - Maine Sunday Telegram - April 14, 2109

With Bernie Sanders’ Medicare for All bill introduced in the Senate, let’s get ready for a big debate about what it really is. Most of it will take place on the Democratic presidential

campaign trail, where all the major contenders say they are for it, but

they all seem to mean something a little different. And Republicans will be having their own debate, trying to

figure out which monster under your bed is a scarier one – Medicare for

All or a Green New Deal. Before things heat up too much, it might be worth talking about

what Sanders’ version of “Medicare for All” is by starting with what it

is not. For one thing, it’s not Medicare, at least not as we know it.

Medicare is a half-century-old single-payer insurance program that

covers hospitalization and doctor visits for people who are 65 and

older, as well as younger people with disabilities. Unlike Sanders’ bill, Medicare does not cover long-term care,

and it does not cover prescription drugs, unless Medicare recipients buy

a separate, optional policy. Medicare doesn’t cover dental care or

glasses, but Sanders’ bill would. People on Medicare usually buy private insurance to supplement

their coverage unless they are low income enough to qualify for

Medicaid, the federal and state health care partnership. Sanders’ bill would wipe that out, giving everyone access to

health care without private insurance, deductibles, co-pays or any other

out-of-pocket costs. The bill does not nail down a funding source, but Sanders says

that shouldn’t be a problem. If you add up what’s spent through

government programs, employer-provided private insurance, tax

expenditures and out-of-pocket expenses, the United States already

spends more on health care than any other country in the developed world

– twice as much as Canada – and has worse results. Sanders figures we

could actually spend less on a better system. Which gets to what this version of “Medicare for All” really

is. It’s a restructuring of the economy. By reallocating who pays for

health care, Sanders would be narrowing the gap between rich and poor in

a way we have not seen since the old New Deal in the 1930s. Here’s how it might work: About half of Americans get their

health insurance through work. Right now, a CEO making $300,000 a year

and a janitor at the same company making $30,000 pay the same insurance

premium. If the employer tries to lower its costs by moving to a less

generous plan – one with higher deductibles, or fewer covered benefits –

the CEO and the janitor would have the same out-of-pocket

responsibilities, even though one’s pocket is deeper than the other’s. If both employees were covered by the new Medicare, and if it

were funded by a progressive income tax, the CEO would be paying much

more than the janitor. It would be easy to structure the tax so that

most people would be paying less for their health care. Since there are fewer rich people than not-rich ones, this should be a winning policy in a democracy. Which leads to the other thing the Medicare for All is: A theory of democratic social change. Sanders is not going to pass his bill by winning a debate in

the Senate – there will not be a debate in the Senate unless Mitch

McConnell wants one, and he doesn’t. He’s not going to lobby his buddies

in the cloakroom or the gym. Sanders doesn’t seem to like other

senators, and they don’t seem to like him. And Sanders is not going to pass his bill by getting the

hospitals, insurance companies and other interested parties to sit

around the table and hammer out a bipartisan deal that everyone can live

with. Sanders is not interested in a House bill that aims to fix some

of the flaws in Obamacare. He’s not motivated to shave a few people off

the list of the uninsured. The only way Medicare for All has a chance (at least as

envisioned by Sanders) is for its supporters to win elections, not just

the presidency but many elections all across the country. The last time any legislation approaching this magnitude became

law was 1965, the year when Lyndon Johnson signed the Voting Rights

Act, Medicaid and the original Medicare. The previous November he had

been returned to office with 63 percent of the popular vote, along with

68 Democratic senators and a 145-representative Democratic advantage in

the House. If Medicare for All is the biggest social program ever

conceived in our history, passing it would take that kind of landslide,

moved by the biggest social movement we’ve ever seen. To work in coalition with people who they don’t like very much

and focus on economic justice, millions of people would have to put

aside some issues that matter very much to them.

Over the next year, we’ll find out if that momentum exists.

It’s what we’ll we be talking about when we talk about Medicare for All.

Why Trump’s New Push to Kill Obamacare Is So Alarming

by Nicholas Bagley - NYT - March 27, 2019

Attorney General William Barr was supposed to be a voice of reason in the Trump administration. An old Washington hand, he had the stature and the backbone to protect the Justice Department from a White House that often seems to disdain the rule of law.

Turns out it isn’t so.

In a stunningtwo-sentence letterto a federal appeals court, the Justice Department announced on Monday that it would now seek the invalidation of the entire Affordable Care Act — every last one of its thousands of provisions.

The irresponsibility of this new legal position is hard to overstate. It’s a shocking dereliction of the Justice Department’s duty, embraced by Republican and Democratic administrations alike, to defend acts of Congress if any plausible argument can be made in their defense.

Nor is the Affordable Care Act some minor statute that can be shoved aside without disruption. It is now part of the basic plumbing of the American health care system. It guarantees protections for people with pre-existing medical conditions. It expanded Medicaid to cover12.6 million more people, and it offers crucial protections to the156 million Americanswho get insurance through employers.

Beyond that, the law forces insurers to cover preventive care and contraception without charge; changed how hospitals and physicians bill for their services; requires fast-food restaurants to post calorie counts; cut hundreds of billions of dollars of Medicare spending; imposed hundreds of billions of dollars in taxes; and much, much more.

Unceremoniously ripping up the law would inflict untold harm on the health care system — and on all Americans who depend on it. Yet the Trump administration has now committed itself to doing just that.

The letter was submitted in a pending case, brought by a group of red states, in which a federal judge in Texas ruled that no part of the Affordable Care Act could stand. The judge reasoned that Congress created a constitutional problem when, in its big tax reform bill in 2017, it eliminated the financial penalty for going without insurance.

