I’ve just finished reading a new book that I think will be of great value to anybody interested in better understanding American health care policy, and why it’s so complex, dysfunctional and hard to change. It’s titled “Medicare For All: A Citizen’s Guide”, written by Abdul El-Sayed and Micah Johnson, and published by the Oxford University Press.

It’s scope and accessible style of writing make it a valuable resource for even a lay audience unfamiliar with the wonky policy jargon that often acts as a barrier to a clear understand of health policy in the US. It explores the history, policy and politics of American health care, and is very much up to date, even through the Covid-19 pandemic. It describes the barriers to reform of our broken health care system, and strategies (and the odds for success) for reform.

Highly recommended!

- SPC

How Trump Affected Americans’ Health

by Giovanni Rossonello - Lancet - February 11, 2021

Former President Donald Trump stands accused of inciting a riot that left at least five peopledead and more than 100 police officers injured.

But according to a new report from The Lancet, a respected medical journal, that’s just the tip of the iceberg when it comes to the harm that Trump did to public health during his time in office.

Released today, the 49-page report ticks off the health effects of Trump’s policies on everything from the environment to taxes to Covid-19. And the results aren’t pretty.

Soon after Trump took office in 2017, The Lancet established the Commission on Public Policy and Health in the Trump Era to study the health impact of his decisions in the White House. Over the past four years, the commission analyzed his policies as they took shape while seeking to place them in a broader historical context.

They found that Trump’s mismanagement of the coronavirus pandemic caused tens of thousands of deaths that might have been avoided if the country’s response had been more effectively coordinated.

“I think the huge number of deaths from Covid, compared to the other G7 wealthy nations, was striking,” said Steffie Woolhandler, a co-chairman of the committee and a distinguished professor at Hunter College in New York.

But even before the pandemic, the report found, Trump’s attempts to dismantle the Affordable Care Act had increased the number of uninsured Americans by two million to three million people.

His trillion-dollar tax cuts primarily benefited high-income Americans, while stripping the federal government of resources that it had used to pay for social-welfare programs.

“Even prior to the pandemic,” said Woolhandler, a physician, “the United States’ policies had so thoroughly failed to provide the conditions to protect health that 461,000 people who died in 2018 would have survived if our death rate were the same as other healthy nations.”

Yet she noted that many of the United States’ public health problems predated not only the pandemic, but also the Trump administration. In many cases, the authors wrote, the health decline under Trump was only a continuation of a broader trend — one that seems to have begun in the early 1980s.

“In 1980, life expectancy in the United States was the same as in all our developed nation counterparts — Germany, France, Japan,” said Kevin Grumbach, a member of the commission and a professor at the University of California, San Francisco. “Every year since 1980, the U.S. started falling farther and farther behind these other nations. So now we are three or four years behind the average life expectancy of these other nations.”

Grumbach, who is also a physician, said that over the same period, the cost of health care had risen far more quickly in the United States than in other nations — a trend that Trump contributed to. The report found that his administration increased the privatization of government health programs like Medicare, most likely leading to a rise in costs for consumers.

The report also concluded that by loosening scores of regulations, Trump caused environmental harm that led to the deaths of over 22,000 people in 2019 alone. That was significantly more than had died for similar reasons in 2016.

“That was very surprising, because it’s one area the United States has been improving on in recent decades,” Woolhandler said. “And Trump very quickly managed to reverse the progress.”

This report by the Lancet

Commission on Public Policy and Health in the Trump Era assesses the

repercussions of President Donald Trump's health-related policies and

examines the failures and social schisms that enabled his election.

Trump exploited low and middle-income white people's anger over their

deteriorating life prospects to mobilise racial animus and xenophobia

and enlist their support for policies that benefit high-income people

and corporations and threaten health. His signature legislative

achievement, a trillion-dollar tax cut for corporations and high-income

individuals, opened a budget hole that he used to justify cutting food

subsidies and health care. His appeals to racism, nativism, and

religious bigotry have emboldened white nationalists and vigilantes, and

encouraged police violence and, at the end of his term in office,

insurrection. He chose judges for US courts who are dismissive of

affirmative action and reproductive, labour, civil, and voting rights;

ordered the mass detention of immigrants in hazardous conditions; and

promulgated regulations that reduce access to abortion and contraception

in the USA and globally. Although his effort to repeal the Affordable

Care Act failed, he weakened its coverage and increased the number of

uninsured people by 2·3 million, even before the mass dislocation of the

COVID-19 pandemic, and has accelerated the privatisation of government

health programmes. Trump's hostility to environmental regulations has

already worsened pollution—resulting in more than 22 000 extra deaths in

2019 alone—hastened global warming, and despoiled national monuments

and lands sacred to Native people. Disdain for science and cuts to

global health programmes and public health agencies have impeded the

response to the COVID-19 pandemic, causing tens of thousands of

unnecessary deaths, and imperil advances against HIV and other diseases.

And Trump's bellicose trade, defence, and foreign policies have led to

economic disruption and threaten an upswing in armed conflict.

Although

Trump's actions were singularly damaging, many of them represent an

aggressive acceleration of neoliberal policies that date back 40 years.

These policies reversed New Deal and civil rights-era advances in

economic and racial equality. Subsequently, inequality widened, with

many people in the USA being denied the benefits of economic growth. US

life expectancy, which was similar to other high-income nations' in

1980, trailed the G7 average by 3·4 years in 2018 (equivalent to 461 000

excess US deaths in that year alone). The so-called war on drugs

initiated by President Richard Nixon widened racial inequities and led

to the mass incarceration of Black, Latinx, and Indigenous people.

Overdose deaths soared, spurred by drug firms' profit-driven promotion

of opioids and the spread of despair in long-afflicted communities of

colour and among working-class white people. Market-oriented health

policies shifted medical resources toward high-income people, burdened

the middle class with unaffordable out-of-pocket costs and deployed

public money to stimulate the corporate takeover of vital health

resources.

