Pence Breaks Tie as Senate Votes to Begin Debating Obamacare Repeal

by Thomas Kaplan and Robert Pear - NYT - July 25, 2017

WASHINGTON — The Senate narrowly voted on Tuesday to begin debate on a bill to repeal major provisions of the Affordable Care Act, taking a pivotal step forward after the dramatic return of Senator John McCain, who cast a crucial vote despite his diagnosis of brain cancer.

Vice President Mike Pence cast the tie-breaking vote.

The 51-50 vote came only a week after the Republican effort to dismantle a pillar of former President Barack Obama’s legacy appeared all but doomed. It marked an initial win for President Trump, who pushed, cajoled and threatened senators over the last days to at least begin debating the repeal of the health care law.

But even with that successful step, it is unclear whether Republicans will have the votes they need to uproot the law that has provided health insurance to millions of Americans. The Senate will now begin debating, amending and ultimately voting in the coming days on legislation that would have a profound impact on the American health care system.

By a single vote, the Senate cleared the way for an epic battle over the future of the health law. Only two Republicans, Susan Collins of Maine and Lisa Murkowski of Alaska, voted against the motion. The debate has broad implications for health care and households in every state.

Senate Republican leaders have struggled all year to fulfill their promise of repealing the 2010 health care law, and the procedural vote in the Senate on Tuesday risked being another big setback for the party. The House narrowly approved a repeal bill in early May, but only after Republicans overcame their own difficulties in that chamber.

President Trump kept up the pressure on Tuesday by posting on Twitter. “After 7 years of talking,” he said, “we will soon see whether or not Republicans are willing to step up to the plate!”

The successful procedural vote on Tuesday is an important step forward for the Senate majority leader, Mitch McConnell of Kentucky, who only a week ago appeared to have failed in his effort to put together a health bill that could squeak through the narrowly divided Senate.

That said, it remained far from certain whether Republicans would actually be able to agree on a bill in the days to come — and what exactly the contents of that bill would be.

For weeks, Mr. McConnell has been promoting and revising a comprehensive bill that would repeal the health law while also replacing it, but he has struggled to nail down the necessary support to pass that measure.

An alternative would be to pass a narrower bill that would repeal the health law without putting in place a replacement, but that approach has been greeted with objections from some Republicans as well.

Senate Parliamentarian Challenges Key Provisions of Health Bill

by Robert Pear and Thomas Kaplan - NYT - July 21, 2017

WASHINGTON — The Senate Republican bill to dismantle the Affordable Care Act encountered huge new problems on Friday night after the Senate parliamentarian challenged key provisions that are needed to win conservative votes and to make the health bill workable.

The provisions appear to violate Senate rules, the parliamentarian said, giving Democrats grounds to challenge them as the Senate prepares for a battle next week over the future of the Affordable Care Act.

One provision questioned by the parliamentarian, Elizabeth MacDonough, and cherished by conservatives would cut off federal funds for Planned Parenthood for one year. Another would prohibit use of federal subsidies to buy insurance that includes coverage for abortions.

A third provision would penalize people who go without health insurance by requiring them to wait six months before their coverage could begin. Insurers would generally be required to impose the waiting period on people who lacked coverage for more than about two months in the prior year.

If formally challenged, the provisions could survive only with 60 votes, a near-impossibility in the partisan, narrowly divided Senate. The abortion-related provisions are important to many conservatives, not just in the Senate but also in the House.

And Democrats made clear they would seize on the findings. “The parliamentarian’s decision today proves once again that the process Republicans have undertaken to repeal the Affordable Care Act and throw 22 million Americans off of health insurance is a disaster,” said Senator Bernie Sanders, independent of Vermont.

Mr. Sanders, the ranking member of the Senate Budget Committee, disclosed the preliminary decisions by the parliamentarian.

The waiting period provision is fundamental to the working of the bill. Because the legislation would end the Affordable Care Act’s mandate that most Americans have health insurance, the waiting period was designed to ensure that people could not simply wait to get sick before they purchased a policy.

Senate Republican leaders plan to begin debate next week on repealing the Affordable Care Act, President Barack Obama’s signature domestic achievement, which has provided health insurance to roughly 20 million Americans.

At the moment, Republican leaders lack the votes to ensure passage of their bill to repeal and replace the law, and they are still modifying it in hopes of gaining support from uncommitted Republican senators. All Democrats are expected to oppose the repeal bill.

Under the procedure that Republicans are using to speed passage of the health care bill, senators can object to a provision if it does not change federal spending or revenue or if the budgetary effects are “merely incidental” to some policy objective. The parliamentarian serves as a sort of referee, determining whether specific provisions of the bill comply with Senate rules.

Don Stewart, a spokesman for the Senate majority leader, Mitch McConnell, Republican of Kentucky, emphasized that “this is guidance, not a ruling.” The parliamentarian “provided guidance,” and that guidance will help inform subsequent drafts of the legislation, he said, suggesting that the bill could be revised to answer her questions.

The Senate’s presiding officer usually follows advice from the parliamentarian. But the full Senate can vote to overturn those decisions.

The parliamentarian also objected to a narrowly written provision that would shift Medicaid costs from New York’s counties to its state government. This provision, tagged by opponents as the “Buffalo Bailout,” was included in a repeal bill passed by the House in May to secure the votes of Republican House members from upstate New York.

The Senate Democratic leader, Chuck Schumer of New York, suggested that other provisions written specifically for different states could also be at risk.

“This will greatly tie the majority leader’s hands as he tries to win over reluctant Republicans with state-specific provisions,” Mr. Schumer said. “We will challenge every one of them.”

Even before the parliamentarian’s blow, Trump administration officials and Republican leaders were struggling to win over moderate Republicans with a new infusion of money to help people who would lose Medicaid under the Senate health care bill.

Senators are set to return to the Capitol on Monday, and Republican leaders are eager to begin debate in the Senate on health care, perhaps as early as Tuesday. It is unclear they have the votes needed to start the debate, let alone to ensure passage of a bill to repeal and replace the health care law.

In their latest bid for agreement on a plan to undo the health care law, Senate Republicans are weighing a proposal to add funds, perhaps $200 billion, to the bill to help low-income people transition from Medicaid to private insurance. But Republican leaders must balance the interests of senators from states that expanded Medicaid under the Affordable Care Act with the goals of fiscal conservatives, who see the repeal bill as a once-in-a-generation opportunity to rein in the growth of one of the nation’s largest entitlement programs.

“You can only go so far, and then you lose votes on one side where we want to make reforms within Medicaid,” Senator Michael Rounds, Republican of South Dakota, said after a lengthy meeting this week with administration officials and other Republican senators. “And if you don’t go far enough, then you’ve got folks that are concerned that we’re making the changes too quick. So it’s that balancing act of trying to keep everybody on board and feeling comfortable.”

The Congressional Budget Office says the Senate repeal bill would cut projected federal Medicaid spending by more than $750 billion in the coming decade, leaving 15 million fewer people on Medicaid in 2026, compared with the enrollment expected under current law.

Those cuts have caused deep concern to Republican senators from states that expanded Medicaid under the Affordable Care Act, including Rob Portman of Ohio, Shelley Moore Capito of West Virginia and Lisa Murkowski of Alaska.

“I would like to do more to help people at the low end of the income scale afford private health insurance,” Mr. Portman said, noting that more than 700,000 people in his state had gained coverage through the expansion of Medicaid under the Affordable Care Act.

Ms. Capito, in a video message on Friday, said that many of her constituents had been hurt by the Affordable Care Act, but that “many West Virginians have benefited from our state’s decision to expand Medicaid” under the health law.

“I have said all along that we need to both repeal and replace Obamacare, and I’m not giving up on that goal,” she said. But, she added, “We aren’t there yet.”

Opponents of repeal, including consumer advocates and health care providers in every state, are keeping up the pressure on Republican senators.

AARP called on senators to vote against the procedural motion to begin debate, while the American Medical Association panned the repeal measure and an alternate Senate bill that would repeal the health law without providing a replacement.