Because of that purported constitutional defect, the court held, the entire law had to fall. The ruling was indefensible: Legal scholarsacross the boardcriticized it as outrageous and predicted it would almost surely fall upon appeal.

Indeed, even the Trump administration couldn’t bring itself to argue that the entire law should be scrapped. It agreed there was a constitutional problem, but said that the right remedy was to keep most of the law in place.Only those partsrequiring private insurers to sell coverage at the same price to healthy and sick people alike — the protections for people with pre-existing conditions — would have to be struck.

That, too, was an outrageous position. It flouted the Justice Department’s duty to defend, a solemn duty, and one that goes to the heart of the rule of law. Without it, the sitting administration could pick which laws it wanted to defend in the courts and which it wanted to abandon. Laws could rise or fall based on nothing more than partisan disagreement. That’s inconsistent with a constitutional system that assigns to Congress — not the president — the power to legislate.

And so, at the confirmation hearing on his nomination to become attorney general, Mr. Barrsaidthat he would review the Justice Department’s position in the Texas lawsuit. Apparently he did just that — but instead of mounting a vigorous defense, he doubled down on killing Obamacare. It’s as if Mr. Barr said to his predecessor, Jeff Sessions: “You thought your position was crazy? Hold my beer.”

Does the administration really think that the very position it advanced just months ago is so untenable that it must now adopt one that is even more extreme?

The shift in legal position won’t make much of a difference in the lawsuit itself. Because a group of blue states has intervened, the appeals court will hear a full-throated defense of the law. Most observers expect the court to uphold the Affordable Care Act; if so, the Supreme Court may choose not to hear the case.

But the Trump administration has signaled loud and clear that its campaign against Obamacare is not over; that it will stop at nothing to achieve in court what it could not achieve in Congress; and that it doesn’t care how many people are hurt if the Affordable Care Act is undone.

It has also put health care back at the center of the political conversation. Republicans already took a beating on the issue in the fall midterm elections, and Democrats, whoreleased a bill in the Houseto strengthen the Affordable Care Act, want to keep running on it. They’ll be sure to remind voters of the Trump administration’s zealous commitment to taking away their health care.

Along the way, the Justice Department has trashed the duty to defend. That’s not to be taken lightly. The duty is a close cousin to the president’s constitutional duty to enforce the law. If the Justice Department really thinks that Obamacare is so blatantly unconstitutional that it can’t be defended, that implies that the president is violating the Constitution whenever he applies it.

It’s not hard to see that as an incipient justification for refusing to enforce any law that the president believes to be unconstitutional, however ridiculous or partisan that belief might be. Hopefully it doesn’t come to that. But the failure to defend the Affordable Care Act is an ominous sign to anyone who cares about the rule of law.

'How Will You Pay for It?' Bernie Sanders Tackles Key Question on Medicare for All

by Jake Johnson - Common Dreams - April 10, 2019

Sen. Bernie Sanders is not ducking the key question constantly posed to Medicare for All supporters by journalists, fellow members of Congress, and critics: "How will you pay for it?"

"'How are you going to pay for it?' That is the question that

bookends nearly every media conversation that takes place on Medicare

for All. The straightforward answer is, we already are." —Sen. Bernie Sanders' office

In a white paper (pdf) released Wednesday alongside the 2020 contender's updated and improved Medicare for All legislation,

Sanders' office outlined a number of possible funding mechanisms for

the comprehensive bill and detailed the enormous savings the U.S. would

reap by transitioning to single-payer.

"Every major industrialized nation on Earth has made healthcare a

right, provided universal coverage to all, and achieved far better

health outcomes in terms of life expectancy and infant mortality

rates—all while spending far less per capita than we do," the paper

states. "Please do not tell us that the United States of America, the

wealthiest nation in the history of the world, cannot do the same."

The paper lists a number of policy changes that could help raise revenue for Medicare for All, including:

A 70 percent top marginal tax rate on Americans earning over $10 million per year;

A 77 percent top tax rate on estates above $1 billion;

A tax on "extreme wealth";

A "fee on large financial institutions";

A "7.5 percent income-based premium paid by employers, exempting the

first $2 million in payroll to protect small businesses"; and

A four percent "income-based premium paid by employees, exempting the first $29,000 in income for a family of four."

While acknowledging its list is not exhaustive, Sanders' office

said the U.S. has a large "variety of options available to support a

Medicare for All, single-payer healthcare system."

"Under every single one of these options the average American family

will save thousands of dollars a year because it will no longer be

writing large checks to private health insurance companies," the

document says.

"The American people are increasingly clear. They want a healthcare

system which guarantees healthcare to all Americans as a right. They

want a healthcare system which will lower healthcare costs and save them

money." —Sen. Bernie Sanders

The white paper also emphasizes the massive savings American families

and the U.S. overall would reap by transitioning from the wasteful

for-profit system to Medicare for All, which would eliminate premiums,

deductibles, and co-pays.

"'How are you going to pay for it?' That is the question that

bookends nearly every media conversation that takes place on Medicare

for All," the paper states. "The straightforward answer is, we already

are."

"Unlike other government outlays—for example, a ship for the

Navy—Medicare for All does not represent any new spending at all," the

document continues. "Instead, it represents a rebalance of how our

current dollars are spent."

Under the for-profit status quo, Sanders' office points out, the U.S.

federal government is on track to spend $59.65 trillion on healthcare

between 2022 and 2031.