The Commission applauds President Joe

Biden and Vice President Kamala Harris for rejoining WHO and the Paris

Climate Agreement, and for other steps they have taken to rescind some

of President Trump's health-harming executive actions. But the new

administration and Congress must go beyond simply repairing Trump's

damage. They must initiate thoroughgoing reforms to reverse widening

economic inequality and the neoliberal policy drift that pre-dated

Trump, and redress long-standing racism—root problems that harm health

and have fomented threats to US democracy. Additionally, forceful action

is needed to forestall environmental disaster and strengthen public

health infrastructure.

Reducing

economic inequality will require raising taxes on the wealthy and using

the proceeds to strengthen social, education, nutrition, and health

programmes. Those programmes should avoid segregating the poor, and

instead encompass all people in the USA to bolster the solidarity that

is key to securing broad and continuing popular support. Government

should stop funnelling expenditures through private firms whose

profit-seeking boosts costs and distorts priorities. Hence, a single

payer health-care reform offers the fairest, most effective, and most

efficient route to universal health coverage.

Censure

of Trump's virulent brand of racism is imperative but insufficient. US

leaders must embrace emphatically anti-racist politics and programmes to

dismantle the centuries-old structures that reproduce racial inequity

in health and all other spheres. Ending mass incarceration and reforming

the execrable policing and criminal justice systems that oppress

communities of colour and fill prisons are essential for racial justice.

Additional steps must include vigorous enforcement of voting and civil

rights; large new investments in educational equity, the Indian Health

Service, and minority-serving health and educational institutions; and

compensation for wealth denied to and confiscated from communities of

colour in the past.

Finally, the

president and the Congress must mobilise massive resources to avert

climate catastrophe, address the calamities caused by COVID-19, and

attenuate global inequality. The 3·4% of GDP the USA currently spends on

troops and armaments should be reduced to the 1·4% average of other G-7

nations, with the savings redeployed to address urgent health, social,

and environmental problems at home; reinvigorate the scientific efforts

that are vital to global progress; and fund the four-times increase in

foreign aid needed to reach the level recommended by the UN.

Key messages

During his time in office President Trump:

•

Politicised and repudiated science, leaving the USA unprepared and exposed to the COVID-19 pandemic

•

Eviscerated environmental regulation, hastening global warming

•

Incited racial, nativist, and religious hatred, provoking vigilante and police violence

•

Denied refuge to migrants fleeing violence and oppression, and abused immigrant detainees

•

Undermined health coverage

•

Weakened food assistance programmes

•

Curtailed reproductive rights

•

Undermined global cooperation for health, and triggered trade wars

•

Shifted resources from social programmes to military spending and tax windfalls for corporations and the wealthy

•

Subverted democracy both nationally and internationally

Although

the Trump administration policies posed a uniquely urgent threat to

health, damaging neoliberal policies predated and abetted his

ascendance:

•

Life expectancy in the USA has lagged behind other wealthy nations since 1980 and began falling in 2014

•

The

chronically high mortality of Native Americans started rising in 1999,

while yawning disparities between Black and white people persisted and

progress on racial equity in other domains (eg, education, housing,

income and policing) halted or reversed

•

Substance abuse deaths greatly increased

•

Income and wealth inequality widened

•

Incarceration

increased four-fold, initiated by President Nixon's racially motivated

war on drugs and compounded by harsh laws enacted under Presidents

Reagan and Clinton

•

Welfare eligibility restrictions implemented by President Clinton removed benefits from millions

•

Deindustrialisation

spurred by trade agreements that favoured corporate interests over

labour protections reduced economic opportunity in many regions of the

USA, damaging health and increasing receptivity to racist and xenophobic

appeals

•

Market-based

reforms commercialised and bureaucratised medical care, raised costs,

and shifted care toward high-income US residents

•

Despite

the Affordable Care Act, nearly 30 million people in the USA remained

uninsured and many more were covered but still unable to afford care

•

Funding cuts reduced the front-line public health workforce by 20%

The

Biden administration must cancel Trump's actions and also address the

health-damaging structural problems that were present before Trump's

presidency:

•

Raise

taxes on high-income people and use the proceeds to bolster social,

educational, and health programmes, and address urgent environmental

problems

•

Mobilise against the structural racism and police violence that shorten the lives of people of colour

•

Replace

means-tested programmes such as Medicaid that segregate low-income

people, with unified programmes such as national health insurance that

serve all US residents, aligning the interests of the middle class and

the poor in maintaining excellence

•

Reclaim

the US Government's role in delivering health and social services, and

stop channelling public funds through private firms whose profit-seeking

skews priorities

•

Redirect

public investments from militarism, corporate subsidies, and distorted

medical priorities to domestic and global fairness, environmental

protection, and neglected public health and social interventions

•

Reinvigorate

US democracy by reforming campaign financing, reinforcing voting,

immigration, and labour rights, and restoring oversight of presidential

prerogatives

COVID-19's

facile breach of national boundaries is a reminder of the vulnerability

of even the most powerful nations in an interconnected world, and the

folly of contempt for science, facts, and equity. In years past, the USA

deployed its economic power and scientific prowess in important,

although imperfect, efforts to advance global health. It must rejoin the

global community in a spirit of collaboration, rejecting the notion

that others must fail in order for the USA to succeed.

Congressional Budget Office Scores Medicare-For-All: Universal Coverage For Less Spending

by Adam Gaffney, David Himmelstein and Steffie Woolhandler - Health Affairs Blog - February 16, 2021

For the first time in a quarter century, the Congressional Budget Office (CBO) has undertaken an economic analysis

of single-payer health care reform, also known as Medicare for All. The

more than 200-page working paper, released last month, includes a rich

explanation of methodology together with cost projections for 2030 and

will no doubt serve as an important reference for years to come.

The report makes many sound assumptions but also some questionable

ones that are overly pessimistic. Yet, overall, its bottom-line

estimates should reassure those concerned about the economic feasibility

of single payer: The CBO projects that such reform would achieve

universal coverage, bolster provider revenues for clinical services, and

eliminate almost all copayments and deductibles—even as overall health

care spending fell.