“Recent revisions do not correct core elements that will lead to millions of Americans losing health insurance coverage with a resulting decline in both health status and outcomes,” Dr. James L. Madara, the association’s chief executive, wrote to Senate leaders on Friday. The Senate legislation, he said, would undermine state Medicaid programs and weaken the individual insurance market.

Save My Care, a group that is fighting the repeal effort, is targeting Ms. Capito, Ms. Murkowski and Senator Dean Heller, Republican of Nevada, with new television commercials urging them to vote against repealing the health law.

“Senator Capito promised to protect our health care,” one of the ads says. “Now Washington insiders are pressuring her to back down.”

On the flip side, Republican senators risk angering conservative supporters — as well as President Trump — if they stand in the way of the repeal effort, perhaps by opposing the procedural motion to begin debate that is planned for next week.

“I don’t know how you face the people who elected you when you don’t even vote to take up the bill,” Senator Ted Cruz, Republican of Texas, said on Fox News.

Health Care Is Still in Danger

Paul Krugman - July 24, 2017

Will Senate Republicans try to destroy health care under cover of a constitutional crisis? That’s a serious question, based in part on what happened in the Houseearlier this year.

As you may remember, back in March attempts to repeal and replace the Affordable Care Act seemed dead after the Congressional Budget Office released a devastating assessment, concluding that the House Republican bill would lead to 23 million more uninsured Americans. Faced with intense media scrutiny and an outpouring of public opposition, House leaders pulled their bill, and the debate seemed over.

But then media attention moved on to presidential tweets and other outrages — and with the spotlight off, House leaders bullied and bribed enough holdouts to narrowly pass a bill after all.

Could something similar happen in the Senate? A few days ago the Senate’s equally awful version of repeal and replace — which the C.B.O. says would leave an extra 22 million people uninsured — seemed dead. And media attention has visibly shifted off the subject, focusing on juicier topics like the Russia-Trump story.

This shift in focus is understandable. After all, there is growing evidence that members of the Trump inner circle did indeed collude with Russia during the election; meanwhile, Trump’s statements and tweets strongly suggest that he’s willing both to abuse his pardon power and to fire Robert Mueller, provoking a constitutional crisis, rather than allow investigation into this scandal to proceed.

But while these developments dominate the news, neither Mitch McConnell nor the White House have given up on their efforts to deprive millions of health care. In fact, on Saturday the tweeter-in-chief, once again breaking long-established rules of decorum, called on the audience at a military ceremony, the commissioning of a new aircraft carrier, to pressure the Senate to pass that bill.

This has many people I know worried that we may see a repeat of what happened in the spring: with the media spotlight shining elsewhere, the usual suspects may ram a horrible bill through. And the House would quickly pass whatever the Senate comes up with. So this is actually a moment of great risk.

One particular concern is that the latest round of falsehoods about health care, combined with the defamation of the C.B.O., may be gaining some political traction.

At this point the more or less official G.O.P. line is that the budget office — whose director, by the way, was picked by the Republicans themselves — can’t be trusted. (This attack provoked an open letter of protest signed by every former C.B.O. director, Republicans and Democrats alike.) In particular, the claim is that its prediction of huge losses in coverage is outlandish, and that to the extent that fewer people would be covered, it would be due to their voluntary choices.

In reality, those C.B.O. predictions of coverage losses are totally reasonable, given the Senate bill’s drastic cuts to Medicaid — 26 percent by 2026, and even deeper in the next decade. You have to wonder how someone like Senator Shelley Moore Capito of West Virginia could even consider supporting this bill, when 34 percent of her nonelderly constituents are on Medicaid. The same goes for Jeff Flake of Arizona, where the corresponding number is 29 percent.

And on those claims that it’s O.K. if people drop coverage, because that would be their own choice: It’s crucial to realize that the Senate bill would degrade the quality of subsidized private insurance, leading to a huge rise in deductibles.

Current law provides enough in subsidies that an individual with an income of $26,500 can afford a plan covering 70 percent of medical expenses, which, the C.B.O. estimates, implies an $800 deductible. The Senate bill reduces that standard of coverage to 58 percent, which would raise the implied deductible to $13,000, making the insurance effectively useless. Would deciding not to buy that useless insurance really be a “choice”?

By the way, remember when Republicans like Paul Ryan used to denounce Obamacare because the insurance policies it offered had high deductibles? It’s hypocrisy all the way down.

In short, the Senate bill is every bit as cruel and grotesque as its critics say. But we need to keep reminding wavering senators and their constituents of that fact, lest they be snowed by a blizzard of lies.

I’m not saying that everyone should ignore Trump-Putin-treason and all its ramifications: Clearly, the fate of our democracy is on the line. But we mustn’t let this mother of all scandals take up all our mental bandwidth: Health care for millions is also on the line.

And while ordinary citizens can’t yet do much about the looming constitutional crisis, their calls, letters, and protests can still make all the difference on health care. Don’t let the bad guys in the Senate do terrible things because you weren’t paying attention!

How health care controls us

by Robert J. Samuelson - Washington Post - July 23, 2017

If we learned anything from the bitter debate over the Affordable Care Act (Obamacare) — which seems doubtful — it is that we cannot discuss health care in a way that is at once compassionate and rational. This is a significant failure, because providing and financing health care have become, over the past half-century, the principal activity of the federal government.

If you go back to 1962, the earliest year with such data, federal health spendingtotaled $2.3 billion, which was 2.1 percent of the $107 billion budget. In 2016, the comparable figures were $1.2 trillion in health spending, which was 31 percent of the $3.85 trillion budget. To put this in perspective, federal health spending last year was twice defense spending ($593 billion) and exceeded Social Security outlays ($916 billion) by a comfortable margin.

The total will grow, because 76 million baby boomers are retiring, and as everyone knows, older people have much higher medical costs than younger people. In 2014, according to the Kaiser Family Foundation, people 65 and over had average annual health costs of $10,494, about three times the $3,287 of people 35 to 44. Medicare and Medicaid, nonexistent in 1962, will bear the brunt of higher spending.

At a gut level, we know why health care defies logical discussion. We personalize it. We assume that what’s good for us as individuals is also good for society. Unfortunately, this is not always true. What we want as individuals (unlimited care) may not be good for the larger society (overspending on health care).

Our goals are mutually inconsistent. We think that everyone should be covered by insurance for needed care; health care is a right. Doctors and patients should make medical choices, not meddlesome insurance companies or government bureaucrats; they might deny coverage as unneeded or unproven. Finally, soaring health spending should not squeeze wages or divert spending from important government programs.

The trouble is that, in practice, we can’t meet all these worthy goals. If everyone is covered for everything, spending will skyrocket. Controlling costs inevitably requires someone to say no. The inconsistencies are obvious and would exist even if we had a single-payer system.

The ACA debate should have been about reaching a better balance among these competing goals — and explaining the contradictions to the public. It wasn’t.

The ACA’s backers focused on how many Americans would lose coverage under various Republican proposals — more than 20 million, the Congressional Budget Office has estimated. The ACA’s entire gain in coverage would be wiped out, and then some. From 2013 to 2015, the number of insured Americans rose by 13 million, estimates Kaiser. But the ACA’s advocates don’t say much about stopping high insurance costs from eroding wage gains or strangling other government programs.

Meanwhile, congressional Republicans and the Trump White House proposed huge cuts in health spending — $1 trillion over 10 years for the ACA’s repeal alone — while implausibly suggesting that hardly anyone would be hurt or inconvenienced. There was no coherent strategy to reconcile better care with lower costs. Democrats kept arguing that the health cuts were intended to pay for big tax cuts that would go mainly to the rich and upper middle class. Sounds right.

Still, there’s no moral high ground. Some Democrats have wrongly accusedObamacare opponents of murder. This is over-the-top rhetoric that discourages honest debate. It’s also inconsistent with research. Kaiser reviewed 108 studies of the ACA’s impact and found that, though beneficiaries used more health care, the “effects on health outcomes” are unclear.