By contrast, according to two studies published last year, Medicare

for All would cost the U.S. significantly less while providing

comprehensive healthcare to all Americans.

"According to estimates from the conservative Mercatus Center,

under the Senate's Medicare for All legislation, [national healthcare]

expenditures will drop by approximately $2 trillion," the paper notes.

"Another study released by PERI

at the University of Massachusetts found that 'Medicare for All could

reduce total healthcare spending in the U.S. by nearly 10 percent,'

resulting in more than $5 trillion in savings."

Medicare for All would also save the U.S. money by slashing prescription drug costs, Sanders' office argued.

"If the U.S. joined the rest of the industrialized world and

negotiated with the pharmaceutical companies to lower prices, our

country could save up to $113 billion per year," the paper states.

The paper closes with a call for "vigorous debate" on the ideal path to funding Medicare for All.

As Vox's Sarah Kliff noted, the items offered by Sanders' paper "could no doubt be used to finance a national healthcare system."

"But eventually," Kliff added, "someone is going to have to pick which items on this list become law—and that's where things get tough."

"Unlike the Republican leadership in Congress which held no hearings

on their disastrous bill which would have thrown 32 million people off

of health insurance," Sanders' office concludes, "we will continue to

get the best ideas from economists, doctors, nurses, and ordinary

Americans to guarantee healthcare as a fundamental right."

The white paper was released as Sanders officially introduced his Medicare for All legislation with the support of 14 Democratic co-sponsors and more than 60 progressive advocacy groups.

"The American people are increasingly clear," Sanders said in a statement.

"They want a healthcare system which guarantees healthcare to all

Americans as a right. They want a healthcare system which will lower

healthcare costs and save them money. They want a healthcare system

which will guarantee them freedom of choice as to which doctor or

hospital they can go to."

"In other words," the Vermont senator added, "they want Medicare for All, and that's what we will deliver to them." https://www.commondreams.org/news/2019/04/10/how-will-you-pay-it-bernie-sanders-tackles-key-question-medicare-all?

'I Felt Americans Needed to Know': Insurance Industry Whistleblower Gives Glimpse of Effort to Crush Medicare for All

by Jake Johnson - Common Dreams - April 11, 2019

In an effort to inform the public about the corporate forces working

to crush Medicare for All, an employee at the insurance giant

UnitedHealthcare leaked a video of his boss bragging about the company's campaign to preserve America's for-profit healthcare system.

"I felt Americans needed to know exactly who it is that's fighting

against the idea that healthcare is a right, not a privilege." —whistleblower

"I felt Americans needed to know exactly who it is that's fighting

against the idea that healthcare is a right, not a privilege," the

anonymous whistleblower told the Washington Post's Jeff Stein.

During an employee town hall in February, Stein reported on Friday, UnitedHealthcare CEO Steve Nelson boasted about how much his company is doing to undermine Medicare for All, which is rapidly gaining support in Congress.

"One of the things you said: 'We're really quiet' or 'It seems like

we're quiet.' Um, we've done a lot more than you would think," Nelson

said. "We are advocating heavily and very involved in the conversation.

Part of it is trying to be thoughtful about how we enter in the

conversation, because there's a risk of seeming like it's self-serving."

According to the Post, which did not publish the video of

Nelson's remarks, the executive said his company "opposes Medicare for

All because it excludes the private sector, which he said does a better

job of delivering healthcare than the government, and said he doubted

how a single-payer system could be funded or effectively administered."

The UnitedHealth employee who leaked The Post

this video says: “I felt Americans needed to know exactly who it is

that’s fighting against the idea that healthcare is a right, not a

privilege."https://t.co/fQAXmVTmdf

Nelson's remarks were leaked just days after Sen. Bernie Sanders (I-Vt.), a 2020 presidential contender, unveiled his improved Medicare for All bill

with the support of 14 Democratic senators and over 60 progressive

organizations representing nurses, physicians, and consumer advocates.

Sanders called out insurance and pharmaceutical industry greed in a statement

following the introduction of his bill, which would virtually eliminate

the private insurance industry and provide comprehensive healthcare to

every American.

"When the people begin organizing against private insurance, the

lonely insurance executives turn to their only friends: the elected

officials beholden to their cash." —Tim Faust

"In my view, the current debate over Medicare for All really has

nothing to do with healthcare. It's all about greed and profiteering,"

said the Vermont senator. "It is about whether we maintain a

dysfunctional system which allows the top five health insurance

companies to make over $20 billion in profits last year."

On Friday, Sanders took to Twitter to send Nelson a message.

"When we are in the White House your greed is going to end," Sanders wrote.

Our message to Steve Nelson and UnitedHealthcare

is simple: When we are in the White House your greed is going to end. We

will end the disgrace of millions of people being denied health care

while a single company earns $226 billion and its CEO makes $7.5 million

in compensation. https://t.co/OafOIT92H9

UnitedHealth Group, the parent company of United Healthcare, raked in

around $17 billion in profits and "spent about $8 million on lobbying

efforts" in 2018, Stein reported.

UnitedHealthcare's fight against single-payer, Stein noted, comes

"amid a broader push from the health insurance industry to prevent

legislation to enact Medicare for All from getting off the ground,

including by trying to direct Democrats toward more centrist efforts and

reject plans that would effectively legislate many of the companies out

of existence."

"[A]bout half a dozen representatives of lobbying firms said they had

pushed for meetings with Democrats over single-payer and other proposed

government expansions of healthcare," according to Stein.