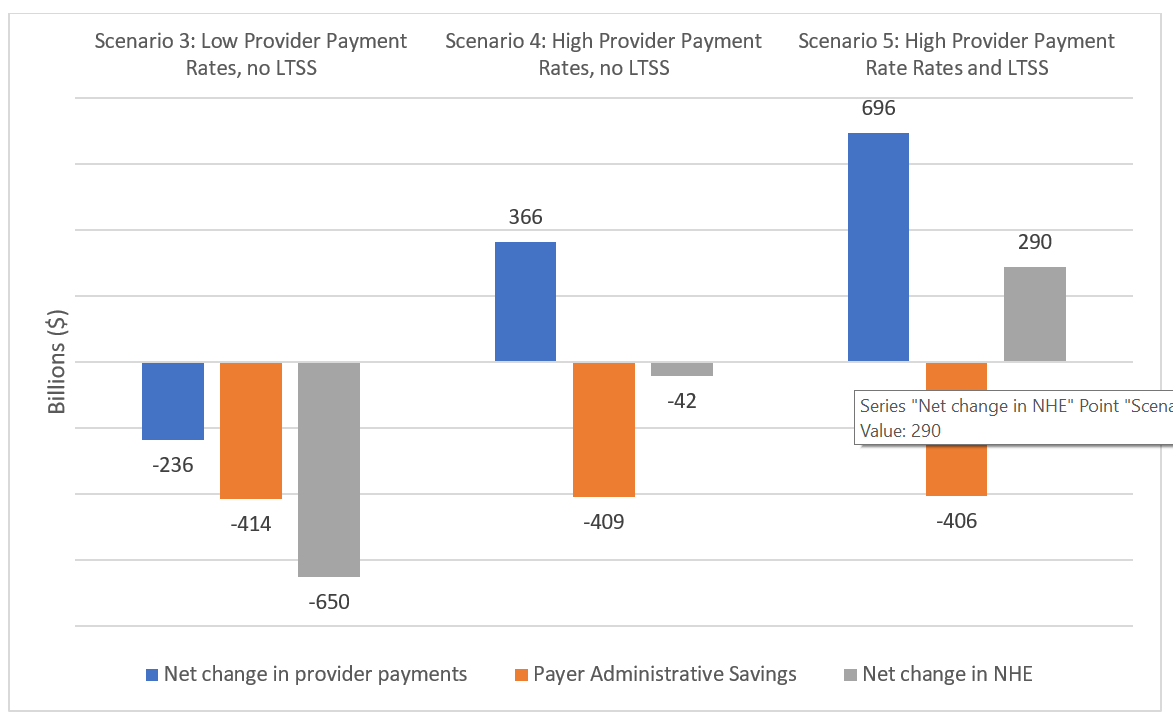

The CBO models costs under five different variants of single payer.

The first four envision universal coverage of all services other than

long-term care, while the fifth incorporates a large expansion of

long-term services and supports (LTSS) for people with disabilities of

all ages. The scenarios vary by patient cost sharing and provider

payment level. Low cost-sharing has no copays or deductibles for medical

services and minimal cost sharing for prescription drugs; under high

cost-sharing, patients with incomes above 150 percent of poverty would

bear about 7.5 percent of costs out of pocket. Low payment rates to

providers would set rates slightly higher than Medicare’s; high rates

would be equivalent to the current average of the rates paid by private

insurers and government programs. The five variants (or scenarios) are

summarized in exhibit 1.

Exhibit 1: Congressional Budget Office’s five single-payer scenarios

We discuss below the CBO’s estimates of single payer’s overall

effects on national health spending, the implications of the estimates

for providers, and the concerns the analysts raise about worsened

“provider congestion” under a single-payer health care system.

Throughout, we point out instances where the CBO’s assumptions differ

from previous, widely publicized analyses, or from provisions included

in the Medicare for All legislation currently in Congress.

CBO’s Estimates Of Single Payer’s Effects On National Health Expenditures

The CBO projects that variants 1–4 of single-payer reform would

reduce national health expenditures (NHE) despite substantial increases

in the use of care triggered by expanded and upgraded coverage. If a

vast new program covering LTSS for all US residents were included

(scenario 5), the CBO estimates that NHE would rise by 4.4 percent above

currently projected spending levels. Exhibit 2 summarizes the CBO’s

spending estimates for the three low cost-sharing scenarios, which are

similar to the Medicare for All bills in Congress.

Exhibit 2: Congressional Budget Office estimates of effect of single

payer on health spending in 2030: low cost-sharing scenarios

How can the use of care rise even as spending falls? Mostly,

according to the CBO, through greater administrative simplicity. As the

CBO notes, traditional Medicare’s administrative overhead accounts for

approximately 2 percent of its total revenue, compared to the 12 percent

overhead of private insurers. Under single payer, the CBO projects,

administrative spending would fall accordingly; overall overhead for the

Medicare for All system is estimated by the CBO at below 2 percent. As

shown in exhibit 2, this translates into around $400 billion annually

(more than $1,000 per capita) in savings under all of the single-payer

variants.

Of note, these evidence-based projections clash with the analyses by the Urban Institute and the RAND Corporation,

which perplexingly assumed much higher administrative overhead under a

single-payer system than under the current traditional Medicare program

or under universal systems abroad.

Implications For Provider Overhead And Revenue

The CBO appropriately projects substantial administrative savings for providers, again unlike many previous analyses. US hospitals and physicians

waste money and time contending with multiple payers, each with its own

complex and varying coverage rules and payment procedures, formularies,

and so forth. The CBO projects that the share of revenues that

hospitals spend on administration would fall from 19 percent at present

to 12 percent under single payer; that physicians’ administrative

overhead would fall from 15 percent to 9 percent; and that the

administrative expenses of other medical providers (for example,

dentists, home health agencies, and hospices) would fall from 9 percent

to 6 percent. In addition, it estimates that physicians and nurses would

spend less time on administrative activities, freeing up 4.8 percent of

physicians’ work hours and 18.4 percent of nurses’ work time. These

assumptions build on a large evidence base showing high administrative overhead among US health care providers relative to other nations.