We are left with a system in which medical costs are highly concentrated with the sickest patients. (The top 5 percent account for half of all medical spending.) This creates a massive resource transfer, through insurance and taxes, from the young and middle-aged to the elderly. (Half of all health spending goes to those 55 and over, who represent just over one-quarter of the population).

And yet, we govern this massive health-care sector — representing roughly a third of federal spending and nearly a fifth of the entire economy — only haphazardly, because it responds to a baffling mixture of moral, economic and political imperatives. It will certainly strike future historians as curious that we tied our national fate to spending that is backward-looking, caring for people in their declining years, instead of spending that prepares us for the future.

We need a better allocation of burdens: higher eligibility ages for Social Security and Medicare; lower subsidies for affluent recipients; tougher restrictions on spending. But this future is impossible without a shift in public opinion that legitimizes imposing limits on health spending.

We didn’t get that with the eight-year Obamacare debate. The compassionate impulse overwhelmed the rational instinct. The result is that health care is controlling us more than we are controlling it.

Thousands flock to free medical clinic, as Washington dithers on health care

by Gregory S. Schneider - Washington Post - July 21, 2017

The sick and the disabled pour out of these mountains every summer for their one shot at free health care, but this year was supposed to hold hope for a better solution.

Donald Trump won the White House in part on a promise to fix the nation’s costly and inefficient health-care system. Instead, Republicans in Congress are paralyzed and threatening to dismantle the imperfect framework of Obamacare.

No relief is in sight for someone like Larry McKnight, who sat in a horse stall at the Wise County Fairgrounds having his shoulder examined. He was among more than a thousand people attending the area’s 18th annual Remote Area Medical clinic, where physicians and dentists dispense free care to those who otherwise have none.

“I really think that they don’t have any clue what’s going on,” McKnight said of political leaders in Washington. “You watch the news and it’s two sides pitted against each other, which in turn just makes them pitted against us, the normal person.”

About 1,100 such people descended on the fairgrounds Friday, with more expected Saturday and Sunday. Medical personnel from across the state were there with makeshift examination rooms in tents and sheds. Sheets hung from clothespins for privacy; giant fans pulled hot air through buildings intended for livestock shows.

These events are staged nationwide, but the Wise clinic is among the biggest, drawing people from throughout Appalachia and casting Washington’s sterile political debates into the starkest human terms.

A third of the patients who registered Friday were unemployed. Those who couldn’t afford a room slept in their cars or camped in the fields around the fairgrounds. They lined up in the dead of night to get a spot inside the event.

It is the place of last resort for people who can’t afford insurance even under Obamacare or who don’t qualify for Medicaid in a state where the legislature has resisted expansion.

At 37, with a long graying ponytail, McKnight had never been sick until about eight months ago. So he hadn’t worried too much about not being able to afford insurance on his roughly $18,000 a year in pay as an auto mechanic. But now he was getting a referral to the University of Virginia hospital to check for the source of his pain, which he had vowed to withstand without resorting to opioid medication.

“The normal person doesn’t care about a lot of the things that they care about [in Washington]. Most people want to work, they want insurance and they want to be able to take care of their family without assistance,” he said.

The only way to do that, he said, is to have everybody — the healthy and the sick — paying into a centralized health insurance plan. “I really think the only thing that would truly help this country is if it were single-payer,” McKnight said.

Around here, that’s not politics, it’s just life. Many of these people voted for Trump — not only for his vow to fix health care, but also for his promise to bring back the coal industry. They’re still waiting for results, with varying degrees of patience.

Patricia McConnell was having trouble speaking around the bloody gauze in her mouth. She had just had four teeth pulled. The unemployed former manager of a McDonald’s had driven eight hours from her home in Glen Burnie, Md., to attend the clinic.

Virginia Gov. Terry McAuliffe hugs Patricia McConnell, who saved money for six months for gas and a hotel room to attend the Remote Area Medical event and have dental work done. (Michael S. Williamson/The Washington Post)

“My teeth were hurting,” she said. McConnell, 63 and disabled, said she had health insurance through Medicaid but no dental coverage.

So this was her dental plan: She’d save for six months to afford a motel room and gas, then wait in line in the morning heat to see a volunteer dentist.

McConnell has been watching the health-care debate in Washington and wondering if it will ever amount to anything that actually helps people like her. “I don’t know what they’re trying to do,” she said, struggling to get the words out around the gauze.

She voted for Trump, she said, and still feels that he’s working hard to help. But his anger and his tweets seem to aggravate Congress, and no one is working together, she said.

They need to set all that aside and work to pass health care for everyone, she said. “Let’s get this done.”

Others had a hard time mustering the faith that anyone cared.

“They’re trying to kill us poor people, is what they’re trying to do,” said Robert Horne, 55, a disabled former construction worker seeking dental care. Horne said he voted for Hillary Clinton last fall because of her pledge to maintain the Affordable Care Act.

That didn’t work out, either.

Virginia Gov. Terry McAuliffe (D), who flew out to the clinic Friday morning, had invited Senate Majority Leader Mitch McConnell to join him but said that the Republican leader “politely” declined. McAuliffe, who visits the clinic every year, spent nearly two hours touring it — twice as long as scheduled — and took every opportunity to proclaim that he’s been trying for three years to get the state legislature to agree to expand Medicaid under Obamacare.

The Republican-controlled General Assembly has resisted, unlike the legislatures in nearby states, which McAuliffe kept reminding the patients and doctors who crowded around him on the hot fairgrounds.

“All of our neighbors in Kentucky and West Virginia and Maryland — they did it!” he said to a Christian counseling group that had set up shop under an awning. But in Virginia, he said, legislators turned down millions in federal dollars that would be available under Medicaid expansion.

“We need it,” called out Tonya Hall, operations director for a hospice-care facility. “Let them come and visit some in southwest Virginia. Let them see the poverty. Let them see how we live. Let them come.”

“This isn’t about politics,” McAuliffe said.

“Right!” Hall agreed. “It’s about people.”

“It’s about people’s lives,” McAuliffe said to a round of “Amens” from the group.

Hall, 42, said she had voted for Trump but that she was disappointed he hadn’t been able to do anything to improve the health-care system. If Obamacare can’t be fixed, she said, “then I say we scrap it and start over. You can see the need,” she added, gesturing at the masses of people waiting for their turn with a medical professional.

Beyond her, a long line stretched into the triage tent, where people were sorted and their vital signs measured. Allen Sexton, 37, was there to have all his teeth removed, years after a car accident had left them a scrambled mess.

In a metal shed nearby, vision specialists sat in darkness, performing eye exams in pools of light. One man said that his glasses had broken a year ago and that he couldn’t see at a distance or up close, but he’d been driving anyway.

There was another tent for orthopedic care. Another for basic checkups. Each one was full, with more people waiting outside on metal folding chairs or standing in lines.

Politicians prowled the fairgrounds. Several area legislators attended while Attorney General Mark Herring (D), running for reelection, walked with McAuliffe and Sen. Tim Kaine (D) helped register patients.

Stan Brock, the English philanthropist who founded the RAM clinic program more than 30 years ago, said there was one more visitor he’d like to see at the clinic.

“It’s absolutely imperative that the president of the United States come and visit one of these events,” he said. “I believe if he did, he would take some immediate action.”

by Martin U. Muller - Der Spiegel Online - July 20, 2017

The health care sector is facing a far-reaching and unpredictable revolution. Smartphones are capable of replacing many devices that have become standard in medical practices and some apps will soon be able to provide diagnoses as well. Patients are becoming less reliant on doctors.

The airplane had just taken off when one of the passengers lost consciousness. Eric Topol pulled his smartphone out of his pocket and immediately performed an electrocardiogram (EKG) on the passenger. He used the device to do an ultrasound scan of the man's heart and measured oxygen levels in his blood. He was then able to give the all-clear and the plane could continue its journey. The man had lost consciousness merely due to a temporarily slowed heart rhythm.