In a statement to the Post, Medicare for All campaigner and

policy expert Tim Faust said, "When the people begin organizing against

private insurance, the lonely insurance executives turn to their only

friends: the elected officials beholden to their cash."

One of the industry-backed groups leading the fight against Medicare

for All is the Partnership for America's Health Care Future, which is comprised of major pharmaceutical and insurance interests.

The Partnership launched a six-figure ad campaign against Medicare for All earlier this year, warning the popular proposal "would cause massive disruption to the current healthcare system."

After the Partnership launched its first digital ad against Medicare for All in January, Wendell Potter—an insurance industry executive-turned-whistleblower—said, "It's almost impressive how many lies they're able to fit into such a short clip."

Watch Potter's breakdown of the Partnership's ad: https://www.commondreams.org/news/2019/04/12/i-felt-americans-needed-know-insurance-industry-whistleblower-gives-glimpse-effort?

Republican Health Care Lying Syndrome

by Paul Krugman - NYT - April 1, 2019

There are three kinds of lies: lies, damned lies and Republican claims about health care.

O.K., it’s not news that politicians make misleading claims, some more than others. According to a running tally kept by Daniel Dale of The Toronto Star, as of Monday morning, Donald Trump had said 4,682 false things as president.

But

G.O.P. health care claims are special, in several ways. First, they’re

outright, clearly intentional lies — not dubious assertions or

misstatements that could be attributed to ignorance or misunderstanding.

Second, they’re repetitive: Rather than making a wide variety of false

claims, Republicans keep telling the same few lies, over and over.

Third, they keep doing this even though the public long ago stopped

believing anything they say on the subject.

This syndrome demands

an explanation, and I’ll get there eventually. Before I do, however,

let’s document the things that make G.O.P. health care lies unique. [For an even deeper look at what’s on Paul Krugman’s mind, sign up for his weekly newsletter.]

First,

as I said, I’m not talking about mere dubious claims. When Trump

officials insisted that the 2017 tax cut would lead to a decade of

miraculous growth, their claim made no sense in terms of the underlying economics,

and it flew in the face of decades of evidence. But it was a

prediction, not a statement of fact, and it’s conceivable (barely) that

Trump’s people actually believed it.

But when Mick Mulvaney, the acting White House chief of staff, went on TV Sunday to declare that “every single plan” Trump has put forward “covered pre-existing conditions,” that was just a lie.

Here’s what the Congressional Budget Office said

in its assessment of the Republicans’ American Health Care Act, which

would have caused 23 million to lose coverage, and would have passed if

John McCain hadn’t voted “No”: “People who are less healthy (including

those with pre-existing or newly acquired medical conditions) would

ultimately be unable to purchase comprehensive nongroup health insurance

at premiums comparable to those under current law, if they could

purchase it at all.”

But Mulvaney’s pre-existing conditions lie,

along with his lie about nobody losing coverage if the lawsuit against

Obamacare succeeds, was normal by G.O.P. standards. Which brings me to

the second reason this particular form of lying is exceptional:

Republicans just keep telling the same lies, over and over. Again and

again they have promised to maintain coverage and protect pre-existing

conditions — then offered plans that would cause tens of millions to

lose health insurance, with the worst impact on those already suffering

from health problems.

The funny thing — which is my third point —

is that almost nobody seems to believe these lies. On the eve of last

year’s midterm elections, the public trusted Democrats over Republicans

to protect Americans with pre-existing conditions by 58 percent to 26

percent. A margin this big tells us that even Trump supporters knew

their man was lying on this issue.

So what’s behind the persistence of R.H.L.S. — Republican health care lying syndrome?

Well,

public opinion here is clear: Americans want everyone to have access to

health care. There isn’t even that much of a partisan divide: An overwhelming majority of Republicans don’t believe insurance companies should be allowed to deny coverage or charge more to those with pre-existing conditions.

This public near-unanimity is one reason Medicare is so popular. Getting older — and thus joining a group with much higher average health costs than the rest of the population — is, after all, the ultimate pre-existing condition.

But there are only two ways to cover people with pre-existing conditions, and both are anathema to conservative ideology.

One is to have taxpayers pay the bills directly, which is what Medicare does.

The

other combines regulation and subsidies. Insurance companies must be

prohibited from discriminating based on medical history — a prohibition

that must include preventing them from issuing bare-bones policies that

will appeal only to those in good health — but that won’t do the job by

itself. Healthy people must also be induced to sign up, to provide a

good risk pool, which means subsidizing premiums for those with lower

incomes and, preferably although not totally necessary, imposing a

penalty on those without insurance.

If the second option sounds

familiar, it should. It’s what countries like the Netherlands and

Switzerland do; it’s also a description of, you guessed it, Obamacare.

But

Republicans cannot admit that the only way to protect pre-existing

conditions is to emulate Democratic policies. The party of Eisenhower,

or even the party of Nixon, might have been able to do such a thing, but

the party of Fox News cannot.

Nor, however, do Republicans dare

admit that they have no interest in providing protection that a vast

majority of voters demands. So they just keep lying.

You may, by

the way, have heard talk about G.O.P. members of Congress opposed to

Trump’s new health care push. But they share his goals; they’re just

questioning his timing. The whole party still wants to take away your

health care. It just hopes to get through the next election before you

find out. https://www.nytimes.com/2019/04/01/opinion/republicans-health-care.html?smid=nytcore-ios-share

Don’t Make Health Care a Purity Test

by Paul Krugman - NYT - March 21, 2019

We’re now in the silly season of the Democratic primary — a

season that, I worry, may last all the way to the nomination. There are

many honorable exceptions, but an awful lot of reporting seems to be

third order — not about the candidates, let alone their policy

proposals, but about pundits’ views about voters’ views of candidates’

electability. It’s a discussion in which essentially nobody has any idea

what he or she is talking about.