The CBO assumes that single payer would allow providers to keep these

savings on administration and billing, and use the resources freed up

to provide more care. Hence, providers’ administrative savings do not

appear as savings in exhibit 2. In effect, the CBO interprets these

efficiencies as reductions in providers’ costs that would enable them to

deliver a greater quantity of services for a given amount of revenue.

Consequently, the “net change in provider payments” shown in exhibit 2

doesn’t fully account for the extra resources made available to

hospitals, doctors, and other providers under Medicare for All. In

contrast, exhibits 3 and 4 present our estimates of single payer’s

financial impacts on physicians and hospitals, incorporating CBO

projections of providers’ savings on administrative spending and

physicians’ and nurses’ time.

As exhibit 3 demonstrates, payments to clinicians would rise in all

five scenarios according to CBO estimates. We estimate this translates

into an additional $39,816–$157,412 in revenue per practicing physician.

At the same time, physicians’ practice overhead would shrink under

single payer, increasing practices’ take-home income. Such a windfall,

in our view, may be excessive, at least for some providers. (Disclosure:

The authors are all physicians).

Source: Authors’ analysis of the Congressional Budget Office’s (CBO’s) Single-Payer Health Care Systems Team. How

CBO analyzes the costs of proposals for single-payer health care

systems that are based on Medicare’s fee-for-service program.

Washington (DC): CBO; 2020 Dec. Note: *Based on Association of American

Medical Costs estimate of 840,000 practicing physicians in 2030 and the

assumption that physician payments account for 77.78 percent of payments

in the “Physician and other Clinical Service” category, as they did in

2018 according to the National Health Expenditure Accounts.

For hospitals, the CBO estimates that gross revenue would fall by

$187 billion under the “low pay” scenario but rise by $144 billion under

the high-payment scenario. Again, these figures do not give the full

picture of the impact on hospitals’ bottom lines, given the CBO’s

projections that single-payer reform would shrink hospitals’ spending on

administration and would also free up substantial amounts of nursing

time that is currently devoted to payment-related tasks. The CBO’s

estimates suggest that hospitals would save $143 billion to $166 billion

on administration and an additional $59 billion on freed-up nursing

time, resources that could be redirected to clinical care (exhibit 4).

Overall, building on the CBO’s projections, we estimate that hospitals’

clinical funding would change little (rising by $15 billion) under the

low-payment scenario or increase substantially, by $369 billion, under

the higher-payment one.

Exhibit 4: Modeling Congressional Budget Office’s low cost-sharing

scenario: ramifications for hospitals’ revenues and clinical operating

budgets

Source: Authors’ analysis of the Congressional Budget Office’s (CBO’s) Single-Payer Health Care Systems Team. How

CBO analyzes the costs of proposals for single-payer health care

systems that are based on Medicare’s fee-for-service program.

Washington (DC): CBO: 2020 Dec. Notes: **Based on the CBO estimate that

hospitals’ spending on administration (excluding registered nurse

(RN)and licensed practical nurse (LPN) time spent on administration)

would be reduced from 19 percent to 12 percent of hospital revenues.

***Based on (1) Bureau of Labor Statistics estimate of number of RNs and

LPNs employed in hospitals and average RN and LPN wages in 2019; (2)

the assumption that benefit costs equal 20 percent of wages; (3) the

assumption that nursing costs would rise at the same rate as overall

hospital costs; and (4) CBO’s estimate that RNs and LPNs devote 23

percent of time to administration and that single payer would reduce

that time by 80 percent.

The large increase in hospital funding that the CBO projects under

the high-payment scenario would, in our view, give an appropriate boost

to many struggling rural and safety-net hospitals but would be excessive

for hospitals that are currently realizing large annual profits.

Additionally, the fee-for-service hospital financing modeled by the

CBO differs from what is envisioned in the Medicare for All bill in the

House of Representatives. The House bill proposes paying hospitals,

nursing homes, and other institutional providers using “global budgets,”

that is, lump sums to cover all of their operating activities. This is

the model used by Canada and the US Veterans Health Administration.

Global budgeting could allow even greater reductions

in administrative spending by eliminating the need for per-patient

billing altogether. It would also allow payments to match current

operating budgets and facilitate the gradual redistribution of funding

among hospitals, directing more resources to communities most in need.

The global budgeting approach, however, would require separate

financing of capital expenditures (as in Canada and some European

nations), which again is an approach explicitly included in Medicare for

All bills in Congress but not in the CBO report. Such regulated capital

financing, in turn, could help regulate cost growth in the longer term

by avoiding investments in duplicative but profitable high-tech

facilities that encourage the delivery of low- or no-value care.

Hence, the CBO’s decision to model a system that used fee-for-service

payments for hospitals and other institutional providers rather than

global budgets with separate capital financing leads it to underestimate

single-payer savings in the short term and to ignore potential

longer-term savings and improvements in the distribution of hospital

infrastructure. That caveat aside, an important takeaway from the CBO’s

analysis is that, overall, providers would see stable or even increased

funding for patient care under single payer, even while overall health

spending fell.

Provider Congestion?

While the CBO report foresees greatly improved financial access to

care under single payer, it raises the specter of “provider congestion,”

that is, greater difficulty making appointments or rising waiting times

under single payer. Because such reform would newly cover the uninsured

and improve coverage for most other people, the CBO projects large

increases in the demand for care, and hence use. However, it projects

that not all of the demand could be met because of supply constraints,

for example, the finite number of doctors, nurses, and hospital beds.

Consequently, the report predicts increased “provider congestion” that

would cause some foregone care.

This prediction, however, is out of touch with clinical reality, an issue we recently explored in Health Affairs.

The CBO’s approach to supply constraints is only half right. There is

little question that, as the CBO assumes, a finite supply of health care

providers constrain utilization increases after coverage expansions: As

we have demonstrated,

in nation after nation, universal coverage expansions have led to

modest, or even no, societywide increases in use. Increased use by the

newly covered has usually been partially or fully offset by small

reductions in use among the well-covered or well-off.