Topol is a cardiologist in La Jolla, California, and it wasn't the first time he had encountered such a situation while flying. On one occasion, he used his mobile phone to determine that a passenger had suffered a heart attack and the plane had to land immediately. Of particular interest to Topol, though, is the fact that anyone can perform such an EKG, whether a professor of medicine, a flight attendant or just a simple passenger. All one needs is a $200 sensor and a smartphone with an app that can analyze the heart's rhythm.

Hardly any other object has changed the world to the degree that smartphones have. It has become completely normal to use our mobile devices for shopping and managing our schedules. Political revolutions have been organized by smartphone and you can use one to find a life partner or to plan a funeral. Every single day, 10 times as many smartphones are sold around the world as babies born. And now, smartphones are conquering medical care.

For millennia, sick people have been dependent on help from others, a healer or a doctor. But now, mobile devices are beginning to change that age-old state of affairs. Coupled with the power of artificial intelligence, the mobile phone promises to fundamentally change medical care. Many medical examinations that were thus far only possible in a doctor's office can now be undertaken at any time by anyone -- even while sitting at home in your easy chair.

With the help of small and affordable accessories, smartphones can measure electrical activity in the brain, intraocular pressure and blood pressure. They can perform an EKG, recognize atrial fibrillation (a type of abnormal heart rhythm), check pulmonary function, record heart murmurs, take photos of your inner ear, perform breathalyzers, perform aorta scans and even sequence DNA.

Soon, there will be little difference from a technical standpoint between a general practitioner's office and a fully equipped smartphone. On the contrary: It is already the case that patients are sometimes better served by a mobile phone.

Doctors Have Competition

Apps like M-sense are revolutionizing migraine diagnostics. At the University of Magdeburg in Germany, a mobile phone program called Neotiv is being developed to reliably diagnose Alzheimer's. There are even scanners reminiscent of the "Star Trek" Tricorder: You simply hold it up to a patient's forehead and receive diagnostic information within seconds. An Israeli company has developed SCiO, the first smartphone app for mass spectrometry. If you briefly hold it up to an apple, for example, its exact composition will appear on your display. The app also works on pills: Using the app, the device scans an object's structure, compares it with a database and then tells you what it is -- a paracetamol tablet, for example. Even today, such a test is far from standard, even in hospital emergency rooms.

It is far from clear what all of these changes will mean for the health care industry -- for patients and doctors and for the manufacturers of large medical devices that may soon no longer be necessary. One thing, though, is certain: Doctors have competition, and that competition is stimulating the industry. Within just a few years, patients won't just be able to decide which doctor to go to, but will also be able to choose between local doctors, online diagnoses and intelligent scanning devices -- and they will perhaps even be able to undergo an examination in their own cars.

The patient is becoming more powerful -- and doctors are becoming less essential.

A BILLION-DOLLAR INDUSTRY

The first wave of health apps was made up of tracking bracelets and similar accessories that were rightly mocked as glorified pedometers. But the second wave is developing into a significant player in the medical technology branch. Investors have begun referring to the development as "serious health," and there is money to be made. A lot of money. But there are other issues at stake as well, such as trust and the potential for overwhelming the traditional health care system.

International Newsletter

Sign up for our newsletter -- and get the very best of SPIEGEL in English sent to your email inbox twice weekly.

The epicenter of digital medicine is not in Silicon Valley, as it tends to be for social media giants like Facebook or Snapchat. Rather, it is on the East Coast of the United States, in Israel and in Europe.

One of the leaders of the scene in Berlin is Markus Müschenich. Ever since he decided to devote his life to digital medicine, the 56-year-old's life has been unrelenting: here, an appointment with German Health Minister Hermann Gröhe, there a video conference with a promising startup. Müschenich is pretty much constantly speaking into the headset of his telephone, and when he's not, he is giving presentations to doctors, insurance company officials and politicians. A former pediatrician, he always wanted to do more than just treat patients. "I still don't regret having set aside my lab coat," he says.

Müschenich was part of the management team at a hospital in Berlin before becoming a member of the board of directors at Sana, a chain of hospitals and clinics in Germany. But he didn't find his true calling either in pediatrics or in analyzing the economic data of heart centers. He moved on to found a company that developed an app to help cure cross-eyed children -- and then convinced the health insurance company Barmer to refund the price of the app to its customers. The result was the first-ever prescription app. Today, he owns the company Flying Health, an incubator for medical industry startups that shares both its money and know-how. His portfolio includes Patientus, a Lübeck-based company that offers doctor consultations by video link, and he offers consulting to the diabetes startup mySugr, which was just recently sold to the Swiss pharma-giant Roche. He is also involved in a company developing software for pregnant women called Onelife and is trying to increase the value of Neotiv, the company that is developing an app to identify Alzheimer's.

Müschenich and his 10 employees work out of a co-working space in Berlin that is shared by other startups. And he has adopted the scene's typically effusive optimism. "Every day, I see young people here who demonstrate that they are better than we are. That's inspiring."

Currently, the health care system consists of the in-patient and out-patient sectors, but economists in the industry are convinced that the digital sector will soon join them. Germany currently spends a total of 350 billion euros ($403 billion) per year on health care, and the high-tech segment will certainly siphon some of that money off from the traditional sectors like hospital and practice care. Müschenich expects the digital medical care sector in Germany to be worth 100 billion euros by 2025. "From an organizational standpoint, the digital sector will come before the two other sectors," Müschenich says. In the future, he explains, doctors will become dependent on getting references from digital systems.

Experts at the Gottlieb Duttweiler Institute (GDI), a future-oriented think tank in Switzerland, likewise believe that smartphones will become the "core interface" of the health care system. "Cost pressures will push the system towards digital," says Karin Frick, head of research at GDI. "It seems logical for patients to undergo an initial examination using smartphone systems. Companies that understand that first will be the winners."

THE PRODUCERS

Not far from the airport in Hamburg, on Röntgen Street -- named after the German physicist who discovered the electromagnetic radiation used in X-rays -- the German headquarters of Philips can be found. Today, the Dutch multinational is no longer the same company it was for the almost 100 years prior to 2014 and the change can even be seen in the architecture. Floors here have been given the names of different Hamburg neighborhoods and meetings are held in "boxes." The CEO has a desk in an open-plan office space and next to the restrooms, there are mounted pods for employees' mobile phones.

Televisions that bear the Philips name no longer have anything directly to do with the company -- the brand has been licensed out. The light bulb division has likewise been sold off. The only thing left is medical equipment. "Wherever I go, I have to explain that the Philips of today is purely a medical technology company," says Peter Vullinghs, Philips head in Germany and manager of 4,800 employees. He does, though, see parallels with the television business, which he once ran. "They went from being high-end products to simple consumer goods. The same thing is now happening with medical technology," he says. A slew of new competitors has joined the market, including Vullinghs says, Google, Apple, Samsung and IBM.

The Case Against the Public Option

by Adam Gaffney - Jacobin - July 19, 2017

The saga of Trumpcare may finally be behind us.

The wretched bill would have wrenched coverage from tens of millions, and — by many estimates — cost tens of thousands of lives a year. Liberals and leftists rightly united in opposition against it. And though Republicans are reportedly still planning on holding an Obamacare repeal vote next week, their agenda seems to have basically crumbled under the weight of mass opposition.

But if the Right’s health care agenda is dead, what is the next move for the Left?

It is by no means a settled question, for once we move past the question of fighting the repeal of the Affordable Care Act (ACA), a divide opens up — including within the Democratic Party, which will sooner or later return to power. On the one side are the most ardent supporters of Medicare for All; on the other, those who couple a defense of the ACA with advocacy for more incremental reforms, like the public option, which in most current iterations would be agovernment-run health care plan that would compete against private insurers on the ACA’s state-based marketplaces.

Admittedly, there is some overlap between the two camps: many look to the public option as a short-term, feasible reform that could help millions of people today, while serving as a stepping stone to a universal system in the future. Yet there is another case to be made: that a public option would be a largely ineffective less-than-half-measure, the pursuit of which could prove to be a major diversion that would paradoxically serve to perpetuate the injustices of the status quo.