Meanwhile, however, there are

some real continuing policy debates. They’re not mainly about goals:

Whoever the Democrats nominate will profess allegiance to a progressive

agenda aimed at reducing inequality, strengthening the social safety net

and taking action on climate change. But there are some big differences

about how to achieve those goals.

And the starkest divide involves health care. Almost surely, the eventual platform will advocate “Medicare for TK.” But what word is eventually chosen to replace the placeholder “TK,”

and more important, what that means in terms of actual policy, will be

crucial both for the general election and for what comes after if

Democrats win.

On one side, there’s “Medicare for All,” which has

come to mean the Bernie Sanders position: replacing the entire existing

U.S. health insurance system with a Medicare-type program in which the

government pays most medical bills directly.

On the other side, there’s “Medicare for America,” originally a proposal from the Center for American Progress, now embodied in legislation.

While none of the announced Democratic candidates has endorsed this

proposal yet, it’s a good guess that most of them will come around to

something similar. [For an even deeper look at what’s on Paul Krugman’s mind, sign up for his weekly newsletter.]

The

big difference from a Sanders-type plan is that people would be allowed

to keep private coverage if they chose — but they or their employers

would also have the option of buying into an enhanced version of

Medicare, with substantial subsidies for lower- and middle-income

families.

The most important thing you need to know about these rival plans is that both of them would do the job.

Many

people realize, I think, that we’re the only advanced country that

doesn’t guarantee essential health care to its legal residents. My guess

is that fewer realize that nations achieve that goal in a variety of

ways — and they all work.

Every two years the Commonwealth Fund provides an invaluable survey

of major nations’ health care systems. America always comes in last; in

the latest edition, the three leaders are Britain, Australia and the

Netherlands.

What’s remarkable about those

top three is that they have radically different systems. Britain has

true socialized medicine — direct government provision of health care.

Australia has single-payer — it’s basically Bernie down under. But the

Dutch rely on private insurance companies

— heavily regulated, with lots of subsidies, but looking more like a

better-funded version of Obamacare than like Medicare for All. And the

Netherlands actually tops the Commonwealth Fund rankings.

So which

system should Democrats advocate? The answer, I’d argue, is the system

we’re most likely actually to create — the one that will play best in

the general election, and is then most likely to pass Congress if the

Democrat wins.

And there’s one big fact on the ground that any realistic health strategy has to deal with: 156 million Americans

— almost half the population — currently receive health insurance

through their employers. And most of these people are fairly satisfied

with their coverage.

A Medicare for All plan would in effect say

to these people, “We’re going to take away your current plan, but trust

us, the replacement will be better. And we’re going to impose a bunch of

new taxes to pay for all this, but trust us, it will be less than you

and your employer currently pay in premiums.”

The thing is, both

of these claims might well be true! A simple, single-payer system would

probably have lower overall costs than a hybrid system that preserves

some forms of private coverage.

But even if optimistic claims

about Medicare for All are true, will people believe them? And even if

most people do, if a significant minority of voters doesn’t trust the

promises of single-payer advocates, that could easily either doom

Democrats in the general election or at least make it impossible to get

their plan through Congress.

To me, then, Medicare for America —

which lets people keep employment-based insurance — looks like a much

better bet for actually getting universal coverage than Medicare for

All. But I could be wrong! And it’s fine to spend the next few months

arguing the issue.

What won’t be fine will

be if activists make a no-private-insurance position a litmus test,

declaring that anyone advocating a more incrementalist approach is no

true progressive, or maybe a corrupt shill for the medical/industrial

complex. As you might guess, my concerns aren’t drawn out of thin air;

they’re things I’m already hearing.

So Democrats should try to

make this a real debate, one about the best strategy for achieving a

shared goal. Can they manage that? I guess we’ll find out. https://www.nytimes.com/2019/03/21/opinion/medicare-for-all-democrats.html?smid=nytcore-ios-share

Opinion | Elissa Ely: Measuring medical care in 20-minute doses - The Boston Globe

by Elissa Ely - Boston Globe - April 12 2019

Consider 20 minutes: a middling amount of time,

not as ample as 47 minutes or as brief as 6, but an interval that seems

long enough to wave at someone over the fence post and maybe hang out a

bit.

Twenty minutes is also long enough to greet a patient in the

waiting room, walk them down the hall, take their weight, fill out

their group-home paperwork, check their refills, see if the Care Plan is

updated in the Electronic Medical Record, and send an e-mail to Central

Scheduling with a follow-up date. It’s probably enough time to inquire

about sleep, appetite, exercise, voices, and bowel function. “How’s your

mood these days?” 20 minutes asks — but when the answer comes, it

doesn’t have time to listen hard. Someone else is already waiting by the

fence post.

Twenty minutes is not long enough to find out what

the greatest worry in life is at the moment, or which TV show offers

respite (bless those Kardashians). It can’t stop to admire how someone

continues to cope with decades of illness — and, if her son happens to

be recovering from an overdose, it’s not long enough to learn the

details. A patient terrified of an upcoming medical procedure will have

to hold onto that thought.

Twenty minutes doesn’t stop for crisis, and even stopping for sorrow

can become a luxury. It’s good for productivity requirements, bad for

relationships.

With all this high efficiency, patients — who are in no position to

argue — may not feel eager to rush back for another 20 minutes.