Yet, these small reductions appear to be mostly due to the reduced provision of low-value care. Two econometricstudies

found that offsets after coverage expansion reflect reductions in the

amount of wasteful care provided to the already insured. Similarly, studies

by the Dartmouth Group indicate that the volume of elective and

low-value care increases when the supply of doctors and hospital beds

rise—a phenomenon called supplier-induced demand. In other words, faced

with an increase in demand for care, providers prioritize their time and

services, delivering more high-value care while reducing the provision

of low- or no-value services.

Characterizing such offsets as “unmet demand” or “congestion” is

hence misleading. It mirrors previous forecasts of “patient pileups”

when Medicare was first implemented—forecasts that proved incorrect. In

the US today, nearly one-third

of all health care delivered is unnecessary or wasteful. Overprovision

is common. If coverage expansion leads to some attenuation in

supplier-induced demand, all the better.

A Notable Omission

Finally, while the CBO projects reductions in health spending in four

out of five single-payer scenarios, as noted, it projects substantial

increases in federal spending that would replace all private insurance

premiums and nearly all out-of-pocket health care costs. Yet, there are

also substantial savings for state and local governments with

single-payer reform. The CBO’s brief mention of the savings likely to

accrue to these governments (and their taxpayers) omits probable savings

from no longer having to bear the costs of public employees’ health

insurance (projected to total $318 billion in 2030), as well as about

$162 billion in savings on other health programs. These, together with

savings on Medicaid (which the CBO does remark on), would bring state

and local governments’ total savings from single payer to about $800

billion in 2030 alone, reductions that provide important context for the

CBO’s estimates of increased federal government expenditures.

The Economics Of Single-Payer Financing: CBO’s Bottom Line

Overall, the CBO report provides one of the most detailed

explorations to date of the economics of single-payer financing. As we

have noted, it makes many sound assumptions, particularly about payer-

and provider-side administrative savings. At the same time, it adopts

some unfavorable assumptions about the structure of single-payer reform

(including some that conflict with key provisions of the Medicare for

All bills in Congress), projects excessive windfalls for some providers,

and asserts clinically nescient portrayals of “unmet demand.”

Nonetheless, the bottom line of the CBO analysis—that universal coverage

can be affordably achieved even as benefits are expanded and cost

sharing all but eliminated—should reinvigorate debate over such reform.

by Austin Frakt and Tynan Friend - The Incidental Economist - February 10, 2021

The complexity

of Medicare Advantage (MA) physician networks has been well-documented,

but the payment regulations that underlie these plans remain opaque,

even to experts. If an MA plan enrollee sees an out-of-network doctor,

how much should she expect to pay?

The answer, like much of the

American healthcare system, is complicated. We’ve consulted experts and

scoured nearly inscrutable government documents to try to find it. In

this post we try to explain what we’ve learned in a much more accessible

way.

Medicare Advantage Basics

Medicare Advantage is the private insurance alternative to traditional Medicare (TM), comprised largely of HMO and PPO options. One-third

of the 60+ million Americans covered by Medicare are enrolled in MA

plans. These plans, subsidized by the government, are governed by

Medicare rules, but, within certain limits, are able to set their own

premiums, deductibles, and service payment schedules each year.

Critically,

they also determine their own network extent, choosing which physicians

are in- or out-of-network. Apart from cost sharing or deductibles, the

cost of care from providers that are in-network is covered by the plan.

However, if an enrollee seeks care from a provider who is outside of

their plan’s network, what the cost is and who bears it is much more

complex.

Provider Types

To understand the MA (and enrollee) payment-to-provider pipeline, we first need to understand the types of providers that exist within the Medicare system.

Participating providers,

which constitute about 97% of all physicians in the U.S., accept

Medicare Fee-For-Service (FFS) rates for full payment of their services.

These are the rates paid by TM. These doctors are subject to the fee

schedules and regulations established by Medicare and MA plans.

Non-participating providers

(about 2% of practicing physicians) can accept FFS Medicare rates for

full payment if they wish (a.k.a., “take assignment”), but they

generally don’t do so. When they don’t take assignment on a particular

case, these providers are not limited to charging FFS rates.

Opt-out providers

don’t accept Medicare FFS payment under any circumstances. These

providers, constituting only 1% of practicing physicians, can set their

own charges for services and require payment directly from the patient.

(Many psychiatrists fall into this category: they make up 42% of all

opt-out providers. This is particularly concerning in light of studies suggesting increased rates of anxiety and depression among adults as a result of the COVID-19 pandemic).

How Out-of-Network Doctors are Paid

So,

if an MA beneficiary goes to see an out-of-network doctor, by whom does

the doctor get paid and how much? At the most basic level, when a Medicare Advantage HMO member

willingly seeks care from an out-of-network provider, the member

assumes full liability for payment. That is, neither the HMO plan nor TM

will pay for services when an MA member goes out-of-network.

The price that the provider can charge for these services, though, varies,

and must be disclosed to the patient before any services are

administered. If the provider is participating with Medicare (in the

sense defined above), they charge the patient no more than the standard

Medicare FFS rate for their services. Non-participating providers that

do not take assignment on the claim are limited to charging the

beneficiary 115% of the Medicare FFS amount, the “limiting charge.” (Some states

further restrict this. In New York State, for instance, the maximum is

105% of Medicare FFS payment.) In these cases, the provider charges the

patient directly, and they are responsible for the entire amount (See Figure 1.)

Alternatively, if the provider has opted-out of Medicare,

there are no limits to what they can charge for their services. The

provider and patient enter into a private contract; the patient agrees

to pay the full amount, out of pocket, for all services.