Which is it? This is a debate worth having right now, well in advance of the 2018 and 2020 elections that may well determine the fate of the US health care system.

Before delving into this debate, it’s first necessary to lay some groundwork: what is the public option, and where it did it come from? What might it achieve, and what would it leave undone? And finally: should we embrace it or reject it in the days to come?

Choice and Competition

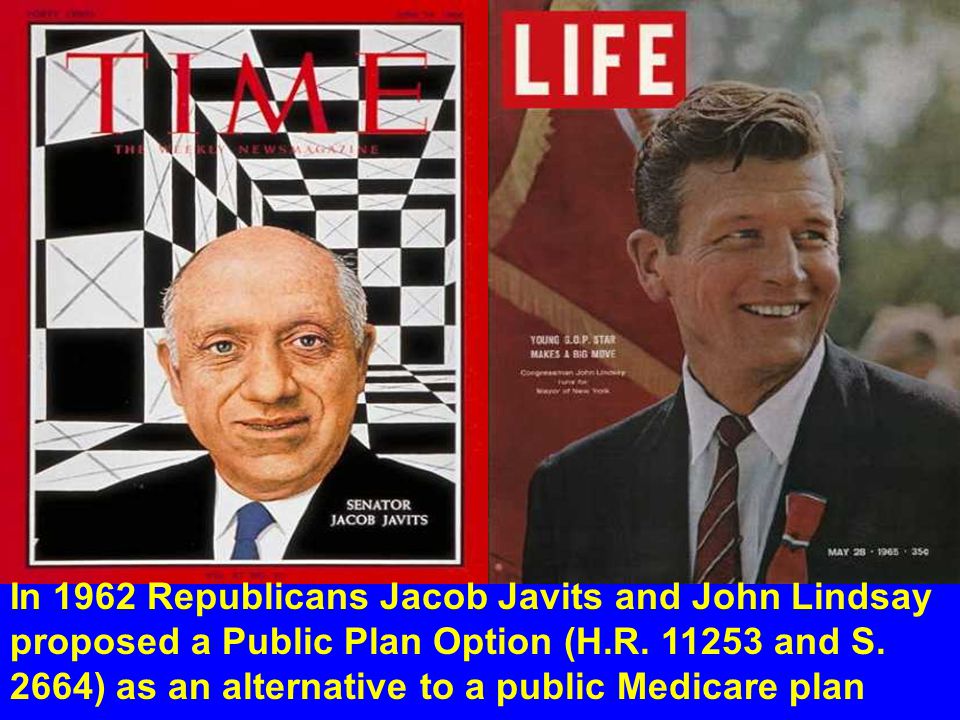

In concept at least, the public option has its roots — as public health scholars David Himmelstein and Steffie Woolhandler have noted — in the early 1960s, as an alternative to Medicare.

{kind=link}

At the time, Wilbur Mills, the Democratic chairman of the House Ways and Means Committee and a well-known fiscal hawk, was obstinately holding up President Kennedy’s Medicare bill. As Philip J. Funigiello describes in Chronic Politics: Health Care Security from FDR to George W. Bush, moderate Republican lawmakers Jacob Javits and John Lindsay offered two bills as a potential compromise to break the gridlock.

“Important to Javits’ proposals and to other alternatives offered at the time,” historian Edward Berkowitz writes, “was the notion of choice. . . . [Consumers] could either accept government health insurance, to be run by the States, or a private health care plan.”

Therein lies the essence of the public option: it’s designed to offer a choice between private and public insurance. Thankfully, Javits’s and Lindsay’s bipartisan bills were rejected: had a compromise been reached, Medicare as we know it today would simply not exist. Instead, Democrats went on to wallop the Republicans in the 1964 election, and Medicare was passed and signed into law the following year as a basically public program (for the time being, anyway).

The current iteration of the public option is of a more recent vintage. Its genesis can be traced to two proposals that emerged in the first decade of the twenty-first century. In a 2010 article in Health Affairs, Helen Halpin and Peter Harbage locate the origins of the public option in a health care reform proposal called “CHOICE,” which was developed by a group of health care leaders who convened in Berkeley in 2001–2, led by Halpin.

CHOICE was a proposal for a “managed competition” model for California in which the public option competed against private plans in a state marketplace. (Most current public option proposals use something of the same template, albeit for the nation as a whole.)

The plan fell by the wayside until the 2008 Democratic presidential primary, when John Edwards released a health care reform proposal that, Halpin and Harbage note, “encompassed the principles of CHOICE.” While Edwards’ campaign disintegrated in scandal, Hillary Clinton and Barack Obama followed his lead on the issue.

The second key proposal was the work of political scientist Jacob Hacker — “the father of the ‘public option,’” according to NPR’s Planet Money — who, a mere two weeks before Edwards came out with his health care plan, published an updated version of his proposal for a Medicare-like public option for those under sixty-five. The public option that all three of the leading Democratic candidates ultimately embraced was, as a 2011 account describes, essentially “a recombination of Hacker’s original Medicare Plus and Halpin’s CHOICE models,” and (rather less clearly) “the only major new idea in the reform debate.”

Yet this ostensibly new idea was to have a short life. Though it became an important focal point in the 2009 health care reform debate, it was eventually killed off by a former Democrat, Connecticut senator Joseph Lieberman, who vowed to oppose the ACA if it included a public option. He got his wish, and a public option-less ACA became law in 2010.

In more recent years, conservatives and liberals have resurrected their own versions of the public option (although only the latter identify them as such). Republicans see it as an instrument for privatization. For instance, under the health care reform frameworkthat Paul Ryan and the House Republicans published in 2016, traditional Medicare would be transformed into a public plan that would compete against private insurance plans in a “Medicare Exchange.” Though Medicare privatization was not included in either the House or the Senate Obamacare repeal bills, the voucherization (and essential destruction) of Medicare remains on the Republicans’ wish list.

In Democratic circles, a public option (for those under sixty-five) is viewed as a potential solution to the inadequacies of the ACA. While Bernie Sanders mainly championed Medicare for All in the Democratic primary, Hillary Clinton — claiming that single-payer would “never, ever” happen — argued instead for a public option and, somewhat similarly, a Medicare “buy in.”

Republican proposals to convert Medicare into a public option for those over sixty-five would obviously take us backward, further privatizing a largely successful and overwhelmingly popular public program. But proposals to create a public option for those under sixty-five, though well intentioned, would fail to take us forward in any meaningful way.

The truth is, both approaches have a common underlying flaw: the notion that “managed competition” between a mixture of public and private insurance plans could save the American health care system. But we don’t need competing public and private insurance plans any more than we need competing public and private air traffic controllers. It adds nothing but waste and a not insignificant degree of hazard.

The Public Option's Cardinal Flaws

Obamacare, most agree, has been going through a rough patch. As of July 12, some 24,525 enrollees in thirty-eight counties were at risk of not having a single insurance option on the ACA marketplaces in 2018, according to the Kaiser Family Foundation.

To some extent, this dysfunction stems from Republican sabotage, especially President Trump’s sometimes-childish yet very consequential threats to cut off payment of Obamacare subsidies to health insurers.

But that’s not the whole story — the malaise in the marketplaces predated Trump. Last summer, for instance, Aetna announced that it was withdrawing from most Obamacare marketplaces, a decision that followed exits by other insurers. Writing in Vox at the time, Hacker, like others, touted the public option as a solution to such troubles. “It’s enough to make a frazzled health care consumer in one of those feeble markets wish there were another option — perhaps even (dare one say it?) a public option,” he wrote.

But here again lies one of the public’s option’s cardinal flaws: whatever it does for those buying insurance on the Obamacare marketplaces (which I’ll return to in a minute), it does basically nothing for the large majority of the nation not insured through them. The so-called “Obamacare” plans cover some 12.2 million enrollees— a substantial number of people to be sure, but still a very small fraction of the population.

What would a public option do, for example, for the 28.6 million US residents who are uninsured? According to the Congressional Budget Office’s (CBO) 2013 scoring of a public option added to the ACA marketplaces, the answer is nothing: the public option, the CBO estimated, “would have minimal effects . . . on the number of people who would be uninsured.”