Caretakers are in no position to argue either. We have this in common

(though naturally, there is not enough time to talk about it).

A number of months ago, a man came in. He was in the depressed phase

of a cycle, barely able to rise off the sofa. We discussed a medication

change, which took all our time. I asked if he would come back sooner

than usual.

“For what?” he said.

“Just to talk,” I said.

He looked surprised.

“Really?” he said. “I didn’t know psychiatrists did that.’’ Elissa Ely is a psychiatrist. https://www.bostonglobe.com/opinion/2019/04/12/measuring-medical-care-minute-doses/9QAhkd96XxRojj6do0MOGP/story.html?et_rid=1744895461&s_campaign=todayinopinion:newsletter

Patients express frustration over surprise medical bills - The Boston Globe

By Liz Kowalczyk - Boston Globe - April 13, 2019

Cheryle Reidel knows a thing or two about surprise medical bills.

There was the $6,000 for a cancer biopsy in 2012. Several years later,

an anesthesiologist and a nurse anesthetist billed her $2,600 for

another procedure.

This year, it happened again: Reidel underwent a

colonoscopy at Norwood Hospital — which is fully covered by her

insurance plan — only to discover that the anesthesiologist who worked

there was not. The bill: $2,490.

What happened after Reidel, 64, received these unexpected medical

charges illustrates one of the most frustrating and unpredictable

aspects of the health care system: It was only after dozens of phone

calls and numerous letters to insurance companies and the providers that

she got these bills

dismissed. Other patients have not been so lucky.

Reidel was one of more than 25 readers who wrote to the Globe after the newspaper published a story last month about out-of-network billing, expressing frustration with unexpected charges.

The 10 top local news stories from metro Boston and around New England delivered daily.

“The patient should not be on the hook for spending hours and hours

digging through paperwork, printing out documents, and contacting the

insurance company, contacting the anesthesiologists, contacting the

hospital,’’ Reidel said. “That’s ridiculous. I work a full-time job.’’

Chloe Nasser’s parents have been relentlessly fighting such bills.

Last summer, her doctor, who is affiliated with Brigham and Women’s

Hospital, ordered routine blood work — at a lab in the same office. She

was astonished to get a $701.89 bill a month later because the lab was

not in her insurance network.

The family is also contesting a much

larger out-of-network bill for a colonoscopy Nasser had at the Brigham,

said her mother, Kathleen Wynn.

Surprise out-of-network medical bills occur when a hospital uses

anesthesiologists, radiologists, ambulance companies, emergency medicine

doctors, or other providers that are not covered by a patient’s

insurance network. Often, providers do not inform patients in advance.

The practice is under growing scrutiny nationwide. A new analysis

shows these charges, also called balance billing, may be more common in

Massachusetts than previously believed.

A study by the nonprofit

Health Care Cost Institute found that 15 percent of 9,041 in-network

hospital admissions in Massachusetts in 2016 included an out-of-network

bill from a professional who worked there — the 11th-highest rate in the

country.

David Seltz, executive director of the Massachusetts

Health Policy Commission, a watchdog group, cautioned that the study

only examined medical claims from large national insurers.

Massachusetts-based insurers tend to have more providers in their

networks, so there is less chance for a patient to be hit with a

surprise medical bill.

Still, the new information “reinforces the

need and urgency for the [state] to take action to address this issue

and help protect patients,’’ Seltz said.

The Globe reported in

March that about 115 patients filed complaints about surprise medical

bills in 2017 and 2018 with Massachusetts Attorney General Maura

Healey’s office. Readers responded to the article quickly and

passionately.

One theme was clear: Patients usually just paid bills that ran in the

hundreds of dollars because they were either too busy or too sick to

fight over relatively small amounts; however, others with large balances

were relentless in challenging the charges. Many readers held hospitals

responsible for using out-of-network doctors.

The Globe reviewed bills to verify readers’ complaints.

A few examples: ■ Nancy Welsh took her diabetic daughter to

Emerson Hospital’s emergency department last July because she wasn’t

eating or drinking. Doctors started intravenous fluids and called

Armstrong Ambulance Service to transfer her to Boston Children’s

Hospital.

Several weeks later, the family received a bill for more

than $3,000. Armstrong, it turns out, was not covered by their Aetna

insurance plan. After eight phone calls, four e-mails, and a registered

letter, Aetna reimbursed Welsh in February.

“A lot of people would have given up,’’ she said. “The more they stalled, the angrier I got.’’

But

Welsh wondered why staff at the Concord hospital did not warn her in

advance. Emerson spokeswoman Leah Lesser said there are so many

different and ever-changing insurance companies and plans that it is

often not possible to determine a patient’s coverage in an emergency.

“We encourage patients, before they need care, to learn what is covered by their insurance plans,’’ Lesser said in a statement. ■ Jonathan Scott, 61, was diagnosed with

advanced cancer in 2016. Scott’s oncologist and surgeon at Beth Israel

Deaconess Medical Center were covered by his Tufts Health Plan network,

as was the hospital, he said. Another surgeon — apparently not covered —

was assigned to implant a tiny catheter above Scott’s heart through

which he would get chemotherapy.

Weeks later, he received a bill for $1,198.

“I

couldn’t eat or walk and I was having to deal with the insurance

company,’’ Scott said. Tufts eventually agreed to waive the charges, he

said.

Hospital spokeswoman Jennifer Kritz said she could not

comment on Scott’s case because of patient privacy rules but said

patients generally need prior approval from their insurance companies

for procedures.