Figure 1: MA HMO Out-of-Network Payments

MA PPO plans operate slightly differently. By nature of the PPO plan,

there are built-in benefits covering visits to out-of-network

physicians (usually at the expense of higher annual deductibles and

co-insurance compared to HMO plans). Like with HMO enrollees, an

out-of-network Medicare-participating physician will charge the PPO

enrollee no more than the standard FFS rate for their services. The PPO

plan will then reimburse the enrollee 100% of this rate, less

coinsurance. (See Figure 2.)

In contrast, a

non-participating physician that does not take assignment is limited to

charging a PPO enrollee 115% of the Medicare FFS amount, which can be

further limited by state regulations. In this case, the PPO enrollee is

also reimbursed by their plan up to 100% (less coinsurance) of the FFS

amount for their visit. Again, opt-out physicians are exempt from these

regulations and must enter private contracts with patients.

Figure 2: MA PPO Out-of-Network Payments

Some Caveats

There are two major caveats to these payment schemes (with many more nuanced and less-frequent exceptions detailed here). First, if a beneficiary seeks urgent or emergent care (as defined by Medicare)

and the provider happens to be out-of-network for the MA plan

(regardless of HMO/PPO status), the plan must cover the services at

their established in-network emergency services rates.

The second

caveat is in regard to the declared public health emergency due to

COVID-19 (set to expire in April 2021, but likely to be extended). MA

plans are currently required

to cover all out-of-network services from providers that contract with

Medicare (i.e., all but opt-out providers) and charge beneficiaries no

more than the plan-established in-network rates for these services. This

is being mandated by CMS to compensate for practice closures and other

difficulties of finding in-network care as a result of the pandemic.

Conclusion

Outside

of the pandemic and emergency situations, knowing how much you’ll need

to pay for out-of-network services as a MA enrollee depends on a

multitude of factors. Though the vast majority of American physicians

contract with Medicare, the intersection of insurer-engineered physician

networks and the complex MA payment system could lead to significant

unexpected costs to the patient.

'I don't make enough': the financial cost of having Covid in the US

by Amanda Golpuch - The Guardian - February 12, 2021

Covid-19 allowed for an experiment in US healthcare: what if doctor’s visits and hospitalizations didn’t cost people money?

In

response to the pandemic, major health insurers volunteered to cover

coronavirus testing and treatment for their paying customers and the

government introduced programs to make care more affordable. But a year

after coronavirus was first identified in the US, those assurances

haven’t played out as planned.

A program to help the country’s 28.9 million uninsured has been riddled with problems,

such as patients not knowing which healthcare providers are actually

participating in the scheme. Undocumented immigrants have largely been

excluded from aid. The complexities of long Covid, when people

experience symptoms for months, have challenged patients and providers.

And health insurers still control what gets covered and for how long.

To better understand these disparities, the Guardian spoke to six people about the financial cost of Covid-19.

Mellisa Arredondo Moncibaiz, 51, Texas: $633.32

Out-of-pocket costs: $572.32;. Premium: $61 (for one month)

Mellisa

Arredondo Moncibaiz’s financial stress is tangled up with grief. Six of

her friends and relatives have died from Covid-19 – four of them in

January. “It’s just horrible all around,” she said.

The Wichita

Falls, Texas, resident had Covid at the end of October and spent five

days in the hospital, resulting in a $42,096 bill. The hospital billed

for more than 200 different items – from an $11 zinc capsule to $1,080

for each day of heart monitoring.

She is grateful her health

insurance will pay most of the $42,096 bill, but she still has many

sleepless nights thinking about her debts. The $572.32 she owes for her

coronavirus treatment is on top of the $3,689.81 she owes the hospital

because she broke her tailbone in June.

“After insurance, it’s

still $4,200, I don’t make enough to pay that,” said Moncibaiz, who

works in housing. “I just pay what I can, $20 there, $10 there. But now,

I haven’t been able to pay that because I am worried about rent,

utilities.”

To have health insurance, Moncibaiz pays a $61 premium each month – only a few insurers included premium relief in their Covid assistance.

Her deductible, what people must pay before the insurance kicks in, is

$2,550. After hitting that, insurance covers 80% of her medical costs.

Moncibaiz

said the debt is causing anxiety and depression, which she hasn’t

sought treatment for because of its price tag. She called the $600

stimulus checks the government sent in January “a kick in the teeth”.

The things which have helped the most, she said, are her understanding

landlord and the national pause on federal student loan payments.

“I am just working to keep my head above water,” she said.

Baldhead Phillips, 51, Georgia: $100,000

Uninsured

Atlanta-based

comedian Baldhead Phillips was hospitalized with Covid-19 for two weeks

in March, and each day watched as other patients were wheeled away on

gurneys after succumbing to the illness.

Doctors sent him home

with an order to use $200-a-month oxygen therapy, prescriptions for 11

drugs and new diagnoses of high blood pressure and heart failure.

“I

got home, got the exhaustion, got into bed and the first and last

thought in my mind was I just spent a lot of money to buy this stuff,

and this is not a cure, it’s just to let me live a little longer and see

how it’s going to go,” Phillips, 51, said.

Two days later,

Phillips received a $15,000 bill from the hospital. More bills followed

and Phillips said they have so far totaled more than $100,000.

Phillips doesn’t have insurance and is on the hook for the entire bill.

He has been able to cover some of the costs with help from a GoFundMe online fundraiser and other contributions from fans and friends, but his income is a fraction of what it used to be.

He

hasn’t been able to work as a standup because of coronavirus

restrictions and has stopped his second job as an Uber driver. “I’m so

stressed out about that but at the same time my family is saying, don’t

worry about bills, worry about getting better,” Phillips said.

Last

spring, Phillips was skeptical about the seriousness of Covid. Now, he

uses his public platform to warn about how grave it can be. Phillips

said: “I crack jokes for a living, but this is no joke at all.”

The

government’s nationalized health insurance program for seniors,

Medicare, has kept money at the back of Ellen’s mind while she struggles

with long Covid.

She pays $150 for the coverage each month and has spent less than $100

since she contracted Covid in April on prescription drugs.

But

Ellen, who asked not to use her last name for privacy, has had Covid

symptoms for 10 months – including 128 days of nonstop headaches.