The goal of single-payer is to reduce that 28.6 million figure to zero; under the public option — at least according to this admittedly old CBO score of one particular variation of the public option — the number wouldn’t so much as budge. Perhaps a more ambitious public option could do a bit better. Nonetheless, it’s not clear that even a more robust plan would be a step toward universal coverage.

And how about for the underinsured? The roughly half of the nation currently covered through their employer saw a 2016 deductible that was 300 percent higher than a decade ago. Such cost-shifting of health care costs to workers is a major cause of financial suffering, as well as deferred medical care. Yet the public option would do nothing for the great majority of these families.

A longstanding aim of universal health care advocates — stretching back to the German Social Democrats’ 1891 Erfurt Program, which called for “[f]ree medical care, including midwifery and medicines” — has been to eliminate out-of-pocket payments (for example, copayments and deductibles) at the time of health care use. In Canada and the United Kingdom, this goal has largely been achieved: most health care remains free when patients use it. The public option, however, would do little to nothing to bring us closer to this goal.

Nor would the public option ameliorate existing deficiencies in the two big public insurance programs, Medicare and Medicaid. Medicare, like private insurance, often imposes high out-of-pocket payments on enrollees, and it excludes coverage for important health services like dentistry and long-term care. The partial privatization of the program (via Medicare Advantage plans, which are managed by private insurance companies) has yielded little but colossal waste over the years.” And while Medicaid has broader benefits and usually minimal out-of-pocket payments, as a result of its lower reimbursements, it sometimes provides inferior access to providers (a vestige of its heritage as a “poor person’s program).

The public option wouldn’t address the inadequacies of either public program.

Finally, in terms of global costs, the public option’s effect would again be quite minor, as single-payer advocates have long noted. Eliminating both uninsurance and underinsurance would cost money, and reduced administrative spending ($503 billion dollars a year, according to one estimate) and reduced drug costs ($113.2 billion a year) are typically cited as key sources of savings. But although a Medicare-like public option may have lower administrative costs, only a small fraction of the efficiency savings of single-payer would be achieved if the multi-payer framework persisted (and drug prices wouldn’t be controlled on a system-wide level).

Or as Physician for a National Health Program’s Don McCanne puts it, the “public option would be only one more player in our wasteful, administratively-complex, fragmented system of financing care.” The upshot? It wouldn’t generate anywhere near the savings needed to fund a truly universal expansion of health care.

Would there be benefits? Probably for some. According to the 2013 CBO estimates, if the public option brought provider reimbursements more in line with those paid by Medicare, its enrollees — which it estimates would account for about 35 percent of those insured through the ACA marketplaces — would enjoy approximately 7 to 8 percent lower premiums. (A 2009 CBO scorethat did not make this assumption, it should be noted, found that premiums might actually be somewhat higher.) Assuming — as the CBO did in 2013 — that about 2 million more individuals would be insured through the marketplaces, this would yield a relatively small reduction in premiums for perhaps some 5 million Americans.

Others in the marketplace could conceivably see a drop in premiums as private plans were forced to compete with the public option. However, given that insurers are currently exiting the marketplace due to what they view as insufficient profitability (even as they raise premiums), it’s hard to see how this would happen.

Of course, if the public option winded up taking on people who are “less healthy — and therefore more costly,” as the CBO assumes, the reform might succeed in “stabilizing” the marketplaces by functioning as a “high risk pool.” In other words, it would essentially subsidize the private insurance industry by socializing the larger health risks (and perhaps increase its profits).

Yet this would also lock into place all the dysfunctions of the health care status quo, perhaps lowering private insurance plan premiums for some but potentially driving up the cost of the public option. More generally, uninsurance would persist while underinsurance could continue to rise.

And the sine qua non of our long-term health care vision — first dollar coverage of world-class medical care for everyone in the nation — would remain unrealized.

What Kind of Reform?

In the 1960s, the French socialist André Gorz introduced a new taxonomy for thinking about reforms. He divided them into two categories: the “reformist reform,” which preserves existing structures, and the “non-reformist reform,” which “is determined not in terms of what can be, but what should be,” and which changes existing structures, opening the door for more fundamental social change.

The public option unfortunately falls into the former category, insofar as it is meant to stabilize the existing insurance marketplace, and therefore the larger multi-payer system.

But this shortcoming isn’t its only problem. We should support defensive battles, and sometimes half-measures, that improve health care — and save lives — even when their long-term structural impact is limited. For instance, pressuring the nineteen state governmentsthat have refused to expand their Medicaid programs is urgently needed. Thousands of lives hang in the balance. The same holds for organizing against Trumpcare, where the stakes have been still higher.

The public option, however, is a different creature: it would require a major nationwide political movement to achieve, and its benefits would not be commensurate with the effort.

Imagine, for a moment, that Democrats got squarely behind a public option, that social movements coalesced around it, that the balance of power in Washington shifted, and that through committed grassroots struggle the private insurance industry’s power was surmounted and a public option finally legislated into existence. Then imagine that all of this had the grand total effect of lowering premiums by, to be generous, 10 percent for a third or so of the 4 to 5 percent of Americans under sixty-five currently insured by marketplace plans.

Would this have been worth the years-long struggle? Sure, the ACA’s turbulent marketplaces might be a bit calmer (and, according to the CBO, the deficit might be smaller). But it would also leave intact the status quo’s injustices and most of its inefficiencies.

Even if we were to fight for a much more expansive public option — as some on the Left have argued we should — the overall picture would not change: costs would remain inadequately controlled, and coverage would remain sub-universal. And from a political standpoint, a public option designed to decimate the private insurance industry might be almost as difficult to achieve as single-payer — despite carrying few of the benefits. In which case, shouldn’t we just fight for the real thing?

A public option would probably help some, and the intentions of its proponents are good. But a public option would not only fail to bring about the long-sought goal of truly universal health care, it could prove to be a dangerous diversion.

We have the capacity for one transformative health care fight in the days ahead. Today, let us rejoice that vampiric Trumpcare seems to be dead. And tomorrow: onwards to real universal health care.

As Senate Prepares For Vote, Susan Collins Says She ‘Simply Cannot Support’ Health Care Plans

by Patty Wight - Maine Public - July 21, 2017

The U.S. Senate is expected to vote on health care next week, though it’s unclear whether they’ll take up a revised version of their bill to repeal and replace the Affordable Care Act or a bill that would just repeal the health care law.

Republican U.S. Sen. Susan Collins of Maine says she doesn’t support either. Speaking to reporters on Friday, she referenced the findings of Congressional Budget Office report on the repeal-only bill.

“That would lead to 32 million people losing health insurance coverage. So I simply cannot support that approach,” she says.

And as for a plan to repeal and replace the ACA, Collins says she’s still opposed, citing drastic cuts to Medicaid.

“You don’t take a safety net program that has been law for more than 50 years and change it in fundamental ways without having a single hearing,” she says.

Collins says she does support a bipartisan approach to fix the Affordable Care Act, and says she’s already discussing next steps with both Democrats and Republicans.

Senate Republicans Don’t Know What Health Care Bill They’re About To Vote For. That’s Nuts.

by Jeffrey Young - Huffington Post - July 24, 2017

The long, halting slog toward Obamacare repeal is set to reach a significant milestone Tuesday, when the Senate is scheduled to vote on ... something.

No, not ”something terrific,” as President Donald Trump promised on the campaign trail. Just ... something. The American public will find out what that something is at about the same time as the Republican senators who Majority Leader Mitch McConnell (R-Ky.) wants to amble down to the well of the Senate, raise their index fingers and say, “Yea.”

Tuesday morning, the Senate is scheduled to begin floor debate on whatever that something is. McConnell is asking GOP senators to approve a procedural motion on a House-passed health care bill, which will then allow him to bring up something else, after which senators will debate and vote on amendments to the something.

No one knows what they’ll be voting to debate. Seriously.