Patients have been receiving these unexpected

bills for years. Doctors often blame insurers for the problem, saying

the large national companies don’t pay enough for them to join their

networks. Meanwhile, insurers argue that doctors prefer to remain

out-of-network because that allows them to charge inflated rates, rather

than accept a negotiated fee.

A number of states

have passed laws regulating out-of-network billing. After failing to

pass consumer projections last year, Massachusetts legislators plan to

reconsider similar measures this year.

Hospital officials often

say the problem is between insurers and doctors’ groups. State laws

typically include a way for the two sides to reach fair payment rates.

But Frederick Isasi,

executive director of the nonprofit Families USA, said hospitals share

the blame.

“They are selecting their providers,’’ said Isasi, who

recently testified before Congress on the issue. “They have a

responsibility to make sure they are in-network.’’

Reidel, a sales analyst for a medical supply company, agrees.

Her first two surprise bills involved care she received at Sturdy Memorial Hospital in Attleboro, which was in her insurance plan’s network, she said.

Amy

Pfeffer, Sturdy’s chief financial officer, said the hospital strongly

encourages all providers to join the same networks as the hospital but

does not require it. Mandating it, she said, might force doctors to

accept smaller payments from insurers that do not cover their costs.

“That would tie their hands,’’ she said.

After

receiving the $2,490 bill from Ether Anesthesia of Massachusetts

following her colonoscopy at Norwood Hospital last year, Reidel left a

message for the hospital’s chief executive. Reidel said two weeks later,

Norwood’s Chief Financial Officer Elizabeth Ganem told her the charges

were resolved.

When asked why Norwood Hospital allows

out-of-network anesthesiologists to work there, spokeswoman Lisa

Tarabelli said in an e-mail that the “hospital is in the process of

bringing the provider in-network.’’

Chloe Nasser’s family is

unsure whether they will succeed in their battle over large

out-of-network medical bills for medical care at Brigham and Women’s

Hospital.

Ethan Slavin, a spokesman for Aetna, her insurer at the

time, said many Aetna plans include the Brigham in their network. But

not Nasser’s particular plan; her Brigham doctor was covered, but the

hospital itself was not. And that is where her doctor sent some lab work

and where he sent her for a colonoscopy. Wynn, Nasser’s mother, said no

one mentioned this possibility.

The Brigham said it is improving

its educational materials for patients to better explain the medical

bills they might face. That information is expected to be ready in May. https://www.bostonglobe.com/metro/2019/04/13/patients-express-frustration-over-surprise-medical-bills/dKHCsHYVfF35QtKidoV75K/story.html?et_rid=1744895461&s_campaign=todaysheadlines:newsletter

Americans Are Delaying Health Care Until Tax Refunds Arrive

Out-of-pocket medical spending jumps once the money hits people’s bank accounts.

by John Tozzi - Bloomberg News - April 12, 2109

When Hayden Myer made an eye doctor’s appointment for the end of

April, he told the clinic that he might not show up for the visit if his

tax refund didn’t arrive in time.

The 27-year-old, who says his vision is bad enough that he

avoids driving at night, has been wearing a four-year-old pair of

glasses since he ran out of contact lenses last summer. He’s expecting

about $265 from his refund.

Myer and many other Americans rely on getting money back at

tax time to pay for important health needs. It’s a result of thin

household savings colliding with rising medical prices and high-deductible insurance plans that expose them to greater health expenses.

“I’ve

never been able to use my return for anything that is a leisure or a

pleasure,” said Myer, who earns about $40,000 a year running a

peer-support line for a mental-health nonprofit in Richmond, Virginia.

The

federal deadline for people to file income taxes is April 15.