“I

still have fatigue, right now I am laying down in bed, a shower will

wipe me out,” she said from her home in Littleton, Colorado. “I still

have brain fog, after we have this talk, I will be exhausted.”

The

66-year-old has seen a battery of specialists to address the lingering

symptoms, and with Medicare, a government health plan for people 65 and

older, the appointments are covered.

Like most Medicare

beneficiaries, Ellen has supplemental coverage which reduces costs of

things like prescription drugs – she estimates she has spent under $100

on those since April. “It’s fantastic,” she said.

Costs are higher

for the 6 million Medicare beneficiaries who don’t have supplementary

coverage to cover prescriptions, co-pays for doctors’ visits and other

medical care.

Adina

Gerver’s March Covid infection has left her with lingering symptoms

including debilitating fatigue, a nerve system condition and a blood

clot in her right lung.

“I am earning very little right now,

because I am working very little, because I am tired all the time,” said

Gerver, who said she’s relying on financial help from family.

The

41-year-old is being treated by specialists at the Mount Sinai Post

Covid Care Center in New York City. She owes $279.87 of the center’s

$3,900 bill for some of the treatments and tests she had in the autumn

and she has yet to receive bills for all the care she’s received.

Gerver

has Cobra, a government program which allows people to continue with

the insurance they had at their previous employer. Since August, she has

paid $1,000 a month in premiums. Before that, her premiums were about

$800. Separately, once she hits her $3,250 deductible, her plan pays for

100% of her medical expenses.

Then there were the other costs,

such as $20 for a pulse oximeter and spending more on ride-shares to get

around the city. Friends and family also bought her a shower chair, bed

desk and support pillow, which together are at least $100.

Gerver

suspects a government marketplace health insurance plan would cost less

than Cobra, but she doesn’t know if the care she needs for long Covid

would be covered.

The process of navigating health coverage in the

US can be frustrating and time-consuming at the best of times – when

coupled with severe fatigue, it was too much. “I could not get it

together to call them,” Gerver said.

She was also too tired to

fight a recent mystery bill - a month’s supply of the blood thinner she

paid $35 for on 31 December, cost her $491.98 in January.

Yaquelin Valencia, 29, California: $2,000

Out-of-pocket costs: $2,000. Premium: $0 (for one month)

When

Yaquelin Valencia had Covid in July, her biggest worry was how to

continue supporting her undocumented family members, especially as the

main provider for her parents.

“I was concerned a little about my

health, but I was more worried about my parents because I am their sole

provider,” said Valencia, who lives in California’s Bay Area.

The

29-year-old is a recipient of Daca, the temporary protection from

deportation for people who were brought to the US as children without

legal papers. Daca allowed her to collect unemployment when she was laid

off in April and get health insurance when she got a new job in June as

a community organizer in La Red, an immigrant rights campaign by the

advocacy group Faith in Action.

“I felt this sense of security that I know others don’t have because of status,” said Valencia.

In

the past, if Valencia needed to see a doctor, she would have to go to

the hospital because she didn’t have insurance. She still owes hospitals

thousands of dollars from the 18 years she didn’t have health

insurance.

Luckily, her Covid infection was mild. She saw a doctor

online and treated her sore throat, fever, fatigue and loss of appetite

with vitamins, sleep medication and other home remedies. She also spent

extra money to stay in an Airbnb while her apartment was sanitized and

to get food delivered for her and her parents, who she lives with,and

are at high risk for severe Covid.

She estimates that extra spending and medicine set her back $2,000.

Catalina Morales, 29, Minnesota: $5,000

Out-of-pocket costs: $5,000

Catalina Morales has spent about $5,000 on Covid care, even though she never had it.

Late

last year, she and her sister traveled from Minnesota to Chicago to

care for five close family members who had severe Covid-19 infections.

This includes her mom and another sister, who were hospitalized for more

than a week.

Meanwhile, Morales’s brother-in-law battled Covid at

home and took care of the couple’s two children, without paid sick

leave because he is undocumented. To help cover the family’s rent and

food, plus the sisters’ travel, Morales fundraised $5,000 by contacting

people she knows.

Morales, a Daca recipient and manager for the La

Red immigrant rights campaign, said the fundraising was only possible

because she is an activist and is familiar with the networks she could

tap to get help.

“Your regular undocumented immigrant doesn’t know

or doesn’t have those relationships,” Morales said. “If I didn’t have

that knowledge, my sister would not have paid her rent the last two

months and my sister and I would have had to use credit cards to pay for

all this.”

Those initial costs aren’t the family’s only financial concern.

Morales’s

mother had been living in the US undocumented until she received a visa

for victims of crime, but the paperwork is being processed. The

hospital, therefore, doesn’t consider her a US resident, blocking her

from qualifying for programs to help the uninsured.

The family will owe the hospital the fullbill,

and plans to negotiate to pay in installments. The average charge for

an uninsured Covid-19 patient’s hospitalization is $73,300, according to

the not-for-profit insurance database Fair Health.

Biden moving to withdraw Trump-approved Medicaid work rules

Democrats long complained the rules were illegal and aimed at shrinking health coverage for poor adults.

by Adam Cancryn - Politico - February 11, 2021

Former President Donald Trump listens as former Administrator of the

Centers for Medicare and Medicaid Services Seema Verma speaks during a

news conference Friday, Nov. 20, 2020. | Susan Walsh/AP

The Biden administration on Friday will notify states it plans to

revoke Medicaid work requirements, starting the process of dismantling

one of the Trump administration's signature health policies.

The move is one of several steps that Biden’s health department is

expected to take this week to unravel the contentious work rules long

criticized by Democrats, according to internal documents obtained by

POLITICO.

The documents — which were labeled “close hold” — do not make clear

how quickly Biden will cut off work rules the previous administration

approved in a number of states, which for the first time were allowed to

mandate that some people work or volunteer as a condition of enrollment

in the low-income health care program.