In their zeal to repeal the Affordable Care Act, Senate Republicans have neglected to actually figure out what they want to enact in its stead. More than 40 of them have shown no signs they have any problem with this, and the handful who have wrung their hands in public about it have failed to take the crucial next step of actually coming out against it. Sen. Susan Collins (R-Maine) is the lone exception.

The lives of tens of millions of people and the health care system itself are in the hands of senators who are practically flying blind. And all of this is in the service of legislation that violates Trump’s promises of lower premiums, smaller deductibles, and coverage for everyone. What’s more, polling consistently shows that very few Americans actually want Congress to do any of this.

Just days ago, enough Republican senators had declared they wouldn’t vote on this “motion to proceed” that the effort to repeal the central components of the Affordable Care Act and “replace” them with more meager reforms looked like it might be dead. McConnell pulled the hastily assembled Better Care Reconciliation Act.

But the process showed new signs of life because of pressure from Trump and conservative activists and donors. Another key factor is the lack of conviction among those “moderate” senators who had expressed alarm at the legislation’s massive cuts to federal health care programs, especially Medicaid, but don’t want to be known as the Republicans who killed Obamacare repeal.

Nevertheless, it’s not clear whether McConnell has the 50 votes he needs to move forward, especially with Sen. John McCain (R-Ariz) likely unavailable after being diagnosed with brain cancer.

So, what will happen in the Senate this week?

This bill

McConnell could bring up a version of the Better Care Reconciliation Act, his favored Obamacare “replacement.”

This bill would slash federal Medicaid funding by more than one-quarter, severely weaken the Affordable Care Act’s protections for people with pre-existing conditions; shrink financial assistance for people who buy private health insurance and make it available to fewer people; permit health insurance companies to go back to selling skimpy, junk policies that cover fewer things; and increase costs for older, sicker people in order to allow younger, healthier people to buy insurance with even bigger deductibles than found on the Obamacare exchanges.

This bill would increase the number of Americans without health coverage by 22 million, bringing the total to 50 million in 2026, compared to 28 million if the Affordable Care Act were left in place, the Congressional Budget Office reported Thursday.

That bill

Or McConnell could opt to bring up the Obamacare Repeal Reconciliation Act. Unlike the other bill, this one is all repeal and no replace. Congress passed a version of this bill in 2015, and President Barack Obama vetoed it.

The legislation would take away funding for the Affordable Care Act’s Medicaid expansion and the subsidies low- and middle-income families receive for private insurance, and do away with other key aspects of the law. But it wouldn’t attempt to replace them with anything. And it would cause chaos in the health insurance market by leaving in place Affordable Care Act regulations requiring insurers to cover everyone regardless of pre-existing conditions ― but without a mandate that people buy the insurance or help to make it more affordable.

The legislation would increase the number of uninsured by 32 million over 10 years, including 17 million next year alone, and the total would reach 59 million by 2026.

The other bill

And then there’s the House-passed American Health Care Act (which would leave 23 million more uninsured by 2026). Technically, the legislation must serve as the vehicle for whatever the “something” turns out to be because the Constitution requires bills with tax provisions to originate in the House. In these cases, the Senate typically strips these House bills of all their language and substitutes its own bill. Nevertheless, this measure still fits the definition of “something,” and the Senate could do whatever it wants.

What McConnell actually appears to be doing is teeing up a vote for all these bills, should he get 50 Republicans on the initial motion to proceed. In fact, he seems to be using the promise of a vote as the carrot to gain the support of reluctant senators. In essence, he’s saying, “Help me open debate, and you can vote for whichever bill you prefer!”

Somehow, this tactic seems to be working. Sen. Rand Paul (R-Ky.) opposes the Better Care Reconciliation Act, for instance, but may vote to start debate on the Obamacare Repeal Reconciliation Act, as may Sen. Mike Lee (R-Utah), who has been reluctant to back McConnell’s bill. And moderates, afraid of blocking their party from even debating repeal, may follow suit.

Uh-oh

But wait ― it gets more complicated.

McConnell revised the Better Care Reconciliation Act with new provisions added to win the support of Sen. Ted Cruz (R-Texas) that would create a two-tiered health insurance system in which insurers could sell two sets of policies. One would have to adhere to Affordable Care Act rules about pre-existing conditions and guaranteed benefits, while the other could exclude people based on their health status or medical histories.

Health insurers have warned that this won’t work, because healthy people would rush to buy the cheaper, skimpier plans, leaving sicker people behind in the other market, where their big medical bills would cause premiums to rise so much, they wouldn’t be able to afford insurance. And the healthy people would have policies so meager, they wouldn’t be adequately protected when the day comes that they stop being so healthy.

That Congressional Budget Office score of the Better Care Reconciliation Act doesn’t even factor in the effects of the Cruz amendment because the agency hasn’t had enough time to analyze it, so the Senate is set to begin debate on something no senators actually understand.

And if things go according to McConnell’s schedule and this all wraps up by week’s end, senators likely will be casting their final votes on something before the Congressional Budget Office can complete its work.

Uh-oh ...

And there’s even further complication.

The congressional GOP opted to use a special procedure called budget reconciliation to advance Affordable Care Act repeal because it can’t be filibustered in the Senate and thus can pass with just 51 votes ― including a possible tiebreaker by Vice President Mike Pence in his constitutional role as president of the Senate.

But this comes with a catch: Bills considered under budget reconciliation are supposed to be limited to matters directly affecting the budget, and provisions the parliamentarian deems don’t meet that standard traditionally must be removed.

On Friday, the parliamentarian announced that key parts of the Better Care Reconciliation Act weren’t kosher. They include funding cuts to Planned Parenthoodand provisions limiting abortion, the absence of which would be a deal-breaker for conservatives, as well as insurance regulations seen as key to the new system the bill would create. And, like the Congressional Budget Office, the parliamentarian also hasn’t had time to review the Cruz amendment.

The world’s greatest deliberative body

This, to be absolutely clear, is highly abnormal. Congress gives more care and consideration to bills renaming post offices than it has to legislation with staggering consequences for the health care system.

So, to recap: Senate Republicans are moving forward with legislation that would gut Medicaid, vastly increase the number of Americans without health coverage, jumble the health insurance market in ways that could cause it to collapse, make it harder for people with pre-existing conditions to get and keep health coverage, and expose poor people to unlimited medical costs.

Only they don’t know what the legislation is or what, exactly, it would do. Now that’sreally something.

The Company Behind Many Surprise Emergency Room Bills

by Julie Creswell, Reed Abelson and Margot Sanger-Katz - NYT - July 24, 2017

Early last year, executives at a small hospital an hour north of Spokane, Wash., started using a company called EmCare to staff and run their emergency room. The hospital had been struggling to find doctors to work in its E.R., and turning to EmCare was something hundreds of other hospitals across the country had done.

That’s when the trouble began.

Before EmCare, about 6 percent of patient visits in the hospital’s emergency room were billed for the most complex, expensive level of care. After EmCare arrived, nearly 28 percent got the highest-level billing code.

On top of that, the hospital, Newport Hospital and Health Services, was getting calls from confused patients who had received surprisingly large bills from the emergency room doctors. Although the hospital had negotiated rates for its fees with many major health insurers, the EmCare physicians were not part of those networks and were sending high bills directly to the patients. For a patient needing care with the highest-level billing code, the hospital’s previous physicians had been charging $467; EmCare’s charged $1,649.

“The billing scenario, that was the real fiasco and caught us off guard,” said Tom Wilbur, the chief executive of Newport Hospital. “Hindsight being 20/20, we never would have done that.” Faced with angry patients, the hospital took back control of its coding and billing.

Newport’s experience with EmCare, now one of the nation’s largest physician-staffing companies for emergency rooms, is part of a pattern. A study released Monday by researchers at Yale found that the rate of out-of-network doctor’s bills for customers of one large insurer jumped when EmCare entered a hospital. The rates of tests ordered and patients admitted from the E.R. into a hospital also rose, though not as much. The use of the highest billing code increased.