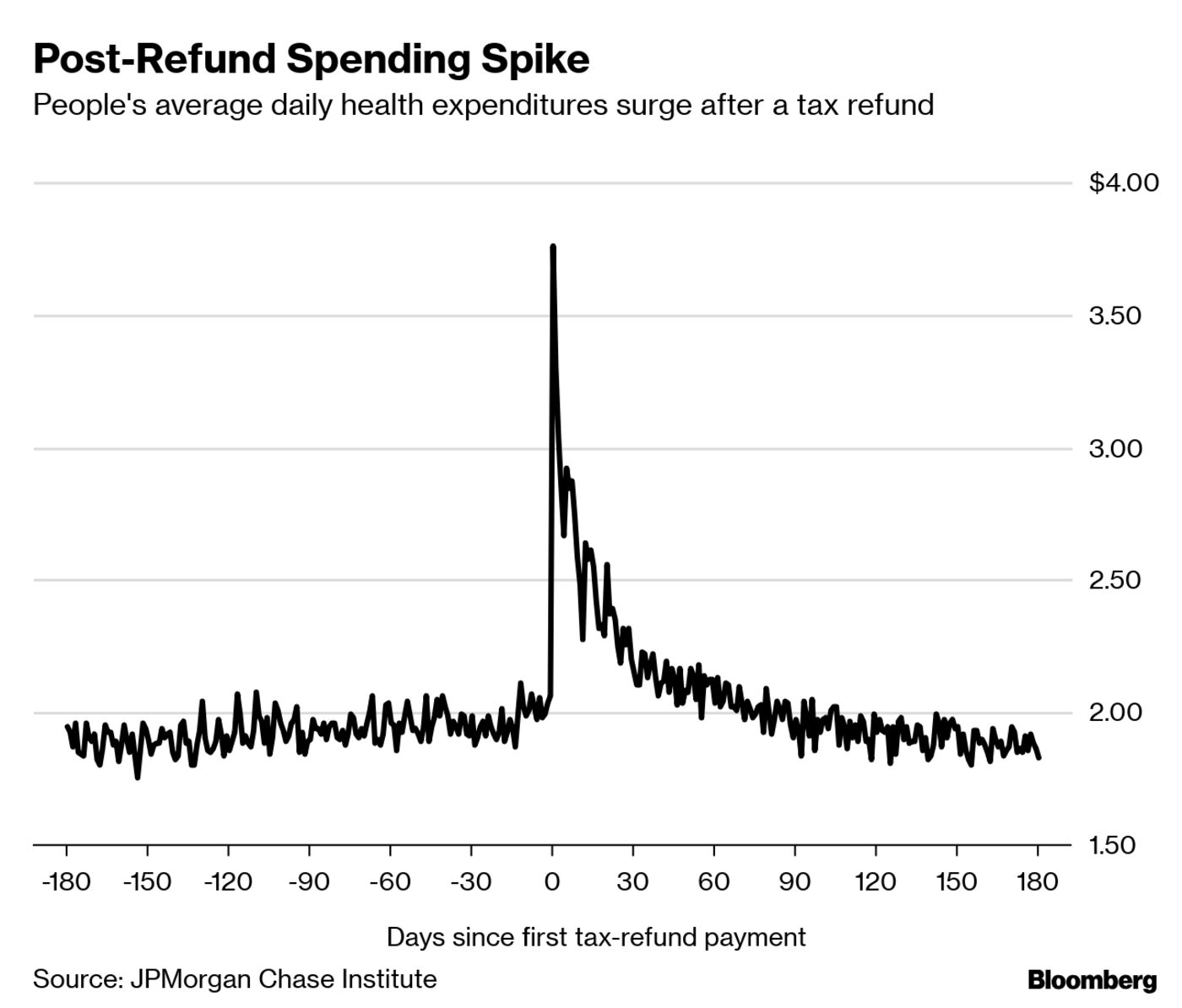

Out-of-pocket spending on health care jumps about 60 percent in the week

after people get their refunds, according to an analysis

of account data published last year by the JPMorgan Chase Institute, a

research group that draws on the bank’s data. The bulk of that money is

spent during face-to-face encounters at clinics, hospitals or other

medical providers.

That suggests people aren’t merely using refunds to pay down

old debts; they’re waiting until they have cash in hand to get treated.

“It

was surprising, and I’d go so far as to say alarming,” said Fiona

Greig, director of consumer research at the JPMorgan Chase Institute.

“Those are visits that would have taken place three weeks earlier, had

the tax refund arrived three weeks earlier.”

Refunds trigger about a 10 percent increase in the number of

people making in-person health-care payments on weekdays, according to

the group’s research. Other research from the institute has shown that

refunds are also frequently followed by increased cash withdrawals,

credit card payments and spending on durable goods.

Tax refunds — the difference between the money withheld from workers’ paychecks and the taxes they actually owe — are the biggest single payment many households receive all year. The average federal refund taxpayers received this spring was $2,873, according to IRS data on filings as of March 29.

More

than 1 in 3 working-age Americans skipped a doctors’ visit or medical

test, or didn’t fill a prescription, because of the cost last year,

according to a recent survey by the Commonwealth Fund, a nonprofit health-research foundation.

Myer,

who has insurance, has been forgoing weekly injections for low

testosterone, getting them only once a month or less. “That prescription

is also just sky-high,” he said, costing about $75 per visit until he

reaches his health plan’s deductible.

The medical costs add to a

pile of student loans, credit-card debt and payments on his Nissan

Rogue. He recently moved back in with his father after he couldn’t

afford a rent increase. He also owes money to a psychiatrist who charges

a sliding-scale fee. Getting a new prescription for his vision is

Myer’s priority, though.

Spring Surge

Dentists and

physicians’ offices accounted for the greatest share of in-person

health payments that followed tax refunds, the JPMorgan Chase

Institute’s report showed. Mark Vitale, a dentist in Edison, New Jersey,

said refunds always bring a surge of patients.

“Year after year, what patients will say to me is, ‘Let’s

just wait until April 1 or May 1 when I get my tax refund,’” he said.

Vitale has practiced for 35 years, and over time, he said, “the dollar

has gotten tighter.’’

Three people who booked significant dental

procedures like implants or crowns around the beginning of April cited

their tax refunds, he said. They’re typically employed, middle-class

people. Sometimes they’ve delayed dental work for years.

The research group analyzed data from millions of Chase bank

accounts, as well as credit and debit cards, looking for patterns in the

movements of money.

The granular picture of how cash flow affects

people’s ability to get medical care reveals problems that clinicians,

health plans, employers and financial companies ought to grapple with,

said Greig.

Doctors need to talk to patients about how to

prioritize care if they can’t pay for it. That conversation now happens

“in a very incomplete way” with finance staff, rather than clinicians,

she said. Employers and health plans should understand that trying to

lower spending by pushing more expenses onto households could backfire

if they delay care.

“Health problems don’t age well,” Greig said. https://www.bloomberg.com/news/articles/2019-04-12/what-to-spend-your-tax-refund-on-how-about-the-doctor

I have been reading your posts regularly which is specially for health, medicine and body care .I need to say that you are doing a fantastic work. Please keep it up the great work. leg pain

I would be grateful if you continue with the quality of what we are doing now with your blog.I really enjoyed it

ReplyDeletetravel and medical insurance

I have been reading your posts regularly which is specially for health, medicine and body care .I need to say that you are doing a fantastic work. Please keep it up the great work.

ReplyDeleteleg pain