Healthofficials

are also preparing to withdraw the Trump administration’s 2018 letter

that first announced the work requirements policy, and rescind a

separate letter from earlier this year aimed at making it more difficult

for the incoming Biden administration to quickly overturn the policy.

“CMS

has serious concerns that now is not the appropriate time to test

policies that risk a substantial loss of health care coverage or

benefits in the near term,” according to a health department draft

rollout plan entitled “Medicaid Work Requirement Rescission.”

President Joe Biden, who has targeted other Trump health policies as he looks to build on Obamacare,

has long signaled plans to unravel the Medicaid work requirements.

Democrats have criticized the rules as unlawful and aimed at kicking

people off the program’s rolls.

Trump

Medicaid chief Seema Verma, who was critical of Obamacare's expansion

of Medicaid to poor adults and crafted the requirements, argued they

would encourage healthy people to work and help keep state Medicaid

programs financially sustainable.

Biden last

month issued an executive order directing his health department to

identify policies that fail to “protect and strengthen Medicaid.” But

the draft rollout plan obtained by POLITICO points to the coronavirus

pandemic as the central reason for rolling back the work rules, arguing

that the crisis has “greatly increased the risk” that the policy will

lead to “unintended coverage loss.”

“In

addition, the uncertainty regarding the lingering health consequences

of COVID infections further exacerbates the harms of coverage loss or

lack of access to coverage for the Medicaid beneficiaries,” the plan

said.

The move also comes as the

Supreme Court is slated to consider the validity of the work rules on

March 29. Lower courts have so far blocked attempts to institute the

work rules, which led most states with the requirements to halt their

enforcement. Biden's plan to withdraw the work rules could render the

Supreme Court case moot.

Centers for Medicare and Medicaid Services did not respond to multiple requests for comment.

Ten

GOP-led states that applied for the Trump administration's permission

for work rules were approved or “considered approved,” according to the

draft rollout plan. Several more states had sought permission for work

rules but had not been approved before Trump left office.

The

work rules were approved through Medicaid waivers, which allow states

to test ideas for health coverage. A new administration typically can

unwind waivers that it believes does not support Medicaid goals, though

states may protest the decision.

In the final weeks of the Trump administration, Verma asked states to

sign contracts that would establish a lengthy process for unwinding

work requirements and other conservative changes to their Medicaid

programs. Medicaid experts have questioned whether those contracts are

legally enforceable.

The health department onFriday is also planning to scrub some

references to the work requirements program and related documents from

the government's Medicaid website.

Instead, it will post a link to an HHS document entitled “Medicaid

Demonstrations and Impacts on Health Coverage: A Review of the

Evidence.” The document, among other topics, will address the “impact of

work requirements on Medicaid’s commitment to Americans in need,” the

draft rollout plan said.

Only one state, Arkansas, ever fully implemented the Medicaid work

rules. About 18,000 people lost Medicaid coverage in 2018 during the few

months the requirements were in effect, before a judge blocked them.

William Clark and Larry Kaplan: Every Maine resident deserves health care.

Universal healthcare — everyone in, no one out — creates unity and solidarity: foundational aspects of American democracy.

Does anyone in your family lack health insurance? Are you foregoing needed medical care? Have you received a “surprise” medical bill. How do Maine residents answer these questions? In autumn 2019, more than 80 volunteers with Maine AllCare interviewed a sample of 3,864 people from every Maine county and 287 towns. The survey, funded by Maine Health Access Foundation, found that while most respondents had health insurance, 78% labeled their health care coverage is “unaffordable.” Forty-two percent reported that they had delayed treatment because of cost while over half received unexpected medical bills that impacted their finances. Most importantly, 81% said they would support “a publicly-funded healthcare system that covered everyone in Maine.”

Also, medical providers complain that they are handcuffed and overburdened by the healthcare system’s complexity and endless administrative paperwork that does not facilitate care. Rural hospitals are threatened with closure. Today’s pandemic underscores the fact that our current system of health care serves both providers and patients poorly, while exorbitant profits flow to insurance corporations, device manufactures and pharmaceutical companies.

Universal healthcare is both equitable and economically viable. Other wealthy countries cover everyone for half to two-thirds of United States costs. Meanwhile, data show that many countries enjoy health outcomes superior to the United States. Advocacy coalitions and legislatures in other states — notably California, Washington, Minnesota and New York — are exploring implementation of universal healthcare. If implemented, these proposals provide more comprehensive benefits than the present ACA plans.

Locally, the Maine Center for Economic Policy examined in 2019 how a hypothetical universal healthcare system would work in Maine. The MECEP study analyst and author James Myall wrote: “I don’t think that it’s impossible for the state to do this, at least from an economic standpoint.” Myall said that Maine residents would save money, despite any new taxes, because care would be virtually free. Moreover, without the need to pay premiums, deductibles or copays, at least 85-90% of families would thus come out ahead and have more cash to spend. Furthermore, businesses would be unburdened from the cost of employee health insurance. Crucially, no person would be uninsured during a pandemic or economic crisis.

Maine Healthcare Action, a nonprofit 501(c)(4) organization started by local Maine physicians and concerned residents, has launched a campaign to put direct pressure on our Legislature in the form of a citizens-initiated resolve. The resolve directs the Legislature “to develop legislation to establish a system of universal healthcare coverage in the State and directs the joint standing committee to report out a bill to the Legislature to implement its proposal by 2024.”

We have begun to collect petition signatures to approve the resolve that will be presented to Maine voters in November 2022. The resolve is simple and straightforward, reflecting the will of the electorate that our Legislature address the inequities and costs of a dysfunctional delivery system and pass comprehensive healthcare reform. Any legislation should be tailored to the needs of Maine residents, and unlike today’s “take it or leave it” insurance-based system, the Legislature could guarantee health care, not just “coverage.”

Universal healthcare — everyone in, no one out — creates unity and solidarity: foundational aspects of American democracy.

William Clark, MD, of Brunswick is a board member with Maine Healthcare Action. Larry Kaplan, MD, MPA, of Cape Elizabeth is the organization’s chairman.

No comments:

Post a Comment