“It almost looked like a light switch was being flipped on,” said Zack Cooper, a health economist at Yale who is one of the study’s authors.

In a statement, EmCare described the study as “fundamentally flawed and dated.” But it acknowledged that surprise billing, as the billing is called when the doctor is unexpectedly not part of an insurance network, is “a source of dissatisfaction for all payors, providers and patients in our current health care system.” It said that the issue was not specific to any one company, and that it had already publicly committed to reaching agreements with insurers for the majority of its doctors within the next two years. This study, and others, have found that EmCare is not alone in the practice of sending out-of-network bills.

EmCare said that it allowed hospitals to treat sicker patients when it takes over, and that an increase in such patients explained the higher billing in Newport.

In the study, the researchers examined nearly nine million visits made to emergency rooms run by a variety of companies between 2011 and 2015, using data from a single insurance company that does business in every state. In exchange for access, the researchers agreed not to identify the insurer. Insurers and health care providers typically sign contracts forbidding them to reveal the prices they have agreed to, and the national trends in surprise billing detected by the Yale team are consistent with a broader study by government researchers.

The new data suggests that EmCare, part of publicly traded Envision Healthcare, did not sign contracts with the insurance company and was able to charge higher prices.

Fiona Scott Morton, a professor at the Yale School of Management and a co-author of the paper, described the strategy as a “kind of ambushing of patients.” A patient who goes to the emergency room can look for a hospital that takes her insurance, but she almost never gets to choose the doctor who treats her.

Sometimes, insurers simply pay higher out-of-network bills, but the cost is often passed on directly to patients.After slipping on some wet leaves outside her house in Crescent City, Calif., in February, Debra Brown, a 60-year-old county accounting clerk, wound up at Sutter Coast Hospital. She is paying off her deductible, but her insurer covered most of her remaining hospital bill. She was shocked to get an additional bill from a doctor who she said never identified himself and only briefly touched her broken ankle. That physician worked for EmCare. Her portion of the bill is more than $500.

“Now I’m going to have to pay this bill off, and I can’t afford to see a doctor about my high blood pressure medication,” Ms. Brown said. “This is insane, and it’s greedy.”

Nationwide, more than one in five visits to an in-network emergency room results in an out-of-network doctor’s bill, previous studies found. But the new Yale research, released by the National Bureau of Economic Research, found those bills aren’t randomly sprinkled throughout the nation’s hospitals. They come mostly from a select group of E.R. doctors at particular hospitals. At about 15 percent of the hospitals, out-of-network rates were over 80 percent, the study found. Many of the emergency rooms in that fraction of hospitals were run by EmCare.

When emergency room doctors work for a company that has not made a deal with an insurer, they are free to bill whatever they want, insurers say. “The more they bill, the more they get paid,” said Shara McClure, an executive with Blue Cross of Texas.

E.R. doctors say out-of-network billing isn’t their fault. Sometimes, insurance companies will offer only low payments, leaving physicians no choice, said William Jaquis, an executive with the American College of Emergency Physicians, who is also an E.R. physician employed by EmCare. Doctors would “prefer that we had better payment and better negotiation with the insurers, and the patients would be covered,” he said.

The researchers focused on 16 hospitals that EmCare entered between 2011 and 2015. In eight of those hospitals, out-of-network billing rose quickly and precipitously. (In the others, the out-of-network rate was already above 97 percent, and it did not go down.) They also looked at a larger sample of 194 hospitals where EmCare worked and found an average out-of-network billing rate of 62 percent, far higher than the national average.

The before-and-after analysis was limited to the small number of hospitals where the researchers could find public records of EmCare’s entrance, and it was based on claims from only one large insurance company. While the nationwide patterns are consistent with studies that have looked at other insurance companies, the single insurer in the study may not be typical in all cases: EmCare does participate in some insurers’ networks, such as Blue Cross of Texas. EmCare also says it has reached agreements with more insurers in Texas, Arizona, Florida and Virginia since 2015.

Researchers also examined what happened when one of EmCare’s top competitors — TeamHealth — took over a handful of mostly nonprofit emergency departments. There, they found a smaller increase in out-of-network billing and virtually no change in hospital admissions, testing or coding.

Analysts point out that hospitals, despite any patient complaints, can benefit financially from the increased testing and admissions EmCare has delivered. In the study, surprise bills were more common at for-profit hospitals than at their nonprofit competitors.

“They’d have to have their heads in the sand to be totally unaware” about the out-of-network billing, said Leemore Dafny, a professor at Harvard Business School, who reviewed the research.

EmCare’s emergency room management has come under scrutiny before. The company was named in a 2011 whistle-blower lawsuit against Health Management Associates, a for-profit hospital chain. The suit alleges that both EmCare and the hospitals pressured E.R. doctors to increase admissions and tests, even when the physicians believed they were not medically necessary. The company “repeatedly terminated physicians and E.R. medical directors” who pushed back, the suit says. The case, which was brought by a hospital chief executive and a former EmCare executive, is still pending. Envision said it does not comment on pending litigation.

Hospital emergency departments, which must take all comers regardless of their health insurance, were once viewed as financial drains. Then hospital leaders started to see the E.R. as the front door, critical to attracting paying patients. In the early 1990s, emergency departments accounted for a third of admissions to hospitals; today, they account for half, according to a RAND study.

As in so many other parts of the modern economy, turning operations over to large outside contractors has been a big part of the transition. Nearly a quarter of all emergency room doctors now work for a national staffing firm, according to a 2013 Deutsche Bank report.

EmCare in particular has thrived. Founded in the 1970s, it has grown rapidly in recent years.

Its sales pitch to hospitals is that it can find high-quality doctors and run emergency rooms more efficiently. It offers a software program called RAP & GO (short for Rapid Admission Process and Gap Orders) that it says speeds admissions and potentially produces “significant new hospital revenue.”

Some doctors say the staffing companies save them from the administrative headaches of billing and scheduling.

In addition to its work in emergency rooms, EmCare has been buying up groups of anesthesiologists and radiologists. In these hospital specialties, it is hard for patients to shop, and out-of-network billing is common.

EmCare’s size and reach have made some doctors wary of criticizing its practices. According to Dr. Carol Cunningham, an emergency room physician in Ohio, that is especially true in places where there is little alternative to working for a large staffing company. “You may have trouble finding something in the area,” she said.

But some doctors outside the E.R. have been less reticent. Dr. Gregory Duncan, chief of surgery at Sutter Coast Hospital in Crescent City, Calif., said patients started complaining about bills they received after EmCare took over the emergency room in 2015.

“I discovered a pattern of inflated bills and out-of-network bills,” he said. “What they are doing is egregious billing.”

Dr. Duncan, who also sits on the county health care district board, has joined with other elected officials in asking Sutter Coast to terminate its contract with EmCare.

In an emailed response, Mitch Hanna, the chief executive of Sutter Coast, said the hospital chose EmCare because of its ability to fully staff its emergency department. He added that he understood EmCare was working to bring two large commercial insurers into its network by the end of the year.

EmCare said in early February that it planned to reach agreements with insurers for most of its doctors. The company also said it was working with insurers, hospitals, lawmakers and others to make sure patients get appropriate care “without creating undue financial burden.” The American College of Emergency Physicians favors an approach in which out-of-network emergency room doctors are paid a standard rate.

California recently passed a law setting a maximum amount that out-of-network doctors can charge patients. Other states, including Florida and New York, have also passed laws to limit surprise bills.

But many state efforts to reduce surprise billing have been met by fierce lobbying from doctors who oppose efforts to weaken their bargaining position, said Chuck Bell, the programs director at the consumer advocacy group Consumers Union.

“The whole thing is really a mess,” he said. “Progress is really slow.”

Editor's Note:

One clarification to the following post: The IFS Committee of the legislature actually voted on a substitute bill to the original LD 1274, that authorized the establishment of a committee to study various approaches to health system reform in Maine.

-SPC

Maine AllCare Finds Community Support at Fisherman’s Day in Stonington

by Joe Lendvai - Bangor Daily News - July 24, 2017